Here’s a recap of this week’s macro analysis:

Our PWA Macro Index contracted slightly this week, dropping 3.57 points to an overall score of -12.50; its 19th consecutive week in the red.

Two data points — weekly jobless claims and the staples/discretionary stocks ratio — went from positive (+1) to neutral (0). No other indicators moved enough to change color this week.

While jobless claims remain at historically low levels, it’s all about trend; and when it comes to the labor market, recessions tend to follow negative trend-changes soon after they develop.

Click each insert below to enlarge…

New claims:

Same look for continuing claims:

Last week we highlighted the positive score change in the staples/discretionary stocks ratio. This week saw a reversal and a recapturing of the previously established uptrend:

While the above components now flashing neutral has our attention, this week’s scoring of our financial stress index has us troubled.

As we’ve discussed and illustrated herein, big recessions and bear markets are generally characterized by trouble in the credit markets. And, alas, we see a growing bubble in corporate debt that has inflated to the point where we’re finding it hard to imagine a resolution that doesn’t ultimately involve a wave of defaults rippling through the broad economy.

We designed our financial stress index to deliver signals when trouble’s brewing in the global credit markets. One component of the index is the pricing of credit default swaps (CDS), which are essentially insurance contracts against bond defaults: Premiums rise as default risk rises.

While the following graphs will likely leave you wondering why we only adjusted our CDS score from positive to neutral, as opposed to negative, the actual levels are not yet near historical highs. However, the sharp spikes higher are definitely concerning enough to move the needle on our index.

Here’s the 1-month graph of CDS spreads for U.S. investment-grade corporate bonds:

Here’s for European investment-grade bonds:

European high yield bonds:

Japanese investment-grade:

Asia ex-Japan investment-grade:

Another component of our stress index is what’s called the “high yield credit spread”; which is simply the difference in yield between 10-year junk bonds and 10-year treasuries. A rise in the spread denotes growing trouble in the lower-rated bond space, as investors perceive the heightened risk and, therefore, demand a higher rate of return relative to government-backed treasury bonds.The spread saw a fairly sharp increase over the past week that has it also moving from positive (+1) to neutral (0) in our index.

Our financial stress index’s overall score declined 66.67 points, coming in at 0 this week. Make no mistake, this is the stuff of insomnia for Fed officials!

As for the rest of the world, we’ve created 23 additional indexes (the Eurozone in the aggregate plus 22 individual countries) to give us a feel for macro conditions outside the U.S.

As I suggested last week, we’re in for some ugly prints as data roll in that reflect the economic impact of the coronavirus COVID-19.

There weren’t a great number of new releases for the data we track this week, but what there was resulted in declining scores in 7 countries; no countries improved on the week:

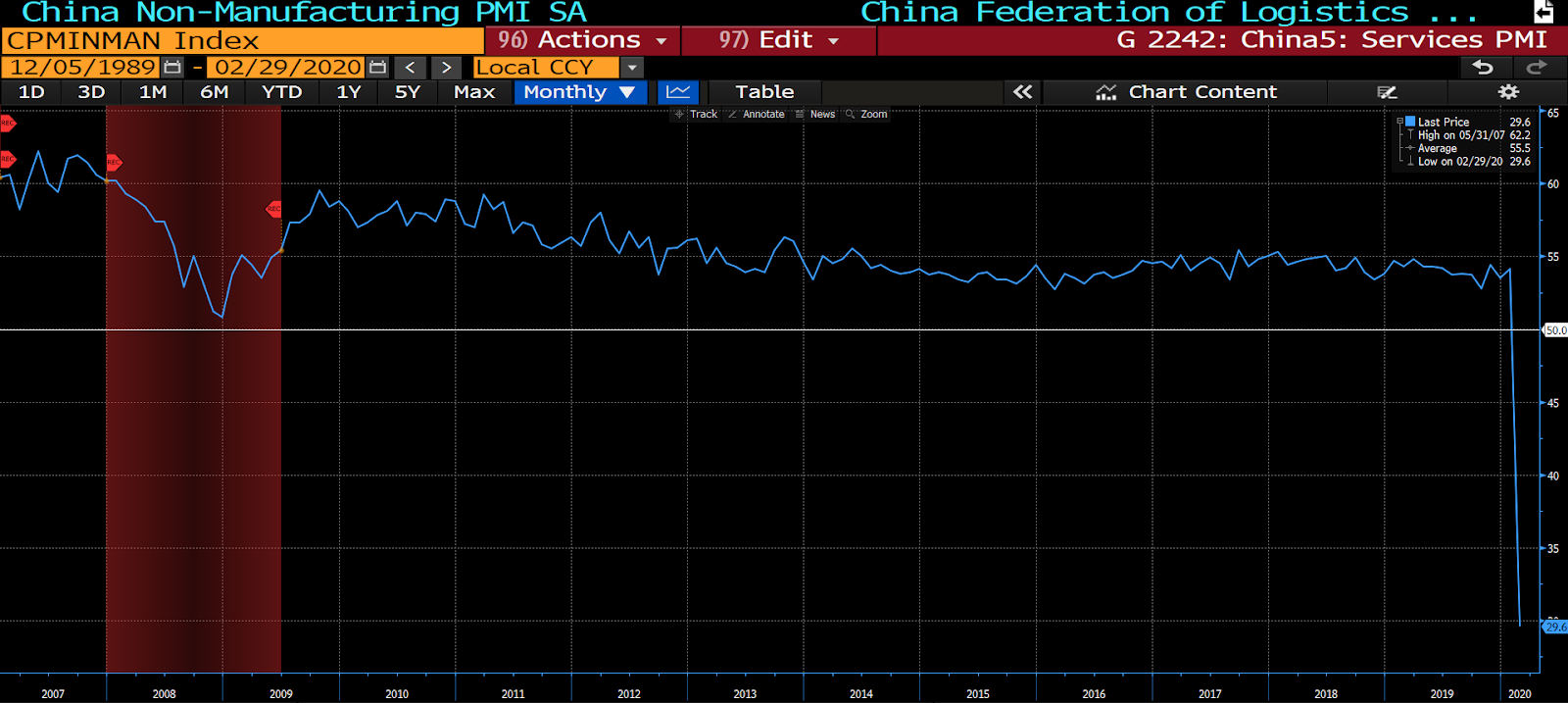

To get a feel for what to expect as more data come in reflecting the effects of COVID-19, take a look at China’s manufacturing and services sectors purchasing managers indices, both released last evening:

China Manufacturing PMI:

China Services PMI:

Those are the worst scores in the history of each survey!

A recession in the world’s second-largest economy is a virtual given at this point, and that’s a problem.

Yes, this week’s stock market drubbing made perfect sense.

And yes, you should expect sharp, central bank-induced rallies to ensue. And, no, barring any fundamentally-positive developments to go with them, they should not — at this juncture — inspire you.

And yes, you should expect sharp, central bank-induced rallies to ensue. And, no, barring any fundamentally-positive developments to go with them, they should not — at this juncture — inspire you.

We’ll keep you posted…