All of this week’s data reports that flow to our proprietary macro index have been released, allowing me to score our index a day early. Just finished, here’s a recap:

As I got down to the last few charts it occurred to me that I may have nothing — in terms of component score changes — to report this week. Then I came to the Staples/Discretionary ratio; which compares the performance of consumer staples stocks (think groceries) and consumer discretionary stocks (think cruise lines).

A rising line means staples are outperforming discretionary stocks, a declining line means the opposite (1-year graph):

Note the green circle where the ratio broke below the upward-sloping trend line, which was about at the break even point for the year. That means that staples stocks — after last week threatening to recapture that trend line — relative to discretionary stocks turned south. Which says good things about the state of the consumer from the market’s perspective (i.e., anticipating that they’ll continue to spend money on fun stuff); adding a net +1 to our index. The overall score improved by 1.78 points to -8.93; the 18th straight week below zero:

Of course “good things about the state of the consumer” are what we’ve been reporting consistently herein. Problem is, as we’ve also been reporting, areas that speak to how the consumer may feel a few months from now are showing some weakness.

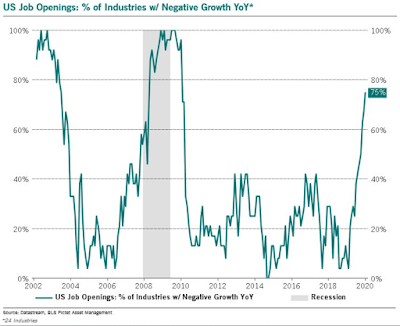

This such as:

The % of U.S. industries (75%) experiencing negative jobs growth:

And declining job openings — at an accelerated pace (rate of change in second panel):

A client asked me this afternoon if I felt that the powers-that-be could successfully keep the market propped up during this election year?

I suggested that the Fed, but not for political reasons, in particular has clearly succeeded thus far. However, their best efforts have unfortunately produced very little in terms of tangibly positive results of late in the real economy.

While higher stock prices are nice, for institutions they don’t pay the rent (although they can make borrowing to pay the rent a bit easier), nor do they pay the salaries of their employees. I reminded her that 2000 and 2008 were election years as well, and they produced stock market returns of -10% and -41% respectively. By the way, 2000 was the first year of a bear market that took stocks down ~50%, while 2008 ushered in a -57% blood bath!

Sadly — and this is not a prediction, just an assessment of general conditions — an uncomfortable array of factors line up in today’s environment much like they did in the months leading into those past two bear markets.

Again, I make no prediction. There are always multiple potential outcomes to any set of circumstances. The best we can do is know where we are in the cycle and act accordingly.

As for our global macro scores; of the 22 countries, plus the Eurozone, that we track, 7 saw conditions deteriorate, 2 improved and 14 stayed the same week-over-week:

Make no mistake folks, given that the data flowing to our individual country indices still predates the worst (thus far) of the coronavirus outbreak, there’s significantly more red to come.

I have no doubt that markets the world over — many already grappling with fragile fundamentals — will begin pricing in more economic pain as a result of the virus. I also have no doubt that we’ll continue to see massive, across the board stimulus from central banks and governments. Think of it as a pulling forward of years of potential future stimulus, with all of the debt and misallocation of resources that comes with it. I know, not pleasant to think about.

As I implied above, we can’t know how the future will unfold, but we can crunch the data as it comes in, we can assess the composition and complexion of leverage in the system, and we can stack the present up against the past and estimate where we stand in the economic cycle.

In a nutshell, we dive to extreme depths to develop our assessment of the prevailing risk/reward setup. And, as you’ve gathered, we believe strongly that present conditions warrant a cautious approach to the management of client portfolios.

Have a great weekend!

Marty