President Trump’s top economic adviser Larry Kudlow did his job well as he made the rounds this morning.

His message being that strong retail sales and low unemployment prove that there’s no recession in sight:

“Trump’s top economic advisor Larry Kudlow said Sunday strong retail sales and low unemployment were signs the economy remained strong.”

The President’s trade adviser Peter Navarro was also out and about today. He echoed Kudlow’s messaging on the economy while touting his 20 years of economic forecasting as he assured Americans that their economy will remain strong and stocks will remain in bull mode through 2020. He also said that the yield curve didn’t actually invert last week (huh?? I actually watched it invert):

The yield on the benchmark 10-year Treasury note briefly fell below the 2-year rate on Wednesday, a phenomenon in the bond market known as yield curve inversion, which is typically taken as a sign that a recession is on the horizon. Navarro, however, disputed this: “Technically, we did not have a yield curve inversion,” he said in an interview on CNN.

Mr. Navarro went on to say that it wasn’t technically an inverted yield curve because it essentially didn’t invert by very much. Well, “technically”, it is absolutely an inverted yield curve the second the 10-yr yield drops by even the tiniest % below the 2-yr. I guess he’s suggesting that it’s not meaningful unless it goes deeper and stays longer, and, frankly, I think that’s a legitimate position.

Okay, so, as I stated recently, we absolutely have to do our own economic analysis. Whether we’re talking political appointees or Wall Street wiz’s, every institutional economist has what I’ll call his or her institutional bias. Even your academics have their biases, as they generally subscribe to some dogma, be it Keynesian, Classical Liberal, and so on.

So what’s my bias? Well, I like to think that I’m biased toward reality. Managing other peoples monies means that I have to see the world as it is, not how I might like it to be.

With seeing-the-world-as-it-is in mind, let’s explore Mr. Kudlow’s assertion that there’s no recession in sight based on the fact that retail sales are up and that unemployment is down.

The fact that both of those are components in our proprietary macro index makes me intimately aware of their present levels, their present trends, and how they tend to trend prior to recessions.

CLICK ANY INSERT BELOW TO ENLARGE…

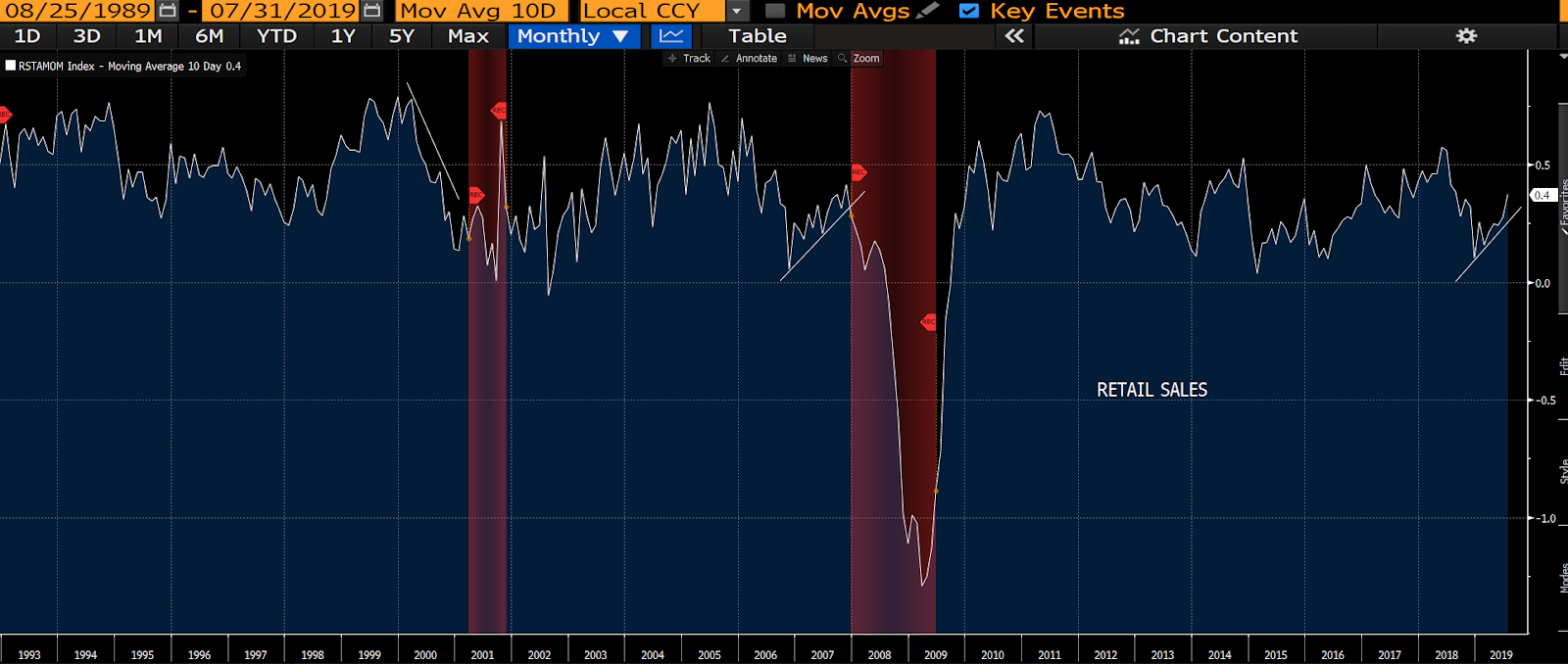

Here’s retail sales (we have 20 years of data):

Kudlow’s right, they are definitely trending up. But, boy, the trend looks eerily like the one that economists chased right into the Great Recession of 2008 (large red shaded area). Imagine how shocked one would be — if all he/she was tracking was retail sales — when the big one hit! Especially after tracking how sales were tanking heading into the early-2000s recession.

