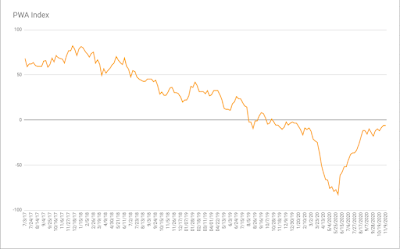

Our proprietary macro index (-6.12) broke even on the week; with two inputs improving, two deteriorating:

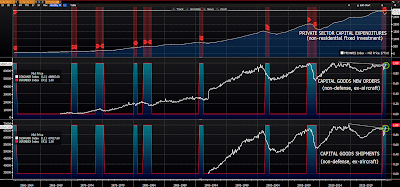

Positive needle-movers…

Capex (business capital expenditures). Rises when companies are buying equipment/expanding capacity (shaded areas denote past recessions):

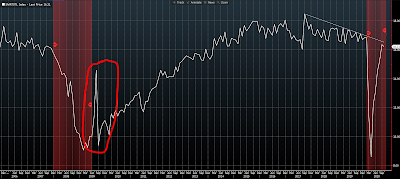

Staples/Discretionary Stock Ratio. Declines when consumer staples stocks (economically defensive) are underperforming consumer discretionary stocks:

Essentially, that (discretionary outperforming staples) is traders anticipating that the companies that produce the goods that folks spend their extra money on are relatively well-positioned going forward. The assumption of course being that folks will have extra money to spend going forward. If the assumption’s correct, then that’s good news.

Negative needle-movers…

Institute for Supply Management (ISM) Non-Manufacturing (services) Index. A gauge of services sector activity and sentiment:

“While the economy is getting better, there is still very much uncertainty about the future. We are putting capital expenditures on hold until we gain additional confidence and certainty.”

“COVID-19 continues to have an effect on supplier support and operations, more from a decreased labor perspective rather than unavailable material.” (Computer & Electronic Products)“Business continues to be robust. Sales are greater than expectations, and cost pressures are modest. There is posturing by suppliers on market price increases for corrugated and polypropylene, yet no firm price increases at this time. We expect a strong finish to 2020 and a solid start in 2021.” (Chemical Products)“Sales continue to be strong — up 4 percent this September compared to September 2019. The year-to-date level is still 21 percent below last year due to the [COVID-19] shutdown, but sales are stronger than expected and forecast to stay strong through the first quarter of 2021.” (Transportation Equipment)“Increased production due to stores stocking up for the second wave of COVID-19.” (Food, Beverage & Tobacco Products)“Continue to see increases in customer demand. We still are not back to pre-COVID-19 levels but are continually improving.” (Fabricated Metal Products)“Construction materials have leveled off but continue to be at an all-time high. Mills for board sheet stock have pushed out lead times citing increasing backlogs related to the pandemic and increased supply in the housing market.” (Furniture & Related Products)“Business is almost back to normal levels; however, customers are still cautious with capital spending.” (Machinery)“Business levels have just about returned to pre-COVID-19 levels. Our company is remaining conservative with fixed-cost spending, knowing the uncertainties that lie ahead with COVID-19 and its potential impact globally.” (Miscellaneous Manufacturing)“October order books are the strongest we have seen in the past six months.” (Paper Products)“We continue to see stronger month-over-month orders in plastic injection molding.” (Plastics & Rubber Products)

Silenced by more pressing issues yesterday was ADP’s private payrolls report (the private sector’s report on employment conditions), which showed 365k new jobs created in October, compared to an estimate of 643k. That’s what you call a miss. Goods producers saw merely 17k new jobs created. That would be another hint that the stimulus-fueled surge off the depths may be losing some steam. Friday we’ll get the government’s number.

This morning’s weekly initial jobless claims report came in at 751k vs a 735k estimate. 7.29 million folks remain on the unemployment rolls, which is down from 7.82 million the previous week.

There are also the special additional programs titled “Pandemic Emergency Unemployment Compensation” and “Pandemic Unemployment Assistance.” The former rose to a new high of 3.96 million folks, the latter declined to 9.33 million. All told, over 20 million people remain on unemployment.