So I ask my friend who’s in the car business: “When those stimulus checks come out, do you get busy?”

He says: “Yeah! Those are down payments.”

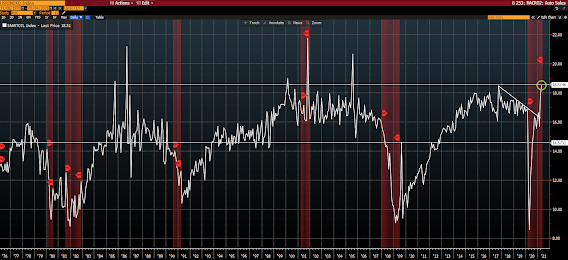

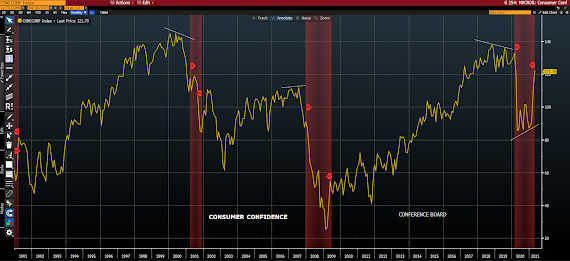

Well, we still have north of a half-million folks filing first-time unemployment claims each week, and, yet, we have auto sales hitting levels not seen since 2005, a manufacturing sector that’s running red hot, and consumer confidence that’s breaking out firmly to the upside.

U.S. auto sales past 45 years:

And speaking of the red-hot manufacturing sector, while this morning’s ISM Manufacturing Survey’s overall score came in under expectations, a 60.7 is still nothing to sneeze at; anything over 50 denotes month-over-month expansion.

- “The current electronics/semiconductor shortage is having tremendous impacts on lead times and pricing. Additionally, there appears to be a general inflation of prices across most, if not all, supply lines.” (Computer & Electronic Products)

- “Upstream producers/suppliers are back online and working towards full rates. Demand is outpacing supply and will continue into the third quarter, when the supply chain is expected to be refilled. Supply/demand should be more balanced in Q3/Q4, but demand will continue as customers run hard to meet their demand and rebuild inventory.” (Chemical Products)

- “Continued strong sales; however, we have had to trim some production due to the global chip shortage. Hasn’t affected inventories greatly yet, but a continued decrease will begin to reduce available inventories if we don’t recover chip supply shortly.” (Transportation Equipment)

- “Business is picking up as restaurants open.” (Food, Beverage & Tobacco Products)

- “Oil production has been steady, along with market prices and capital expenditures.” (Petroleum & Coal Products)

- “Steel prices are crazy high. The normal checks on the domestic steel mills are not functioning — imported steel is distorted by the Section 232 tariffs.” (Fabricated Metal Products)

- “It’s getting much more difficult to supply production with materials that are made with copper or steel. Lots of work on the floor, but I am worried about getting the materials to support.” (Electrical Equipment, Appliances & Components)

- “Market capacity in most areas is oversold, with no realistic improvement on the horizon. In fact, it appears that demand will continue to strengthen, leading to more significant disruptions.” (Furniture & Related Products)

- “In 35 years of purchasing, I’ve never seen everything like these extended lead times and rising prices — from colors, film, corrugate to resins, they’re all up. The only thing plentiful at present, according to my spam filter, is personal protective equipment [PPE].” (Plastics & Rubber Products)

- “The metals markets remain very challenging at best. Shortages of raw materials have increased, especially in aluminum and carbon steel. Prices continue to rapidly increase. Transportation and trucking [are] also a big challenge.” (Primary Metals)

- “Demand continues to be very strong. Supply chain delays hamper our availability and ability to sell more.” (Machinery)

All this optimism, and upward pressure on manufacturing, etc., and somebody has the nerve to write an article that inspires a friend to pose the following via email to me yesterday:

“Marty, agree with this?:

A 10% drop or at least a pause could be looming for the S&P 500. Take shelter in these sectors, says veteran strategist

Sell in May and go away? How about ‘curb your enthusiasm,’ says our call of the day from Stifel.

Read in MarketWatch: https://apple.news/AJiT6AW_FSAijQQCDocBdKA“

“Yeah, sure… while of course I have my own thoughts on how to hedge, and what sectors make sense, this market is extended in ways seldom (never, in many respects) seen.

Double-digit corrections from these valuation levels, etc., are an absolute given…

Seasonality places a higher risk of that over the next few months…

Then when the market realizes that government injections (and debt), in the trillions, is what held the ship together, well, business is going to have to come back hugely (and some!) just to compensate for what happens when the government spigot gets dialed back, taxes go up, etc...”

So — my “absolute given” aside (a true/legit prediction needs a more specific time frame, right?) — am I predicting pain in the near, or the longer, term? Nope. I am, however, pointing to the unusual circumstances we find ourselves in, and the risks they present…

My general message above is that, due to government intervention, we’re seeing a massive pull-forward of activity. It therefore makes sense that we’ll feel a notable letdown at the point when activity that would’ve happened doesn’t, because it already did…

Asian equities struggled overnight, with 2/3rds of the markets we track closing lower (China’s on-shore, and Japanese markets were closed).

Europe’s struggling notably this morning as well, with all but 3 of the bourses we follow in the red (Greek markets are closed today).

U.S. major averages are off (tech-heavy Nasdaq especially) to start the day as well: Dow down 238 points (0.64%), SP500 down 1.00%, SP500 Equal Weight down 0.54%, Nasdaq 100 down 2.35%, Nasdaq comp down 1.98%, Russell 2000 down 1.24%.

The VIX (SP500 implied volatility) is up 7.63%. VXN (Nasdaq i.v.) is up 11.27%.

Oil futures are up 1.22%, gold’s up 0.13%, silver’s down 0.24%, copper futures are down 0.09% and the ag complex is up 0.70%.

The 10-year treasury is up (yield down) and the dollar is up 0.34%.

Led by metals miners, AT&T, ag commodity futures, uranium miners and Verizon — but dragged by solar stocks, ALB (lithium miner), wind stocks, tech stocks and Eurozone stocks — our core portfolio is off 0.44% as I type.

“It is impossible to understand the world if you insist on thinking in absolute terms. The world is not black and white. Everything has shades of gray.”

Have a great day!

Marty