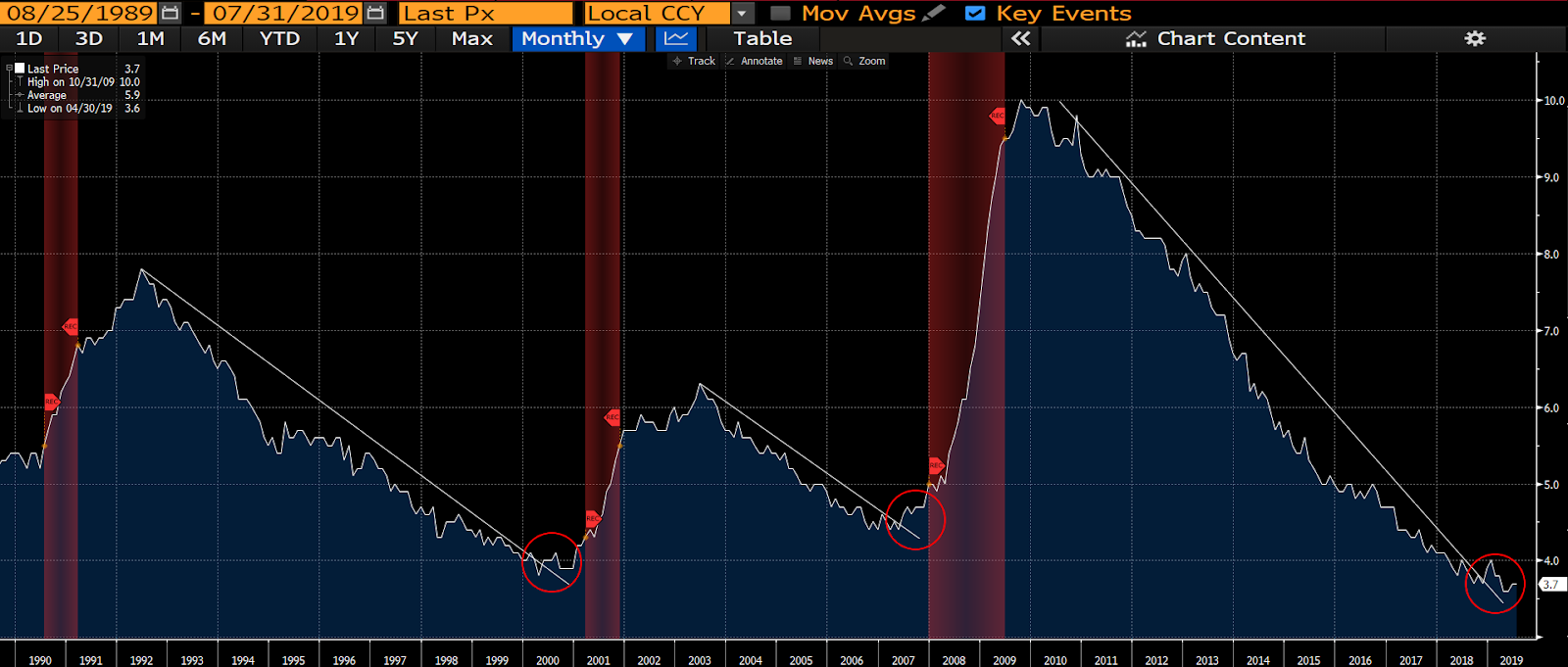

How about the unemployment rate?

OMG! Man, you’d sure think that unemployment, of all things, would be a huge indicator of a looming recession. Well, as you can see, it was of zero help heading into the last three.

Since Mr. Navarro brought it up, here’s our yield curve graph. Top panel is the 2-yr/10-yr, bottom is the 3-mo/10-yr (the one the Fed tracks):

As you can see, the 3-mo/10-yr has been underwater, with some space, for several weeks. Again, the 2-yr/10-yr just visited inversion last week, for the first time in years.

As for tracking macro tea leaves, like Navarro, we do it religiously.

