Of all the things I might attest to, the notion that there’s much more to investing than passively riding the market wave would be one in which I’d have high conviction.

Now, note that those few challenging past periods (when the price action deviated epically from the fundamentals) left a trail of destruction in their wake that would have any tutored, experienced and/or historically-studied portfolio manager today diversifying into non-correlated (to stocks) asset classes and hedging their equity exposure against disaster using options.

No doubt, I’m a contrarian by nature. However, if I aspire to those world’s-best portfolio manager traits I outlined in Part One of this year’s final message, #s 5, 7 and 8 demand that I can never be contrary simply for contrary’s sake.

Here, once again, are all 8:

1. A passion for macro economics and market history

2. A firm understanding of intermarket relationships

3. A firm grasp of global macro and geopolitical developments

4. An obsessively strong work ethic

5. The ability to transcend his/her ego and political preferences

6. An understanding of and appreciation for the uncertainty of markets

7. A flexible and open mind

8. Utter humility

Now, I could catch some legitimate criticism from those who believe that the path to investment success lies in riding the wave, or the momentum, all the way to its end.

I mean, I totally get the momentum-driven approach to asset management. In fact, when conditions underneath the asset in question justify its positive momentum (as in equities from early ‘09 to late-summer ‘19), I’m totally on board.

However, there’s another momentum that — with other peoples’ fortunes at stake — I feel demands even greater attention/study than does the momentum in price.

That would be the momentum in/direction of the underlying fundamentals.And while, for the moment, underlying fundamentals are taking a back seat (well, they’re presently locked away in the trunk) to headlines and price momentum, I still subscribe to the following profound statement by retired hedge fund manager Colm O’shea.

Like O’shea, I equate the price action by itself more to wind than I do tide. The tide being the fundamentals:

“People get all excited about the price movements, but they completely misunderstand that there is a bigger picture in which those price movements happen. Price movements only have meaning in the context of the fundamental landscape.

To use a sailing analogy, the wind matters, but the tide matters too. If you don’t know what the tide is, and you plan everything based on the wind, you are going to end up crashing into the rocks.”

So, it’s all about Covid, right? I mean, the fundamentals would be fine were it not for Covid, right?

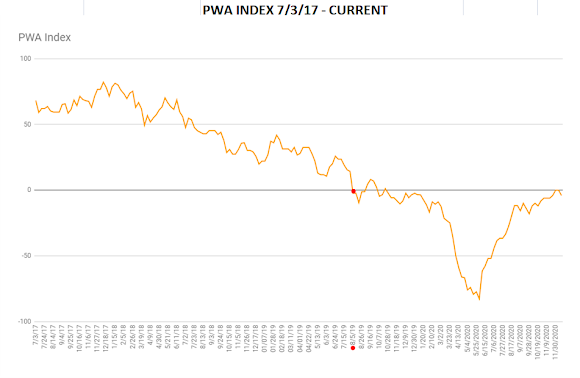

Well, wrong. Our macro index turned red during late-summer 2019, suggesting that the record-long expansion had essentially (fundamentally) run its course.

Clients will recall that during our review meetings at the time, I warned in advance that a thrust higher in stocks may be in the cards; one that we weren’t going to ride in the manner they’d grown accustomed to the previous 10 years.

That thrust would come by way of intervention from the Fed, as I knew that the Fed’s own economists were looking at some of the same data we were.

I.e., in conflict with what chairman Powell was publicly advertising, the Fed’s own quarterly reports pointed to the very fragilities we were pointing to in client meetings and on the blog. Particularly the underlying dynamics in corporate credit…

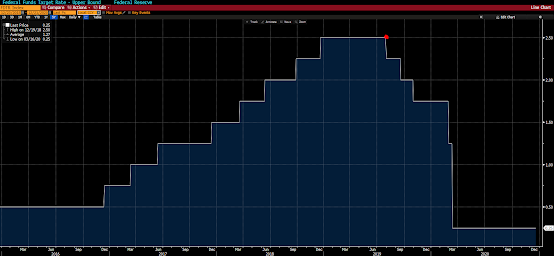

So, yes, amid what was being billed as the greatest economy ever, interest rates were cut (right on cue with our index turning red). And that was long before “Covid” was introduced into the mainstream vernacular.

