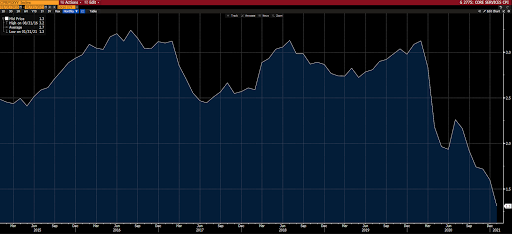

All in, January saw a moderate 1.4% year-on-year headline CPI print:

The above (headline print) has bonds rallying, yields falling, this morning…

It’ll be interesting to see how the bond market treats the inevitable catch up in services prices to come once we’re over the COVID hump, and how the Fed ultimately deals with it.

Speaking of which, the current Fed heads — as they forever do — say inflation’s not a worry and what we’re seeing, and will see going forward, is only “transitory”…. Ah, but once they’re off the board and onto the uber-lucrative speaking circuit, or off to write their memoirs, my how the narrative instantly changes.

I found Greenspan’s post-fed writings to be insightful and enlightening. I don’t know how many times (lots), however, while reading those books I found myself muttering “dude, who are you? I was there, I watched you in action!”

I.e., no longer being the man who had to save the world by bailing out failed institutions and desperately attempting to keep bubbles afloat, the maestro was free to tell it like it is, or like it should be.

Now we have the esteemed Bill Dudley; a most accommodating and line-toeing Fed board member during his tenure as NY Fed president from 2009 to 2018. This morning, however, he’s writing on the huge risk of some serious, potentially policy-impacting, inflation to come. (h/t Peter Boockvar)

Here’s the close to his Bloomberg piece this morning:

“All this suggests that the Fed, despite its desire to be accommodative and boost employment, might have to pull back on stimulus sooner and with greater force than anticipated to keep inflation in check.

Such a move would be a significant surprise, given that in the Fed’s most recent Summary of Economic Projections, the median projection foresees no rate hikes through 2023.

This, in turn, would further increase the chances of a volatile market reaction, along the lines of the taper tantrum that the U.S. experienced in 2013.”

Dude, who are you?!?

Asian equities leaned green overnight, with 10 of the 16 markets we track closing higher.

Europe’s mixed; with 9 of the 19 bourses we follow in the red so far this morning.

The U.S. major averages opened nicely higher, but are rolling into the red as I type: Dow down 31 points (0.10%), SP500 down 0.19%, Nasdaq down 0.49%, Russell 2000 up 0.81%.

The VIX (SP500 implied volatility) is up (3rd day running) 6.70%. VXN (Nasdaq i.v.) is up 5.49%.

Oil futures are up 0.19%, gold’s up 0.30%, silver’s down 0.55%, copper futures are up 1.32% and the ag complex is down 0.72%.

The 10-year treasury is up (yield down) and the dollar is down 0.14%.

Buoyed by energy, base metals, gold, gold miners, utilities and banks — but dragged almost equally by ag commodities, base metals miners, silver, tech and AT&T — our core portfolio is up 0.03% to start the day.

So, former fed chair/current treasury secretary Janet Yellen recently told Congress that now’s the time to go big on borrowing and spending… Hmm… I wonder what she’ll be saying about deficit spending once she heads back to the real world.

Here’s what Alan Greenspan had to say in his post-fed-life best seller The Age of Turbulence:

“Big deficits have an insidious effect. When the government overspends, it must borrow to balance its books. It borrows by selling treasury securities, which siphons away capital that could otherwise be invested in the private economy.“