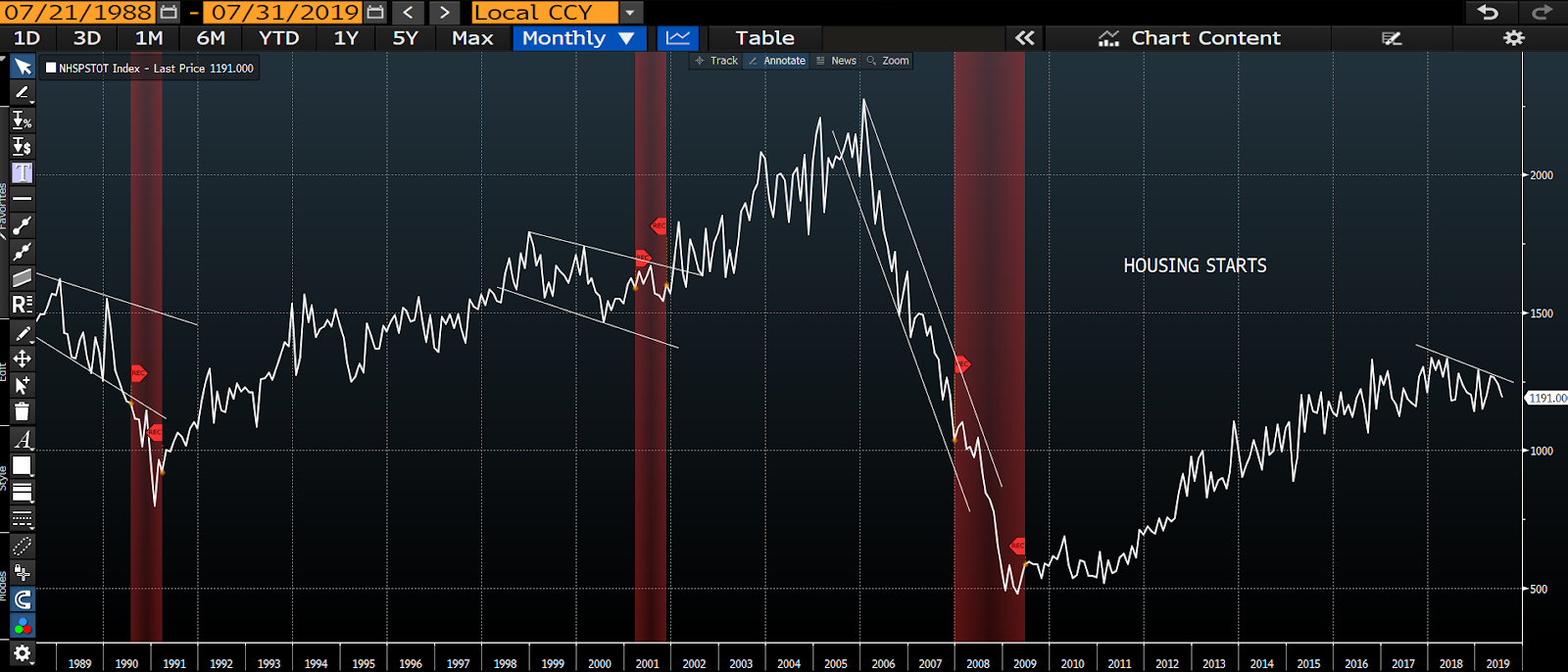

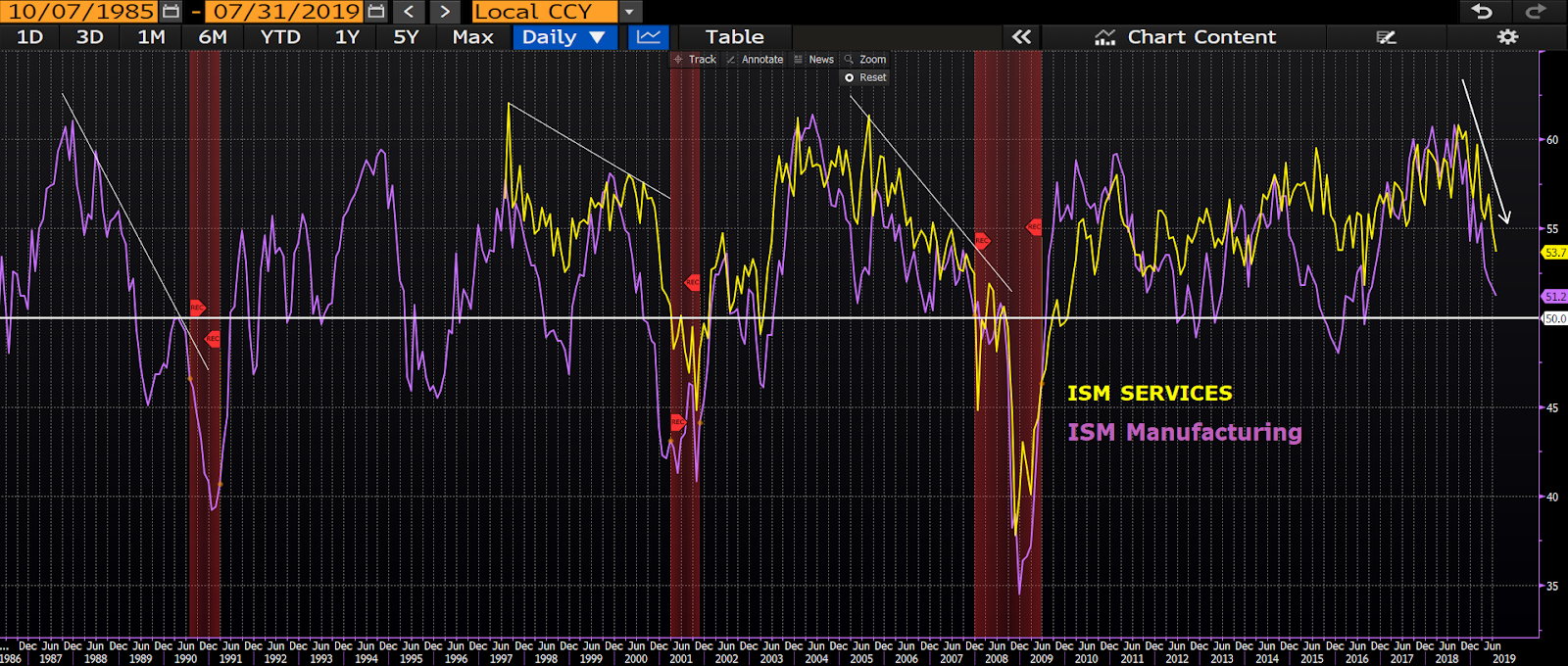

Here are a few of the key macro indicators that are presently weighing on our index. Note how they tend to trend leading into recession; you’ll