Listening to Bloomberg Asia last evening I caught a segment where Bloomberg’s reporter, after referencing the IMFs latest downgrade of global growth (they estimate that “90% of the world will experience a growth slowdown this year”) and the Brookings Institute characterizing present global general conditions as a “synchronized stagnation”, accurately listed the plethora of global headwinds that he suggests virtually have to “entrench a period of gloom”.

His guest, Principal Global Investors’ (a subsidiary of my employer for the first 23 years of my career by the way) executive director, responded with a laudation of the amazing resiliency of the market in the face of what any thoughtful economist or analyst would have to describe as palpable global uncertainty. He went on to make his bullish case for stocks with an emphasis on the enormous amount of cash that sits idle on the sidelines; presumably destined to come roaring into the stock market on the first sign of stability.

Well, I must confess, over the years I have heard myself make that very same case on many an occasion. And the fact of the matter is, the gentleman is absolutely right; in terms of there being a ton of cash sloshing around out there.

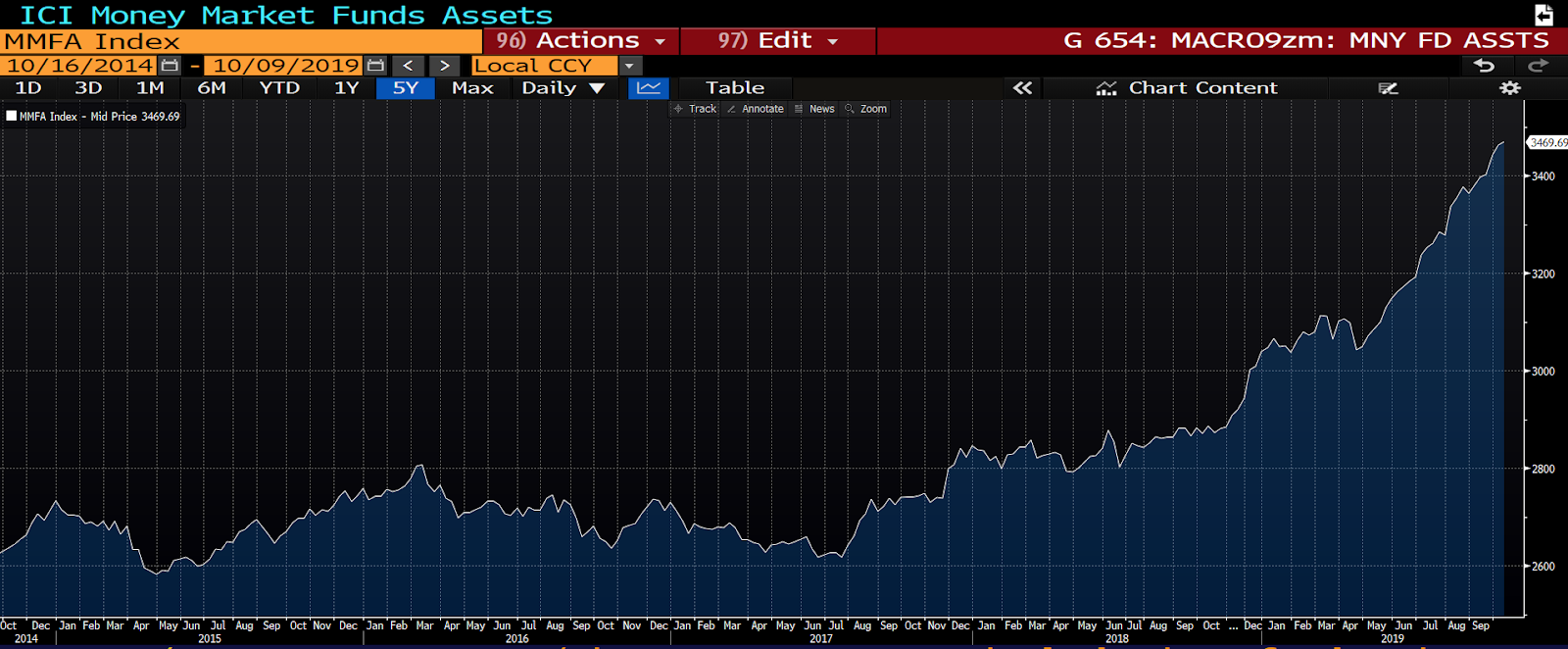

5-year graph of money market fund assets: click to enlarge…

The above chart speaks loudly to his case. And, make no mistake, that’s a legitimate case to make: Again, we’re looking at some serious cash that can indeed buy stocks if its owners ultimately decide that that’s its best use.

