As is usually the case I have much queued up to share with you in our main weekly message.

Having sifted through the data and macro commentary I found worthy to cite, I’ve decided to keep it in queue this week and instead offer up some highlights from our lengthy 2020 year-end message.

As much of it touches on/confirms much of what I have queued up to share.

From Part Two: The “Momentum” We’re Concerned With:

However, there’s another momentum that — with other peoples’ fortunes at stake — I feel demands even greater attention/study than does the momentum in price.

That would be the momentum in/direction of the underlying fundamentals.And while, for the moment, underlying fundamentals are taking a back seat (well, they’re presently locked away in the trunk) to headlines and price momentum, I still subscribe to the following profound statement by retired hedge fund manager Colm O’shea.

Like O’shea, I equate the price action by itself more to wind than I do tide. The tide being the fundamentals:

“People get all excited about the price movements, but they completely misunderstand that there is a bigger picture in which those price movements happen. Price movements only have meaning in the context of the fundamental landscape.

To use a sailing analogy, the wind matters, but the tide matters too. If you don’t know what the tide is, and you plan everything based on the wind, you are going to end up crashing into the rocks.””

From Part Three: Bubbles, Zombification, the Fed and the Future

“There’s much more we could dissect with regard to Japan’s post-80s economy — ~zero interest rates in perpetuity, central bank balance sheet, lousy demographics, waning productivity, etc. — but suffice to say that virtually all of it, even to some degree lousy demographics (read immigration policies, and the correlation between wage growth/standard of living and population growth), results from government’s unwillingness to allow markets to clean up the messes government creates.

And, lastly, before we tackle today’s debt bubble, while the above may sound dire, understanding what policymakers will have to bring to bear in their attempts to avert a worse-than-2008 financial market scenario brings clarity (read opportunity) to the portfolio management process…”

From Part Four: The Good, the Bad and the Ugly — And — Lessons of Nature

“Like no other time in history, stock markets have the support of policymakers.

Years of business cycle manipulation, resulting in persistently low interest rates, have established stocks as the perceived only game in town to capture yield and to beat inflation.

In fact, or in addition, it’s little stretch to say that stocks these days in the eyes of many possess money-like qualities, as people succumb to the allure of ever-rising prices supported by ever-present “money” printing and move their life savings into the market.

The Fed, having boxed themselves (and, alas, the economy) into a place where the world is so heavily-leveraged against stock prices, and, now, everyday folks (in terms of perceived safety) mistake stocks for money, have — in their minds — no choice but to do everything possible to keep the market levitated virtually ad infinitum.

For the moment, while policymakers’ backstopping stocks is plenty to like all by itself, it would indeed be a stretch to, at this time, confidently expand a list of good reasons to own them — in the aggregate, that is.

On a sector by sector basis, however, absolutely, when, for example, we consider infrastructure spending on the horizon, and, thinking globally, when we branch beyond U.S. borders, there are indeed opportunities in stocks to be thoughtfully exploited going forward.”

From Part Five: Commodities and the Dollar

“…in that commodities the world over are mostly traded in U.S. dollars, our longer-term weak-dollar thesis makes maintaining some commodities exposure going forward a no-brainer.

Secondly, the world is in stimulus mode like I personally have never seen it:

China is on yet another tear when it comes to infrastructure spending within their own economy; gobbling up much of the world’s industrial commodities production in the process. Plus, with their “One Belt, One Road” initiative, they are rapidly expanding across the globe, financing infrastructure projects from East China through Southeast and South and Central Asia all the way to Europe.

And while there’s much to parse in this massive global outreach — including the potential to provide a huge springboard for China’s own digital currency, which some view as the most credible threat to the U.S. dollar’s global dominance going forward (a serious topic we’ll no doubt broach often and in detail in the months to come) — make no mistake, with regard to commodities demand, it’s big!

And, as we know, the U.S. is sorely overdue in its own infrastructure ambitions. Hence we look for a trillion or three of fresh government borrowing and spending in that direction over the coming months/years.

Thirdly, given the weak price action over the past decade, commodities producers have notably cut their spending, thus reducing overall capacity.

Growing demand against reduced capacity of course leads to higher prices…

Yes, contrary to the opinion of many a pundit, inflation is no small risk going forward…”

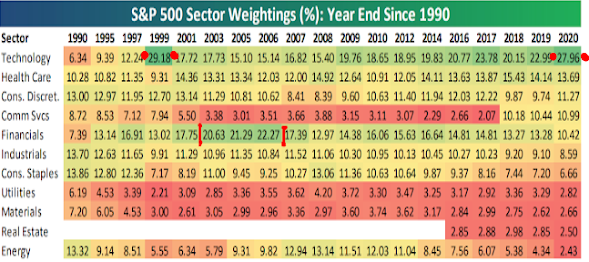

“In this part six of our year-end letter I’ll present an overview of how we see the U.S. equity market setup on a sector by sector basis.

First, let’s take a look at how the major sectors stack up in terms of their weightings within the S&P 500 Index (compliments of Bespoke Investment Group).

I.e., our hedging portfolios these days has zero to do with bent or bias… It’s all about data, human nature, and history…”

Here’s a 30-year look:

“As I suspect you’ve pondered, COVID changes things big time in the workplace. And/or, we might say, COVID has accelerated preexisting trends in the workplace — per the following from the World Economic Forum’s The Future of Jobs Report 2020, published in October:

“The COVID-19 pandemic-induced lockdowns and related global recession of 2020 have created a highly uncertain outlook for the labour market and accelerated the arrival of the future of work.”“The adoption of cloud computing, big data and e-commerce remain high priorities for business leaders, following a trend established in previous years.”

“In addition to the current disruption from the pandemic-induced lockdowns and economic contraction, technological adoption by companies will transform tasks, jobs and skills by 2025.”

“By 2025, the time spent on current tasks at work by humans and machines will be equal.”“A significant share of companies also expect to make changes to locations, their value chains, and the size of their workforce due to factors beyond technology in the next five years.”

“On average, companies estimate that around 40% of workers will require reskilling of six months or less and 94% of business leaders report that they expect employees to pick up new skills on the job, a sharp uptake from 65% in 2018.”“Eighty-four percent of employers are set to rapidly digitalize working processes, including a significant expansion of remote work—with the potential to move 44% of their workforce to operate remotely.”

And, make no mistake:

“…inequality is likely to be exacerbated by the dual impact of technology and the pandemic recession.”

Although I’d say “by the triple impact of technology, recession, and what amounts to utterly egregious government-funded bailouts of junk debt-hoarding hedge funds and private equity firms.”

If you think 2020’s stock market action remotely discounted the changes (read risks and opportunities) to come, I’m afraid you’ll need to think again.”