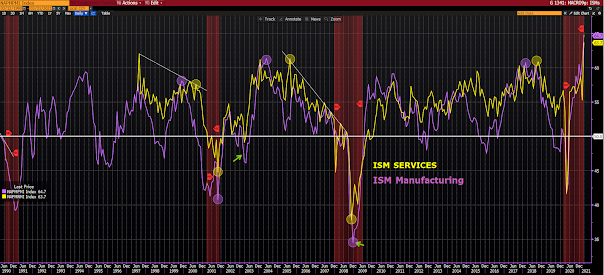

In last Friday’s macro video I pointed to the huge spike in the purple line below:

Commodities Up in Price:

Acetone (2); Acrylonitrile Butadiene Styrene (ABS) Plastic (3); Adhesives; Aluminum (10); Aluminum Extrusions (2); Brass Products; Copper (10); Copper Products; Corn; Corrugate (6); Corrugated Boxes (5); Crude Oil (4); Diesel (3); Electrical Components (4); Electronic Components (4); Epoxy Resins; Ethylene; Freight (5); Foam Products; High-Density Polyethylene (HDPE) (3); Isocyanate; Labor — Temporary; Light Emitting Diode (LED) Displays; Lumber (9); Medium-Density Fiberboard (MDF); Nylon Fiber (3); Ocean Freight (4); Oil-Derived Products (2); Packaging Supplies (4); Paper Products (4); Petroleum-Based Products; Phosphates; Plastic Resins (7); Plasticizers; Polyethylene (2); Polypropylene (9); Polyvinyl Chloride (PVC) (6); Propylene (3); Resin-Based Products (2); Rubber Products (2); Semiconductors (2); Solvents — Other (2); Soybean Products (6); Steel (8); Steel — Carbon (4); Steel — Cold Rolled (7); Steel — Galvanized; Steel — Hot Rolled (7); Steel — Scrap (4); Steel — Stainless (5); Steel Products (7); Styrene; Surfactants; Wire Products; Wood — Pallets (4); and Vinyl Acetate Monomer.Commodities Down in Price

None.

Commodities Up in Price

Chemicals; Construction Materials; Construction Services; Copper Products (2); Diesel (4); Electrical Components (2); Exam Gloves (6); Food & Beverage; Freight (4); Fuel (3); Gasoline (4); Gasoline-Related Products; Labor (4); Labor — Construction; Labor — Temporary (3); Lumber (3); Oriented Strand Board (OSB) (4); Packaging Materials; Paint-Related Products; Personal Protective Equipment (PPE)* (14); PPE — Gloves (6); Poly Products; Polyvinyl Chloride (PVC) Products (7); Resin Products (3); Steel (7); Steel Conduit; Steel Products (3); Steel — Rolled; Trucking Services; and Wood Products (2).Commodities Down in Price

Personal Protective Equipment (PPE).

As for the respondents’ featured commentary, economist Peter Boockvar sums up the sum-up nicely:

“The ISM summed up the release by saying “Respondents’ comments indicate that the lifting of covid related restrictions has released pent-up demand for many of their respective companies’ services. Production capacity constraints, material shortages, weather and challenges in logistics and human resources continue to cause supply chain disruption.”

Me: this is a recipe for continued cost pressures.

Will companies be able to pass it on?

Markit said this today in their revised services PMI release after saying “input costs soared in March”, “Subsequently, firms sought to pass on higher costs to clients through a sharper rise in selling prices. A number of companies also stated that stronger client demand allowed a greater proportion of the hike in costs to passed through. The resulting rate of charge inflation was the quickest on record.””

14 of the 16 Asian equity markets we track reopened last night, and their results were mixed: 8 higher, 6 lower on the session.

Europe’s leaning green this morning, with 14 of the 19 bourses we follow presently higher on the session.

U.S. major averages are, save for the Russell, fairly flat to start the session: Dow up 7 points (0.02%), SP500 up 0.13%, SP500 Equal Weight up 0.33%, Nasdaq 100 down 0.03%, Russell 2000 up 0.57%.

The VIX (SP500 implied volatility) is up 0.39%. VXN (Nasdaq 100 i.v.) is up 0.25%.

Oil futures are up 3.29%, gold’s up 0.80%, silver’s up 1.16%, copper futures are down 0.75% and the ag complex is up 0.83%.

The 10-year treasury is up (yield down) and the dollar is down 0.17%.

Led by solar stocks, oil services, gold miners, energy and silver — but dragged by wind stocks, Eurozone equities, Asia Pac equities, MP (rare earth miner) and utilities — our core mix is up 0.19% to start the day.

I’m enjoying Diego Parrilla’s latest book The Anti-Bubbles, probably because I sympathize with his general thesis. I, as regular readers know, also share his cynicism around the government’s inflation numbers:

“The convenience of having inflation benchmarks give the governments significant power, as they can conveniently adjust composition and weightings of the inflation basket to achieve their own objectives, and explains why many of these indicators conveniently exclude energy prices or housing, despite being major components of our true inflation basket.”

Have a great day!