I think it’s safe to say that history has never concluded a setup like the current without seeing stocks suffer a significant, protracted bear market in the process (the Feb/March experience btw doesn’t come close). So the question has to be, how does one manage a portfolio amid historic certainty that before the next true expansion or bull market gets underway stocks will experience major, extended losses?

Problem being one of timing, and one of the inherent uncertainty of “historic certainty”. I.e., market history typically rhymes, but it never precisely repeats — to paraphrase one of history’s great phrasers.

I mean, maybe infinite money printing and government borrowing and spending can indeed save the stock market’s day this go-round…

In our view, all one can (or should) do — one who sees forests through trees, that is — is dispense with the messy and profoundly futile business of market forecasting, while forever and painstakingly assessing the prevailing risk/reward setup and investing accordingly.

Which to us — along with hedging crash risk — means, at this juncture, recognizing, crash or not, how the powers-that-be will attempt to manage their way out of what is the greatest debt bubble in the history of mankind.

Well, as the present crisis — and all past modern-day crises for that matter — so vividly illustrates, the powers-that-be know of only one method of “managing” crises — print, borrow and spend money, while cutting interest rates to the bone.

A weak dollar regime — assuming they can sustainably fend off the effects of trillions of dollar-denominated foreign-held debt, and hold interest rates at bay — is therefore to be expected. Couple that with what will certainly be attendant yield curve control (i.e., capped treasury market interest rates), and seemingly obvious investible themes emerge. Gold is the ultimate no-brainer under such a scenario — its at times extreme volatility notwithstanding. Other commodities such as agriculture are likely to do well under such a setup as well.

New government spending will largely focus on infrastructure. The outcome of the coming election will determine the extent to which we invest in traditional infrastructure plays vs those catering to a more environmentally-focused regime.

We’ll keep you posted as our core allocation evolves to fit our evolving thesis in the months to come…

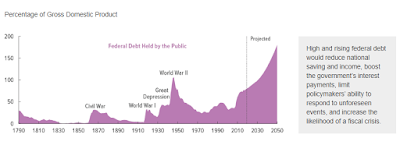

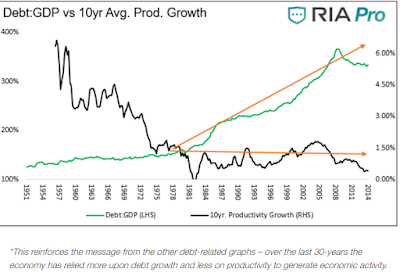

As for the fundamental long-term challenges around “the greatest debt bubble” ever, well, they’re daunting.

We’ll scratch that surface, visually, by pulling from my “Charts That Trouble Me” file:

Q3 was the worst Q3 ever for bankruptcies:

“In fiscal year 2019, the federal government spent $4.4 trillion, amounting to 21 percent of the nation’s gross domestic product (GDP). Of that $4.4 trillion, over $3.5 trillion was financed by federal revenues. The remaining amount ($984 billion) was financed by borrowing. As the chart below shows, three major areas of spending make up the majority of the budget:

- Social Security

- Medicare, Medicaid, CHIP, and marketplace subsidies

- Defense and international security assistance

Two other categories together account for less than a fifth of spending:

- Safety Net Programs

- Interest on Debt

“

“

“Stay tuned…

Marty