Optimism over US fiscal stimulus prospects and positive commentary around the President’s present condition is overcoming news of re-lockdowns in New York City, Spain, France, UK and the Czech Republic as global markets get underway this week.

All but 3 of the 16 Asian markets we track closed higher overnight. All but 2 of the 19 European bourses we follow are heading higher this morning, while US major averages are green across the board: Dow up 272 points (0.99%), S&P 500 up 1.14%, Nasdaq up 1.52%, Russell 2000 up 1.30%.

The VIX (SP500 implied volatility), on the other hand, up 3.66%, has the options market pricing in trouble. Although VXN (Nasdaq vol) isn’t confirming that signal with regard primarily to tech stocks, down -0.03%.

Oil futures are up a whopping 5.51%, gold’s up 0.54%, silver’s up 1.74%, copper futures (bucking the bullish trend) continue to tank, down -1.31%, and the ag complex is up 0.22% as I type.

The 10-year treasury is taking a beating this morning (yield higher), and the dollar is providing a nice tailwind for risk assets, down -0.49%.

Hampered only by slight declines in utility stocks and the yen, our core mix is up 0.83% as I type. Silver, materials, banks, industrials and tech lead the way.

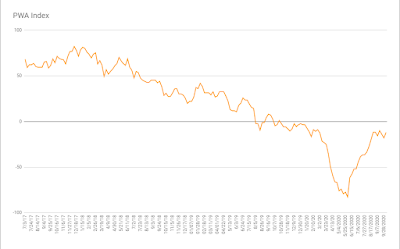

Having disconnected myself from late last week to last evening, I wasn’t able to produce the usual Friday macro update. Did, however, score our index last night. Summarizing the results for you below.

The PWA Index gained 6 points, taking our overall net score to -12.