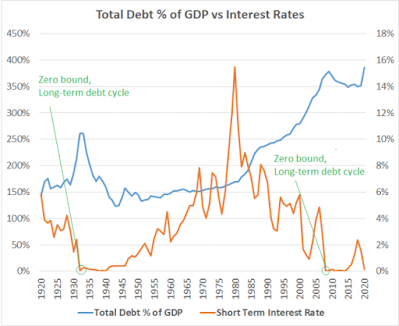

The case that inflation will, via official metrics, remain nowhere to be found is rooted in the economic constraints endemic in today’s record high debt, strained general conditions (there’ll be a lengthy recession overhang), demographics and technological advancements.

The inflation is coming narrative, on the other hand, contends that massive fiscal injections — with the pain of covid, the continuing rise of inequality, the trend in deglobalization, and continued economic weakness offering huge political cover — will come in such enormous quantity, against a Fed that will continue to suppress borrowing rates (effectively mitigating any rising-rate headwind against inflation), that rising inflation will be virtually impossible to avoid.

As I’ve previously stated herein,

“…the Fed’s new approach to potential inflation — let it run hotter — is, contrary to popular opinion, not about their desire to inspire inflation via “forward guidance”, but to give themselves the wherewithal to not address it with higher interest rates if/when it ultimately exceeds the point where their old commitment would’ve had them doing so.

I.e., imagine the Fed hiking rates amid history’s greatest debt bubble when their decades-long practice of bailing out otherwise failed institutions, not to mention rescuing egregiously careless hedge funds and private equity firms (this go round), coupled with financial repression, leaves them with virtually no choice but to in fact inflate the debt away via the printing press.”

Therefore, beyond the election, and as we enter 2021, we may very well be adding exposures in areas such as materials and industrial equities to exploit targeted spending regimes, while managing a healthy mix of commodities and foreign equities to take advantage of what will highly likely turn out to be a protracted weak-dollar environment.

Now, that said, while high government spending amid a zero interest rate environment makes for an intuitively bullish backdrop, it’s of course never that easy.

Bottom line; while the future will no doubt present opportunities for the experienced, thoughtful, prudent maco-focused investor, real risk will permeate the global landscape well into the foreseeable future. Thus, as we’ll look to take full advantage of whatever opportunities lie in store, we expect we’ll be maintaining an active hedging strategy all along the way…