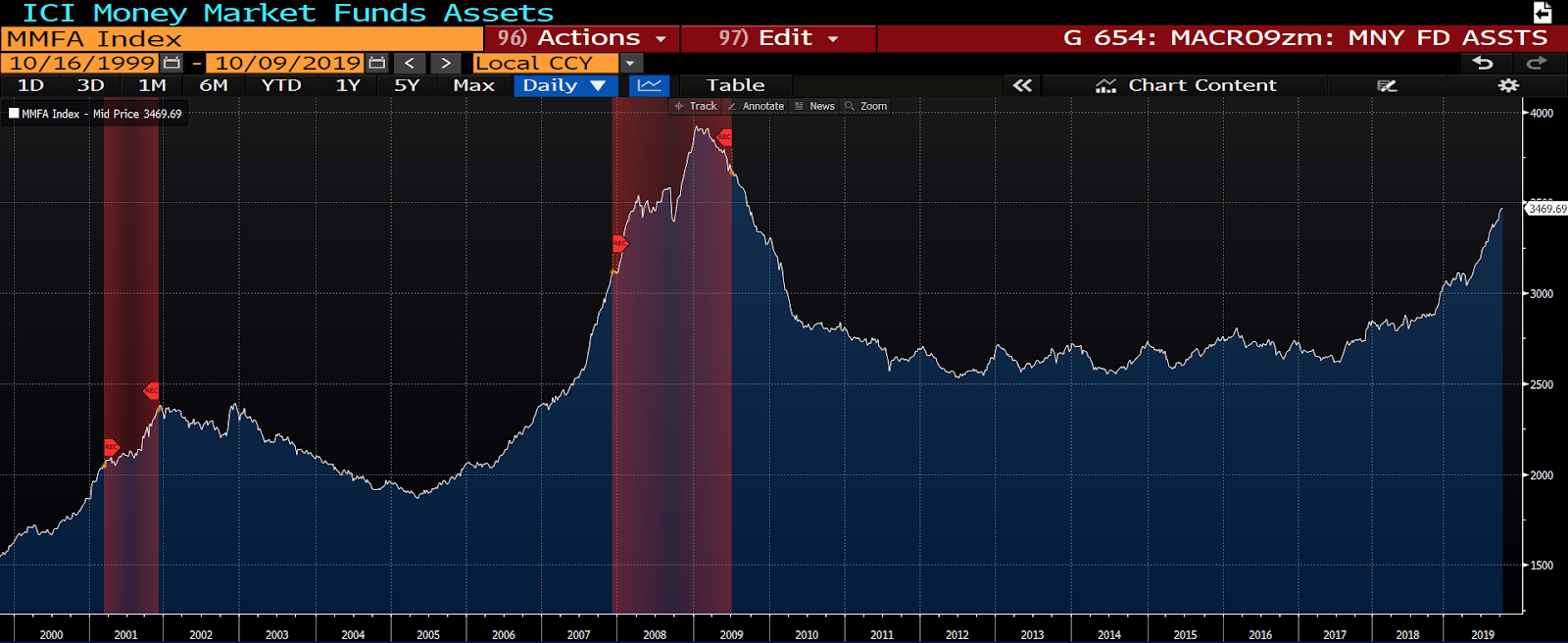

There is, however, another angle from which to view the above. Or, I should say, there’s another (higher) elevation (longer time frame) from which we should view the graph before concluding that it’s unambiguously bullish.

20-year graph of money market fund assets (last two recessions in red):

Clearly, it’s all about the conditions under which cash is being hoarded.

If indeed the current trajectory in money fund assets leads right into the next recession, well, per the next graph, it’s likely to be quite some time before stocks become the next serious (or sustained) destination of choice.

