Yesterday I suggested that the setup for today (Fed meeting wrap up) was volatility.

With the Dow down 162 points, and the SP500 down 0.08% and the Nasdaq Comp off by 0.28% — well..… volatility? While equities did jump around a bit as Powell spoke, not so much, at least not in stocks…

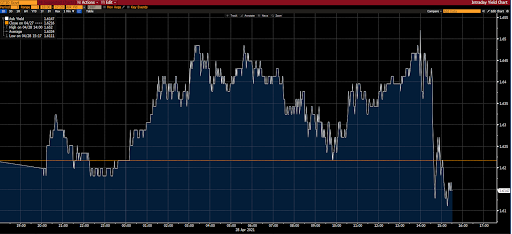

Bond volatility, however, is worth mentioning.

Here’s the 10-year treasury yield today:

“Really don’t think the Fed “wants it (inflation) hot”. “Hot” would have them tightening.

The Fed talks up what they want, especially when it’s not there. They have been talking down inflation (or talking up “transitory inflation”) because if indeed it’s running hot, they’ll have to tighten — and in this setup they’ve backed themselves into — tapering is indeed tightening. I.e., tapering will have a serious knock-on tightening effect in markets.

Longer-term, analysts like V. Deluard make a compelling case for structural changes in Asia — moving from export driven (exporting deflation) models to consumption, which, along with what amounts to heightened pushback against globalization — leaving a real risk of structural/long-term global inflation going forward.

Not to mention, we’re looking at a fiscal impulse that — when coupled with a debt bubble that presents the greatest ycc (yield curve control) odds since the ’40s — could very well provoke longer-term inflation without the normal interest rate mechanism doing its job (in terms of cooling)”