I’ll be out of town this weekend, so I’m crunching the essential weekend tasks into today’s things to do. Thus, I’ll keep this week’s macro note brief and to the point.

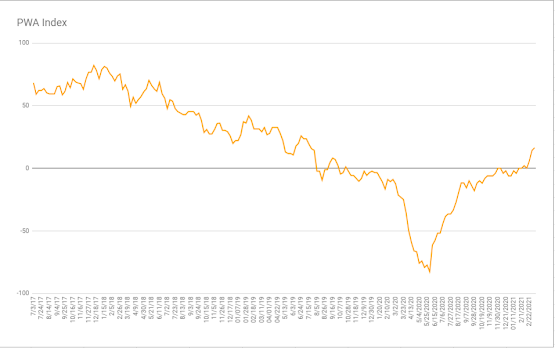

Our PWA Macro Index continues to reflect notably improving economic conditions (please read this morning’s important note to get a feel for the equity market implications), increasing another 2.04 points this week, to +16.33:

“The coronavirus [COVID-19] pandemic is affecting us in terms of getting material to build from local and our overseas third- and fourth-tier suppliers. Suppliers are complaining of [a lack of] available resources [people] for manufacturing, creating major delivery issues.” (Computer & Electronic Products)

“Supply chains are depleted; inventories up and down the supply chain are empty. Lead times increasing, prices increasing, [and] demand increasing. Deep freeze in the Gulf Coast expected to extend duration of shortages.” (Chemical Products)

“Steel prices have increased significantly in recent months, driving costs up from our suppliers and on proposals for new work that we are bidding. In addition, the tariffs and anti-dumping fees/penalties incurred by international mills/suppliers are being passed on to us.” (Transportation Equipment)

“We have experienced a higher rate of delinquent shipments from our ingredient suppliers in the last month. We are still struggling keeping our production lines fully manned. We anticipate a fast and large order surge in the food-service sector as restaurants open back up.” (Food, Beverage & Tobacco Products)

“Overall capacities are full across our industry. Logistics times are at record times. Continuing to fight through shipping and increased lead times on both raw materials and finished goods due to the pandemic.” (Fabricated Metal Products)

“Prices are going up, and lead times are growing longer by the day. While business and backlog remain strong, the supply chain is going to be stretched very [thin] to keep up.” (Machinery)

“Things are now out of control. Everything is a mess, and we are seeing wide-scale shortages.” (Electrical Equipment, Appliances & Components)

“Labor shortages at suppliers are affecting material deliveries and prices.” (Plastics & Rubber Products)

“We have seen our new-order log increase by 40 percent over the last two months. We are overloaded with orders and do not have the personnel to get product out the door on schedule.” (Primary Metals)

“A sense of urgency is being felt regarding new orders. Customers are giving an impression that a presence of stability is forthcoming and order flow is increasing.” (Textile Mills)

“Prices are rising so rapidly that many are wondering if [the situation] is sustainable. Shortages have the industry concerned for supply going forward, at least deep into the second quarter.” (Wood Products)

“Suppliers are taking the opportunity with the commodity-price increases in the last few months to propose price increases that are above and beyond normal expectations, causing significant concern. Business growth remains optimistic on the emergence of a post-coronavirus [COVID-19] era in [the] second half of 2021. U.S. port delays are problematic.” (Accommodation & Food Services)

“The declining COVID-19 cases in the four states we operate in, combined with the increased vaccination rates, should bode well for our increased business activity moving into the second quarter of 2021.” (Arts, Entertainment & Recreation)

“Sales of residential real estate continue to be strong, even outstripping supply. Cost inflation in building materials seen as shortages develop from sporadic COVID-19 closures at manufacturing facilities. Port congestion on the West Coast [and] winter weather in Canada closing mills and restricting truck shipping are contributing to product shortages nationwide.” (Construction)

“COVID-19 restrictions continue to affect the number of students either applying to college, living on campus or finding alternative means of a valuable education. As such, revenues have decreased while expenses increased.” (Educational Services)

“Business is steady during Q1 2021.” (Finance & Insurance)

“Exponential demand for critical supplies due to [the] pandemic is driving distributer allocations and forcing alternative sourcing.” (Health Care & Social Assistance)

“Our company has an overall positive outlook, with new COVID-19 cases trending down nationally and vaccine distribution coming online. However, possible changes to the regulatory environment for oil and gas is a looming negative influence.” (Management of Companies & Support Services)

“The business continues to reduce real-estate/brick-and-mortar [operations] and transition to a work-from-home model. Innovation is the watchword in all things; as such, the need to right-size all consumption as patterns have changed.” (Information)

“Supplier deliveries continue to be an issue as well as lead-times. Additionally, price increases are occurring with more frequency for products containing raw materials such as copper and steel.” (Retail Trade)

“Construction and customer activity remains robust. Many materials have inconsistent lead times or are facing delivery delays.” (Utilities)

“We are seeing an ongoing influx of price increases due to raw-material shortages, labor shortages, and transportation delays.” (Wholesale Trade)

“We were excited [in January], when orders and activity were increasing. Now, they are not receding, but they’re flat month over month. That’s not the rebound we were hoping for.” (Professional, Scientific & Technical Services)

Suffice to say that the balance of economic risks — for the moment — has shifted from contraction to potentially major overheating. Hence the challenge for markets I discussed in my earlier note this morning.

Have a nice weekend!

Marty