As I type the Nasdaq 100 Index (read tech) is staging one heck of a rally, up 3.21% on the day thus far (although giving a bit back the past hour or so):

15-minute chart:

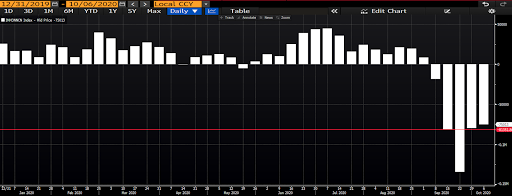

Part of our weekly exercise involves tracking the net positioning of futures speculators across a number of indices and commodities.

Here’s the latest positioning among those who speculate in Nasdaq 100 Index futures:

So what does that tell us? Well, it tells us that, save for a little ambiguity back in May, futures speculators were betting on higher tech stocks all year, up until September that is. Then they flipped in a big way. I.e., they went from net long (betting on more upside) to big net short (betting on big downside).

Hence, the short squeeze phenomenon I’ve written much about herein over the course of this year (but in the S&P). I.e., to be short stocks means to have sold borrowed shares that you expect to replace later at a lower price, while pocketing the difference. There’s only one thing there for certain, that you’ll have to replace those stocks. If, alas, the price is higher than what you originally sold them for you lose. The higher they go the more you lose…

So, when the price moves against you, you cover (you buy). And when there are lots of yous out there, the price of the shorted item can scream higher simply on you and your fellow yous covering.

Yes, that’s indeed playing out in today’s move…

Another big rally occurring (to the tune of 6.17%) today is in VXN, which tracks the implied volatility in Nasdaq 100 Index options.

Talk about your contrary indicators! This says options traders are, at the moment, thinking that the shorts actually may have had it right after all… As implied volatility tends to correlate most negatively to the underlying security’s price action…

I.e., typically, the Nasdaq 100 would be tanking with VXN up over 6%. One will no doubt be giving way as the week unfolds…