Well, for the first time since October 2019 our PWA Macro Index is out of the red. Can’t quite say “in the green”, since it presently scores a 0. But what a rebound off of a -82.69 back in June!

Now, before we release the pigeons we have to remain cognizant of the reality that merely 29% of the data points we track presently earn a positive score, while 29% score negative and 42% neutral. And, as I’ve stressed herein of late, some of the negatives are turning more so (jobless claims, for one example, rose again this week)…

This weeks pluses…

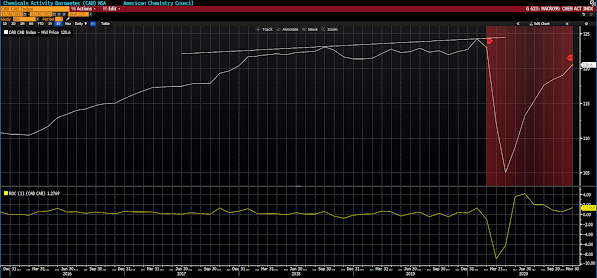

The Chemical Activity Index (nice to see this one turn back up!):

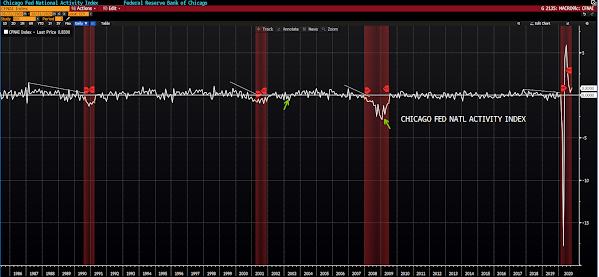

Chicago Fed National Activity Index:

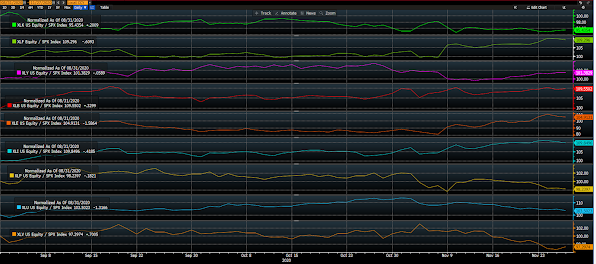

Sector/SP500 Equity Performance Ratios. Cyclical sectors, save for tech, currently outperforming the S&P:

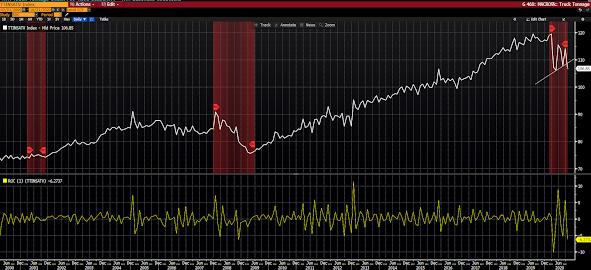

Staples/Discretionary Performance Ratio:

This week’s minuses:

Personal Income (speaks to the nature of the rebound; income declining as government transfer payments abate):

Truck Tonnage:

“The bull-bear spread is again in the danger zone, at +41.4%, up from +39.8% last issue. That exceeds the +40.4% reading three weeks ago.

Late Aug the difference hit +45.1%, the widest spread since Jan-2018 when it exceeded 50%! Above +30% counts show more risk the higher they get, with defensive measures appropriate above 40%.

Prior to +41.5% difference in Jan this year we saw a +43.2% spread late Sep-18, just before the S&P 500 corrected 19.7% to its Christmas Eve low that year.”

Here I placed a red circle on an S&P 500 graph at each of the highlighted +40% bull/bear spread dates referenced above: