Cass Information Systems’ monthly Freight Index Report is widely followed and respected because, simply put:

“….since the end of World War II (the period for which we have reliable data) there has never been an economic contraction without there first being a contraction in freight flows.”

As I read the first two bullet points (I highly recommend a reading of the entire report for those who like getting into the global economic weeds [although I must warn you, it won’t leave you feeling good about current conditions]) of the August report this morning it occurred to me that Cass’s analysts’ evolving view of economic conditions during the course of 2019 pretty much lines up with ours.

Here they are:

- When the December 2018 Cass Shipments Index was negative for the first time in 24 months, we dismissed the decline as reflective of a tough comparison. In January and February 2019, we again made rationalizations. When March was also negative (-1.0%), we warned that we were preparing to “change tack” in our outlook; when April was down (-3.2%), we said, “we see material and growing downside risk to the economic outlook.”

- With the -3.0% drop in August, following the -5.9% drop in July, -5.3% drop in June, and the -6.0% drop in May, we repeat our message from last three months: the shipments index has gone from “warning of a potential slowdown” to “signaling an economic contraction.”

In terms of our views lining up (sticking with Cass’s featured timeline above), here’s from a January blog post:

“As I said in this week’s video, the underlying current (general conditions) is still moving in the direction of expansion (albeit slower than even a few months ago)…”

Here’s from one in February:

“The housing sector, via XHB, the S&P Homebuilders ETF (which, in addition to the homebuilder stocks, includes names like Owens Corning, Whirlpool, Home Depot and Lowes) is offering zero support for anyone who thinks our consumer-driven economy is teetering on the edge of the next recession.”

Here’s from a March one:

“Make no mistake, if indeed we’re not nearing the end of this unique bout of protectionism, the global economy, and equity markets, will have a very tough time of it going forward.”

“Bottom line for now: A generally okay macro backdrop, decent valuations, sufficient pessimism (potential market fuel), and amazingly dovish central banks sets a nice stage for stock market performance going forward.”

From April:

“Beneath the relative calm of year-to-date gains, record levels and positive earnings results, there lies the potential for huge global disruptions…”

“…there’s not much underpinning the current expansion beyond the consumer and the Fed; a steep correction could indeed tip the economy into recession if it sends the consumer into hiding.”

And here’s from last week:

“As I’ve pounded herein, and on the videos, the long-term technical setup looks too much like pre-recessionary/bear market periods, to, when coupled with a weakening macro trend, allow for anything but a relatively cautious approach to investing at this juncture.”

The remaining three of the report’s opening bullet points essentially sum up its conclusions:

- We acknowledge that: all of these negative percentages are against extremely tough comparisons, and the Cass Shipments Index has gone negative before without being followed by a negative GDP. However, weakness in demand is being seen across most modes of transportation, both domestically and internationally, with many experiencing increases in the rates of decline.

- We know that freight flows are a leading indicator, so by definition there is a lag between what they are predicting and when the outcome is reported. Nevertheless, we see a growing risk that GDP will go negative by year’s end.

- The weakness in spot market pricing for many transportation services, especially trucking, is consistent with the negative Cass Shipments Index and, along with airfreight and railroad volume data, strengthens our concerns about the economy and the risk of ongoing trade policy disputes. Weakness in commodity prices, and the ongoing decline in interest rates, have all joined the chorus of signals calling for an economic contraction.

Back to our analysis: While transportation is an important component in our proprietary macro index (includes truck tonnage, rail traffic, and the Cass Shipping and Expenditures Indexes), there are another 82 inputs that include consumer and business data, economic stress markers, and a host of financial market indicators. And while I indeed sympathize with the findings in the August Cass Report, our assessment, while notably concerning, doesn’t leave us quite as dire in our outlook. I.e., we don’t see negative GDP by year’s end; however we do by, say, this time next year if present trends remain intact — so I guess we’re close.

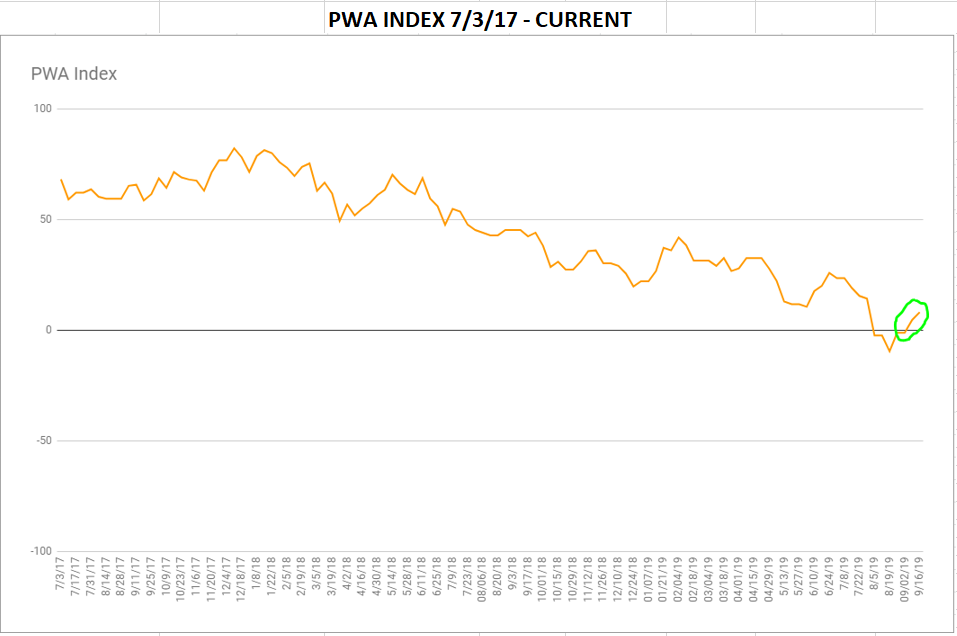

This week our index posted its second consecutive positive overall result (after suffering 5 straight weeks in the red). However, just like last week, the financial markets subindex — with a 22.73-point increase — single-handedly kept our macro score in the green (albeit slightly), while the economic subindex declined to a still-positive +7.41 (down 3.7 points on the week).

As for the gain in our financial markets subindex; it was the result of a nearly across-the-board improvement in stock market breadth.

As for the hit to our economic subindex; deterioration in the latest consumer debt numbers, rail traffic and the Baltic Dry Index (commodity-related) were the culprits.

Bottom line: While we’re not yet ready to hit the exits, when we square what is clearly a weakening macro backdrop

PWA Index

with technical equity market setups that resemble those leading into bear markets past,

S&P 500 Weekly Chart

S&P 500 Monthly Chart

we think a bit of portfolio hedging makes very good sense right here.

Have a nice weekend!

Marty