see why we don’t share Kudlow and Navarro’s confidence on the present state of general conditions.

Housing Starts:

Institute for Supply Management Surveys:

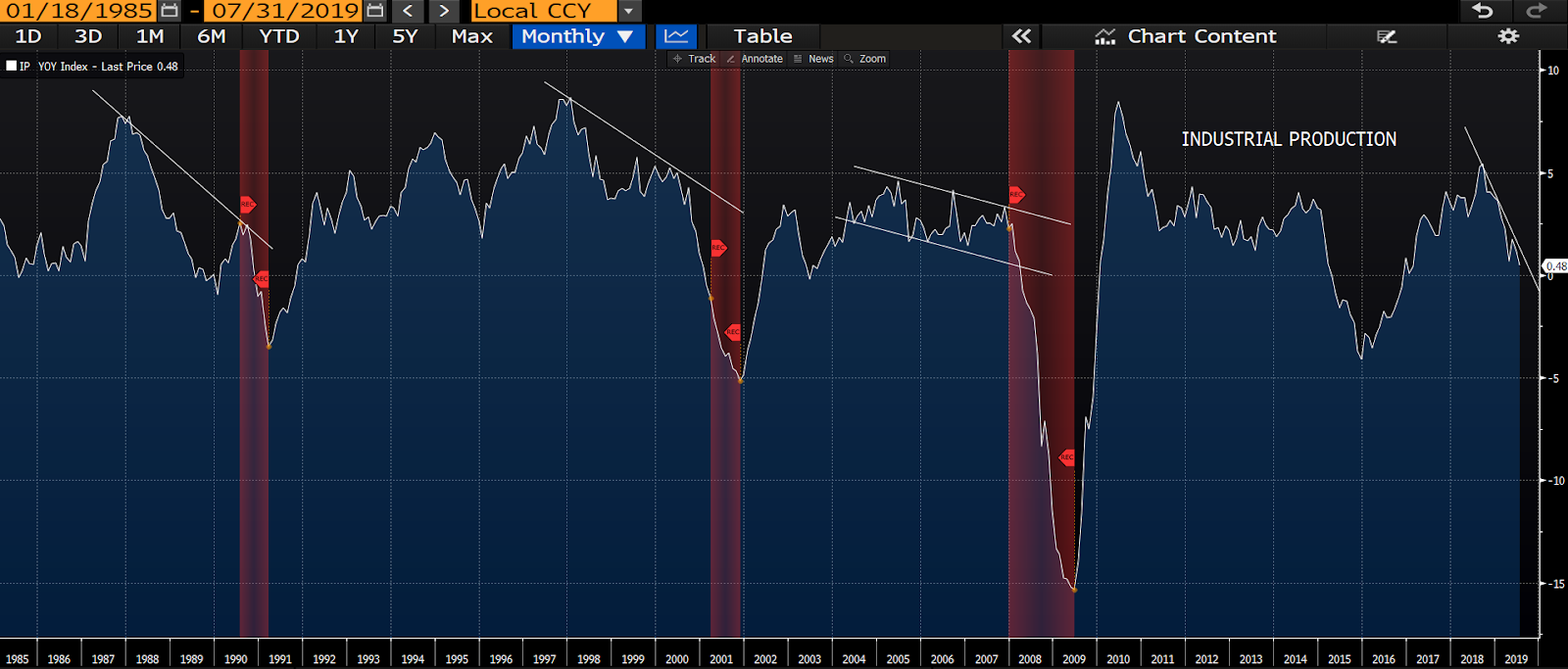

Industrial Production:

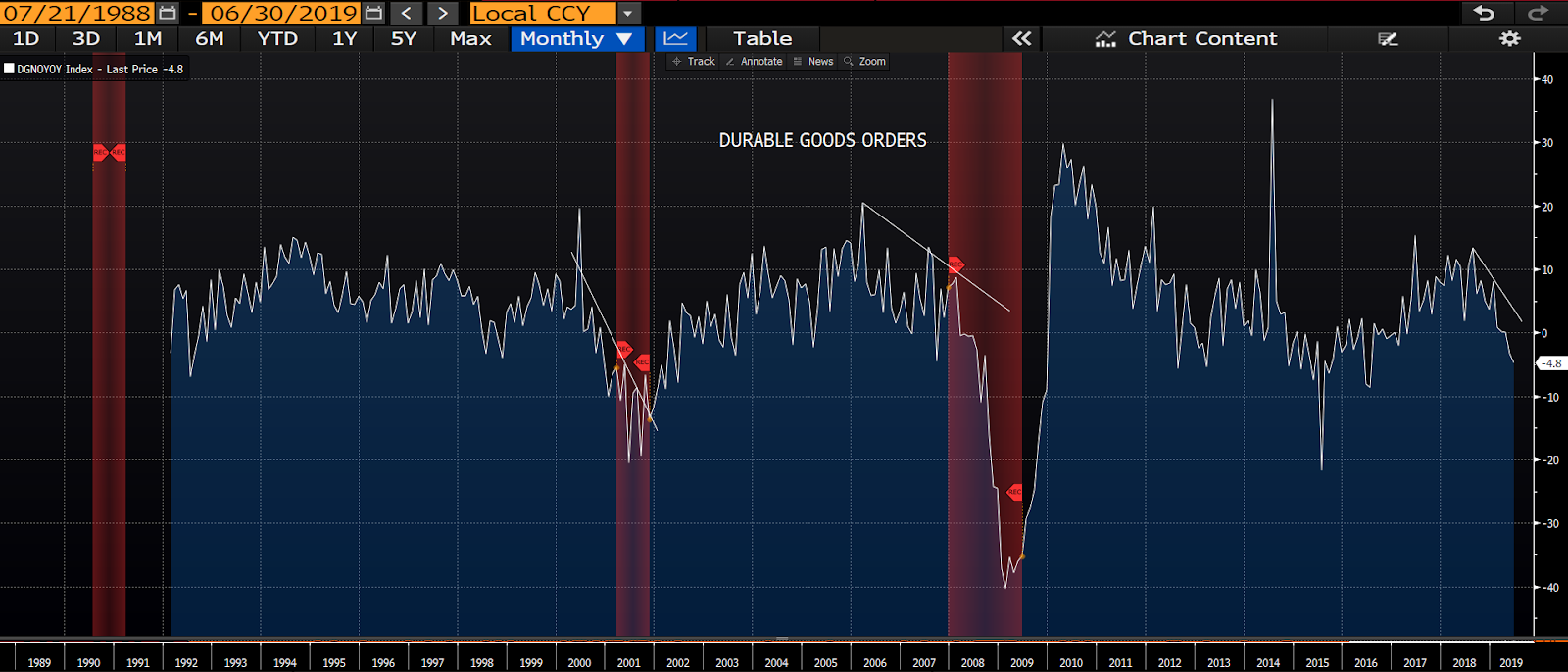

Durable Goods Orders:

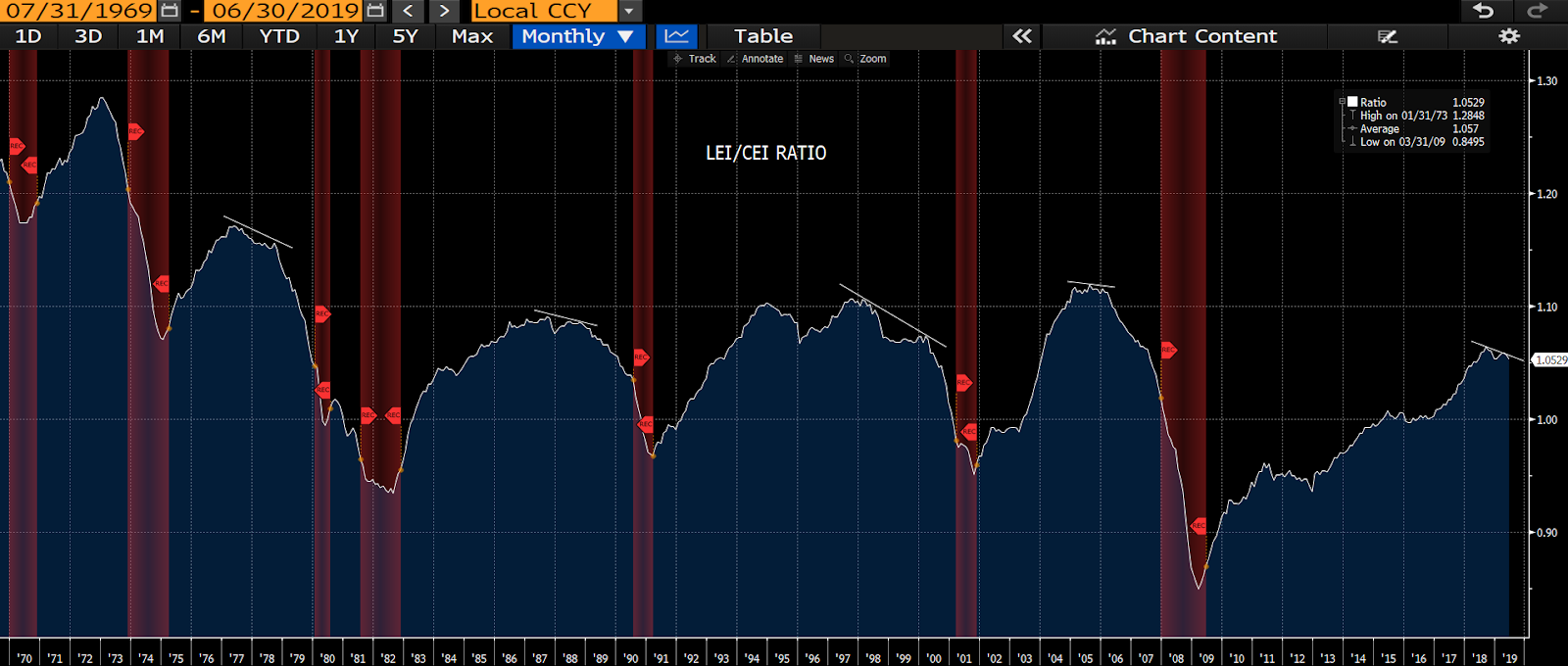

Leading Economic Index/Coincident Economic Index Ratio:

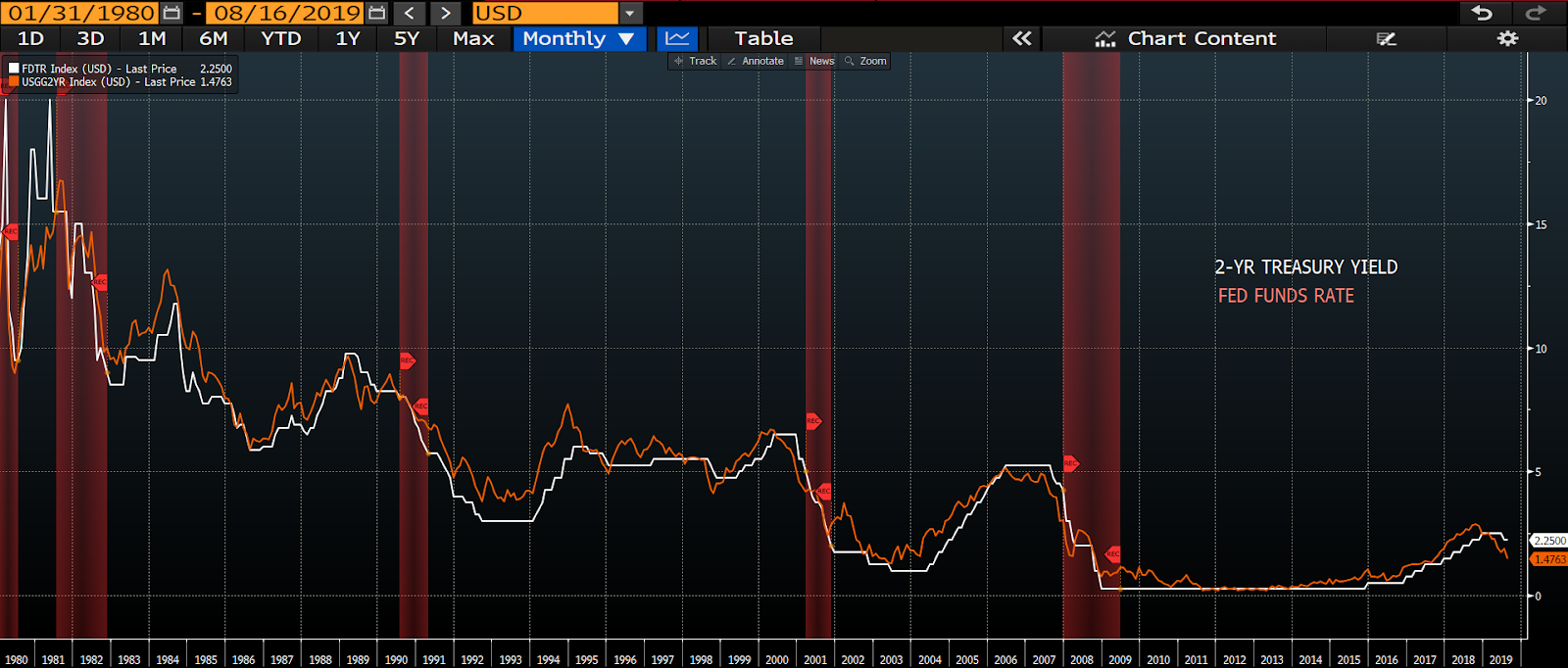

2-Yr Treasury/Fed Funds Spread:

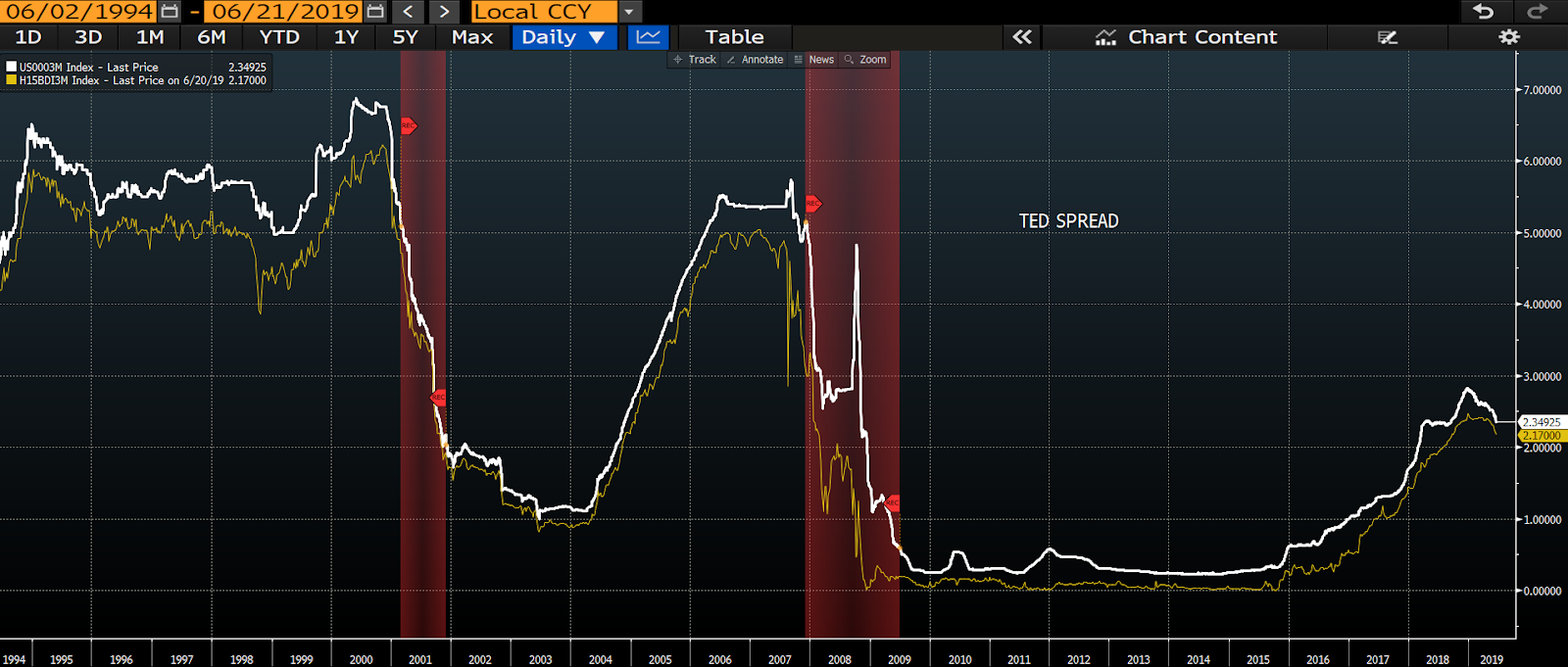

TED Spread (3-mo LIBOR/3-mo TBill):

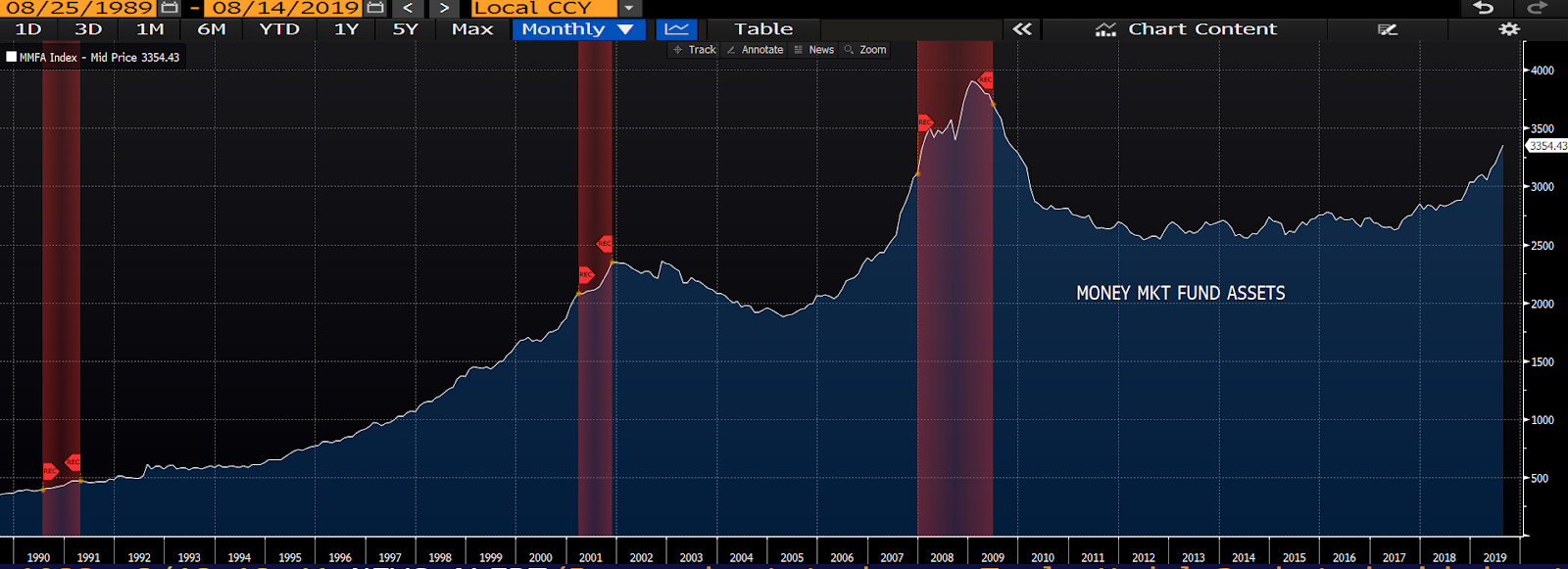

Money Fund Assets:

