In Part Five I explained the relationship — negative correlation — between commodities prices and the U.S. dollar.

Nearly as notable is the same — on a trend basis — with regard to the dollar and emerging market equities.

Note that much of the production of the world’s commodities takes place within its emerging countries. Therefore, from that angle, indeed, the relationship makes sense.

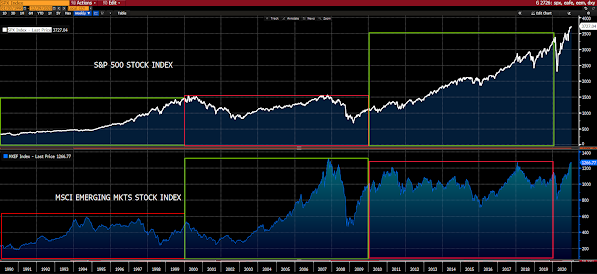

Here’s a 30-year look:

So it’s unquestionably a good idea to own emerging markets stocks in a weak-dollar environment.

Another, I’d argue more important, reason is the fact that, for sustainable economic growth, demographics matter. Big time!

If, at the end of the day, growth opportunities exist where people, and natural resources, exist, and, all-the-more, where populations are growing, and where economic/infrastructure development has some catching up to do relative to the rest of the world — well then, emerging markets, by definition, are literally screaming for smart-minded investors to engage (or to continue/stepup their engagement) in a big way.

Note: For our purposes, we’ll say in a “big(ger)” way than we have the past few years.

Yes, 85% of the world’s population resides in emerging economies. And, by all measures, their populations (from Chile to India to Africa, and so on) are significantly younger than those of developed economies (U.S., Japan, Western & Central Europe, Australia, etc.).

Speaking of these past few years, while this is anything but the basis for a workable investment thesis, it’s been my observation that performance leadership between emerging market and U.S. equities tends to change hands roughly every decade.

Remarkable the flatness (consolidation) in emerging market equities, as a group, during the second decade of the 21st Century.

Although, we can say the same thing about the U.S. (with two historic bear markets along the way) during the 21st Century’s first decade.

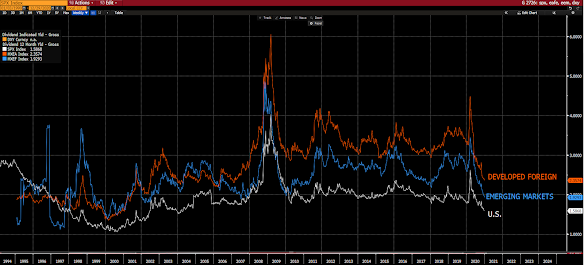

That interesting, yet non-actionable, 10-year performance phenomenon has been the case when comparing developed foreign markets to the U.S. as well:

From a valuation standpoint — looking at price to projected earnings — foreign stocks present a relative bargain:

And from a dividend income standpoint, foreign equities presently offer the investor more for his/her buck there as well:

For any reader who may be at all taken aback by the notion that a good chunk of their portfolios ought to exploit themes outside the U.S., take a look at some of the companies featured in the two foreign indexes presented in the graphs above:

Adidas, Bridgestone, Crown Resorts, Daimler (Mercedes Benz), Electrolux, Toyota, Sony, Honda Motors, Volkswagen, Panasonic, Michelin, Nissan Motors, Novartis, AstraZeneca, Glaxo, Merck, Siemens, Airbus, Kubota, Logitech, Nokia, HSBC, Nestle, Unilever, L’Oréal, Woolworths, Heineken, Ace Hardware Indonesia, Alibaba, Hyundai, Kia Motors, LG Electronics, Ambev, Colgate Palmolive Indonesia, Nestle India, Walmart De Mexico, Siemens LTD, Infosys, Lenovo… to name a few.

While we could devote volumes herein digging into investment prospects region by region, we’ll devote the remainder to a brief look at the unique opportunities developing in the second most populous country in the world, India.

China’s global influence, which is expanding at breakneck speed, is arguably something that the free world should be concerned about, and intently focused on going forward.

India, therefore, being the world’s largest democracy, virtually has to be a huge part of the answer in terms of checking China’s aggressive outreach in the years ahead.

The subcontinent is literally brimming with potential.

It’s population, nearly the size of China’s, is enormous. And, as, again, young growing populations are utterly key to sustainable economic growth, India — with its median age of 28, vs China’s (and ours for that matter) of 38 — possesses a real competitive advantage.

Imagine what a serious manufacturing infrastructure campaign in India might accomplish in terms of taking global market share from the world’s most powerful communist regime.

Imagine the investment opportunities inherent in such a scenario.

Yes, absolutely, the U.S. government should, and I suspect will, make India a top priority in terms of fostering favorable trade arrangements in the coming years.

In fact, per the excerpt below, it appears as though there is a stepping up of supply-chain shifting currently taking place: Apple, for example, recently announced that it plans to shift some of its production from China to India, while other tech firms are working to expand their presence there as well.

Toby Simms, of the UK’s Fidelity International, does a nice job summarizing the opportunities as well as the obstacles present in India’s current setup in his article titled Is there a case to be made for investing in India.

Here are a few snippets:

“…existing trends of better education and increasing urbanisation are expected to continue over the coming decade. Behind them should follow average income and consumption levels.

But there are obstacles in the way. One is the steady stagnation of India’s manufacturing sector. Reforms and investment in infrastructure are needed to boost the sector, increase efficiencies and create further jobs. Many of the foundations have already been laid, and India’s Prime Minister, Narendra Modi, is committed to his ‘Make in India’ initiative, designed to further unleash the country’s potential.”

“…with Covid shifting the makeup of global supply chains, India and its large workforce could attract further attention from foreign companies.

Silicon Valley hasn’t been slow to notice this potential. Earlier this year, Apple announced its plans to shift some of its production lines from China to India, to cater to both export markets and India’s domestic demand. Other Big Tech giants have steadily been building their presence in the country.”

“Of course, this is an emerging market, and as such it could present a riskier investment destination than others. A full recovery from the COVID crisis could take time as well, even with vaccine hopes rising by the day.

But there is an encouraging outlook here, especially when parts of nearby China are starting to look expensive. A combination of favourable demographics, shifting supply lines and reforms designed to encourage growth could make India an attractive proposition for investors looking to diversify their portfolios geographically.”

So, yes, we’re eyeballing India, by itself, as a potential destination for a portion of our emerging markets exposure. It’s presently the third-largest country weighting — accounting for 10% — in our current emerging markets exposure.

My only hesitation is the timing, as Indian equities’ recent runup (reflected in this year’s performance of our emerging mkts ETF [+12.8%]), and their relatively rich valuations, like so many other things of late, fly in the face of present underlying fundamentals:

Definitely wrapping up our year-end letter in Part Eight to come…

We wish you and yours a Safe, Healthy and Happy New Year!