As I continue to stress herein, our presently cautious stance stems from our assessment of conditions, both technically (the market/asset class trends) and fundamentally (from a macro economic perspective).

emphasis mine…

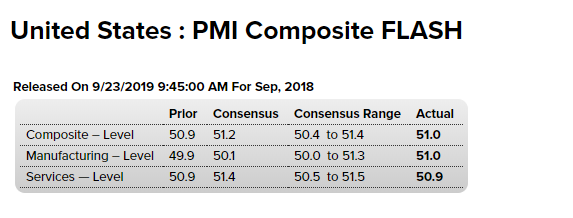

Highlights

Nearly flat are the results of both September’s manufacturing PMI, at 51.0, and services PMI, 50.9. The composite for the month is 51.0 and little changed from August’s 51.2 in a two-month stretch that is the weakest for these data in more than three years.

And the outlook for October’s activity isn’t favorable based on new business growth which, despite an uptick for the manufacturing sample that was, however, offset by services, is at record lows for this report where data go back about 10 years.

Companies can keep up activity like production, at least for a time, by working down backlog orders which they are doing in these samples. Low backlogs are a negative for employment which the report notes saw cutbacks. In fact, indications from the samples, for the first time in nearly 10 years, point to contraction in September private payrolls. A small plus is a slight pick up in business expectations which, nevertheless, remain near seven year lows. Confirmation of weakness comes from prices which contracted for inputs, especially in the service sector, and were unchanged for selling prices.

The report notes that export orders for the manufacturing sample continue to weaken, a reminder that slowing global demand has been holding down the US factory sector and appears to be spilling into services and holding this sector down as well.

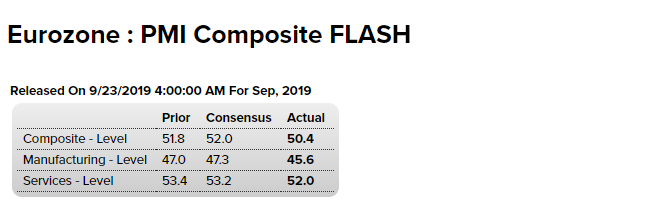

Highlights

September looks likely to have provided a disappointingly weak end to third quarter business activity. The flash composite output index weighed in at just 50.4, well down from its final 51.9 post in August and even further short of market expectations. This points to the slowest economic growth in some seventy-five months.

The headline decline reflected worsening conditions in both manufacturing and services. The flash PMI for the former sunk from August’s final 47.0 to a lowly 45.6, an 83-month trough. At 52.0, its services counterpart was at least still on the right side of the 50-expansion threshold but also comfortably below its 53.5 final August print and an 8-month low.

Manufacturing output (46.0) saw its worst performance in eighty-one months and prospects of any near-term rebound look less than slim as new orders recorded another substantial decline. New business in services edged higher but overall, orders were down for the first time in eight months. Moreover, both sectors saw another drop in backlogs which, at the aggregate level, was the sharpest since November 2014. One of the few bright spots was (again) employment which continued to expand. However, even then, the increase in headcount was the smallest in fifty-six months. Expectations for the year ahead were only marginally higher than in August and so remained at one of the lowest levels since 2012.

Meanwhile inflation pressures eased further. Input costs saw their smallest increase in more than two years and output prices edged just fractionally higher.

Regionally, both core countries noted a sharp slowdown in business activity rates. Hence, the flash composite output index in France (51.3) hit a 4-month low and in Germany (49.1) an 83-month tough. The rest of the euro area also saw growth soften, hitting its weakest point since November 2013.

Today’s results simply underscore the need for the ECB easing package announced earlier in the month. Indeed, with further signs of a decelerating services sector, for some time the key prop for overall Eurozone economic growth, real GDP will do well to keep its head above water this quarter.