On 8/5/2019 our index went red for the first time since July 2007 (back-tested):

The Fed’s first of five rate cuts occurred on 7/31/19:

So, why, knowing that the Fed was engaging, would we even think about cutting risk? Which we did at the time, not by selling assets, but by implementing a modified (allows more upside than the base concept) options collar.

Well, that’s a great question, and it’s a doozy of a question for those of us who manage other peoples’ money.

If we were ultimately concerned with always looking good against the market while it’s rising (as I understand most managers are), well then indeed the thing to do would be to back up the truck every time the Fed opens up the spigot.

I mean, later, if/when investors/traders ultimately decide that fundamentals matter, surely our clients would forgive us if we crash with the market, as long as we can show that, say, with our diversification, we captured maybe 80% of the hit.

Well, if that’s a 2008-style hit to stocks, while our clients may indeed forgive us, capturing 80% of a 57% loss would not be something we’d be celebrating internally, I can assure you!

Thus, if we’re ultimately concerned with our clients’ long-term financial well-being, we are absolutely going to take some risk off the table when — despite Fed intervention — conditions demand that we do so.

Of course we then run the risk of underperforming “the market” if it melts higher — amid Fed intervention and despite dangerous fundamentals — and disappointing

for awhile those clients who tether their investment success to the returns of a given stock index.As O’shea stated in the second line of this next quote:

“You have to look at real fundamentals, not at what policy makers want to happen. The willing disbelief of people can carry on for a long time, but eventually it is overwhelmed by the market.”

And in the following, most succinctly:

“After a bull market that goes on for years, who is managing most of the money?

“The managers who are relentlessly bullish and who buy more every time the market goes down will be the ones who end up managing most of the money. So, you shouldn’t expect a big bull market to end in any rational fashion.”

“Because the bulls control most of the money, you should expect the transition to a bear market to be quite slow, but then for the move to be enormous when the turn does happen.

Then the bulls will say, “This makes no sense. This was unforeseeable.” Well, it clearly wasn’t unforeseeable.”

Well, frankly, we strenuously resist being beholden to any benchmark whatsoever, as well as to any innate bias we may have toward the bull or the bear side of the market equation.

I.e., we’re bulls when bullish general conditions dictate, and bears when bearish conditions dictate, and, let’s say, appropriately cautious when conditions are cloudy. (Following the Le Bon quote below is our current posture)

Anything less of us would offer virtually nothing of value to those who entrust their long-term portfolios to our management.

Picking on those “relentlessly bullish” managers, we’d substitute “clients’” for “personal” in the third paragraph of this utterly timeless, and critically important for the investor to understand, 135 year-old quote:

“…the individual forming part of a crowd acquires, solely from numerical considerations, a sentiment of invincible power which allows him to yield to instincts which, had he been alone, he would perforce have kept under restraint.

He will be less disposed to check himself from the consideration that, a crowd being anonymous, and in consequence irresponsible, the sentiment of responsibility which always controls individuals disappears entirely.”

“In a crowd every sentiment and act is contagious, and contagious to such a degree that an individual readily sacrifices his personal interest to the collective interest. This is an aptitude very contrary to his nature, and of which a man is scarcely capable, except when he makes part of a crowd.”

As for the present bull/bear setup, while we see significant underlying risk (that we’ll discuss in Part 3), we nevertheless see some bullish opportunities to exploit — which we’ve begun incrementally expressing in our core portfolio.

Next up we’ll dig deep into global credit markets to illustrate why it’s so important that we keep our wits about us as we navigate the go-forward investing

landscape.