Core PCE (personal consumption expenditures) inflation bested expectations; up 0.7% month-on-month — that’s not a little. And while the debate — transient vs structural inflation — will rage on for months to come, suffice to say that higher prices look to be hanging around awhile.

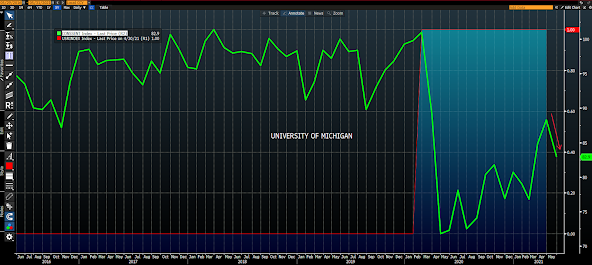

We’ll tackle macro in depth in our weekly update coming your way later today, or tomorrow at the latest. In the meantime, I’ll tease it with a quick note on the just-now released University of Michigan Consumer Sentiment Survey.

Here’s a 5-year chart of the index:

Asian equities leaned green overnight, with 10 of the 14 markets we track closing higher.

Europe’s higher nearly across the board this morning, with 16 of the 19 bourses we follow trading up as I type.

U.S. equities are mostly (save for smallcaps) higher to start the session: Dow up 99 points (0.29%), SP500 up 0.23%, SP500 Equal Weight up 0.08%, Nasdaq 100 up 0.48%, Nasdaq Comp up 0.38%, Russell 2000 down 0.13%.

The VIX (SP500 implied volatility) is down 1.55%. VXN (Nasdaq 100 i.v.) is down 2.08%.

Oil futures are up 0.04%, gold’s down 0.06%, silver’s down 0.43%, copper futures are down 0.25% and the ag complex is up 0.57%.

The 10-year treasury is up (yield down) and the dollar is up 0.27%.

Led by healthcare stocks, uranium miners, solar stocks, Asia Pac stocks and utilities stocks — but dragged by metals miners, ALB (lithium miner), bank stocks, oil services stocks and base metals futures — our core portfolio is up 0.22% to start the day.

While we track historical patterns and perform deep fundamental and technical analyses ad nauseam, it’s critically important that we constantly think outside the box and remain on our toes. As, frankly,

“…popular math tools and risk models are incapable of sufficiently preparing investors for large and highly unpredictable deviations from historic patterns—deviations that occur more frequently than most models suggest.” — Gregory Zuckerman

Have a great day!