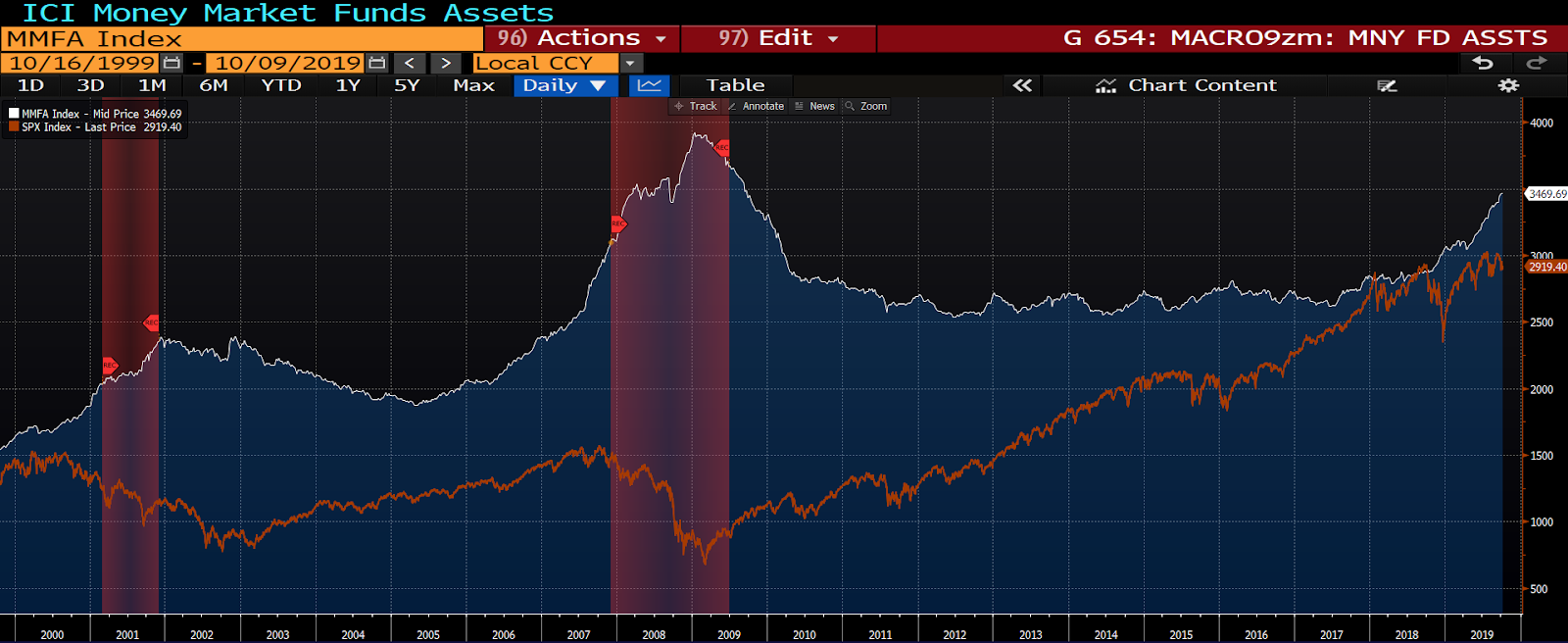

S&P 500 layered in:

Okay, so we have this palpably uncertain global backdrop, we have money market funds bulging like there’s no tomorrow (or like there’s a recession coming tomorrow), and nevertheless we have stocks parked within a stone’s throw of their all time highs!?!

So what gives?

Well, that’s the question!

While I suspect that there are more than a couple legitimate answers, I’ll offer up a couple that — given present circumstances — make sense to me:

1. Long-term tops — if that’s indeed what this finally (after 10+ years of rising stock prices) is — are always messy. They start with the data rolling over, followed by policy-maker-panic (the proverbial kitchen sink of monetary and fiscal stimulus) which sucks in unsuspecting late-comers who — believing that central bankers and politicians will save the day — push stocks to new marginal highs, only to have the smart money sell into those rallies before reality shows up in the form of corporate cutbacks, job losses, debt defaults, and so on: I.e., before recession, and the attendant bear market in stocks, sets in.

Or,

2. Traders are simply unwilling to abandon stocks while they still believe that logic will prevail with regard to the two biggies in terms of geopolitical headwinds; the US/China trade war and Brexit. Clearly, based on the patterns in trading we’re witnessing on the headlines and the tweets, a positive resolution in either, or both, will be good for a serious rally in equities.

Of course, depending on macro conditions if/when such resolution(s) occur, the subsequent rally(ies) could turn out to be that last thrust to new highs before the reality I mentioned in answer #1 sets in — as opposed to the beginning of yet another extension of the longest bull market in history (which, by the way, shouldn’t be dismissed out of hand [again, it’ll depend on conditions at the time]).

In either event, general conditions are presently as strained as we’ve seen them throughout this entire epic bull market. And, as we’ve pointed out for months herein, that straining is largely due to global trade uncertainty.

While we’re yet to enter the next recession, our view is that we’re getting too close for comfort, and, therefore, if — in particular — resolution (that eliminates all associated tariffs) to the China dispute doesn’t come soon, accompanied by a commitment to not incite similar disputes with our other trading partners, we will indeed see the next recession and its attendant bear market in stocks sooner than we otherwise would have.

Thus, market rallies and near-term new highs (which we fully expect to see) notwithstanding, we hedge until the smoke clears…