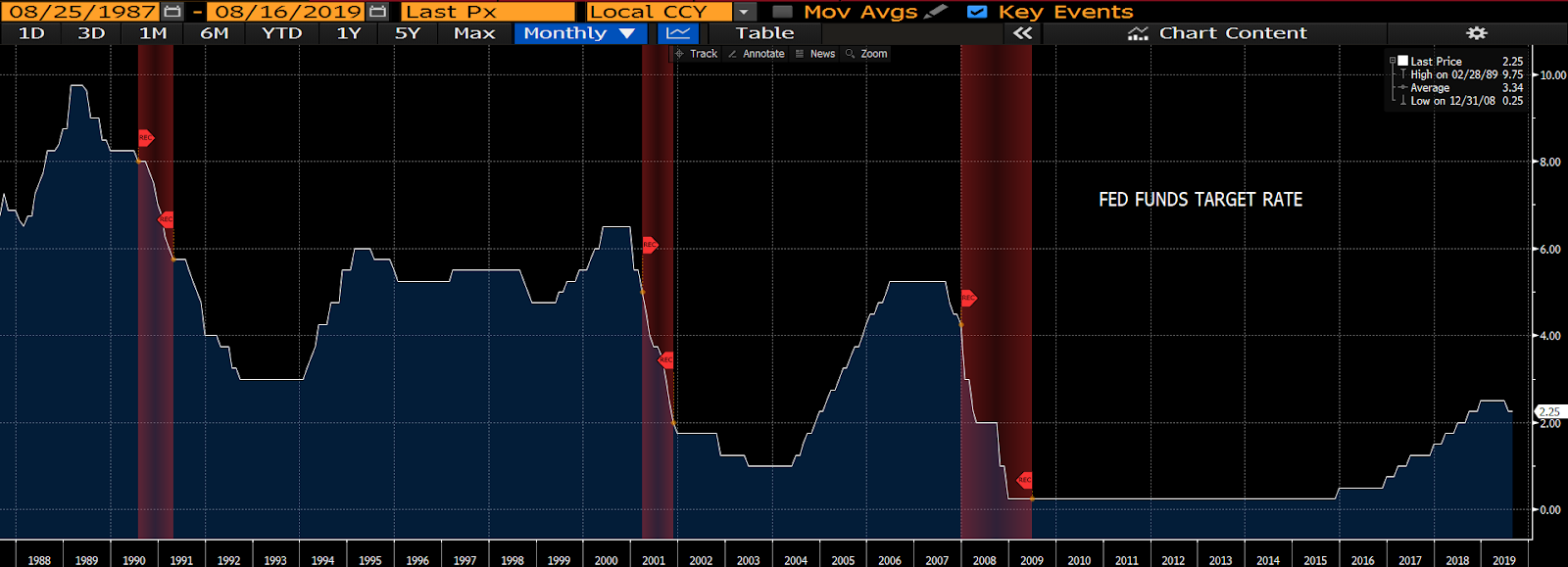

And, lastly, Mr. Navarro based much of his bullish prediction on the fact that central banks will be cutting rates like mad for the foreseeable future (stocks tend to love that, for awhile, by the way).

Here’s the Fed Funds target rate. Note all the times it’s dropped (when the Fed cut it) over the past 20+ years. Remember, the red shaded areas are past recessions:

In closing, a personal note to clients: I fully recognize that, especially over the next 15 months, political tensions will be running very high within the American community (not that they aren’t already), and that it’s quite possible (if not highly likely) that as I address the issues, factors, conditions, policies, proposals, etc., that effect markets herein, that I’ll touch a nerve every now and again.

Clearly, the above message (for example) isn’t complementary of two of the current administration’s top appointees. As I read what I wrote, it actually seems a bit condescending. But the thing is, if you caught either gentleman on TV today, you might walk away wondering “what the heck is Marty doing hedging my portfolio right now.”. Well, I felt like I should remind you.

Oh, and by the way, if you’re new to the blog, long-time subscribers will tell you that I seemed brutal at times to the prior Administration and its henchpersons. Read my 2013 book if you don’t believe me. (Oh geeze, was that a shameless plug or what!?!)

All I can say my friends is that it is never my intent to offend or annoy anyone as I share my thoughts on the whys and wherefores of the developments that impact general conditions, risk/return setups and influence how we approach the management of your money during what are bound to be very uncertain times ahead.

It is my hope, actually, that you fully appreciate how important it is that the folks who manage your portfolios are able to transcend their own political biases as they fulfill their fiduciary responsibility to you and yours.

Yours truly,

Marty