Today, true to form for the past few days, the market rallied right into the close (very bullish indicator) and logged yet another all-time high for the major averages!

As I stated yesterday, the disconnect between the action in fixed income versus equities is stark!

The bond market is virtually screaming recession, while the stock market is screaming nothing but blue skies ahead; that is, the major averages are screaming blue skies ahead.

“That is”, small caps and transportation stocks – traditional bull market leaders – are presently severe laggards:

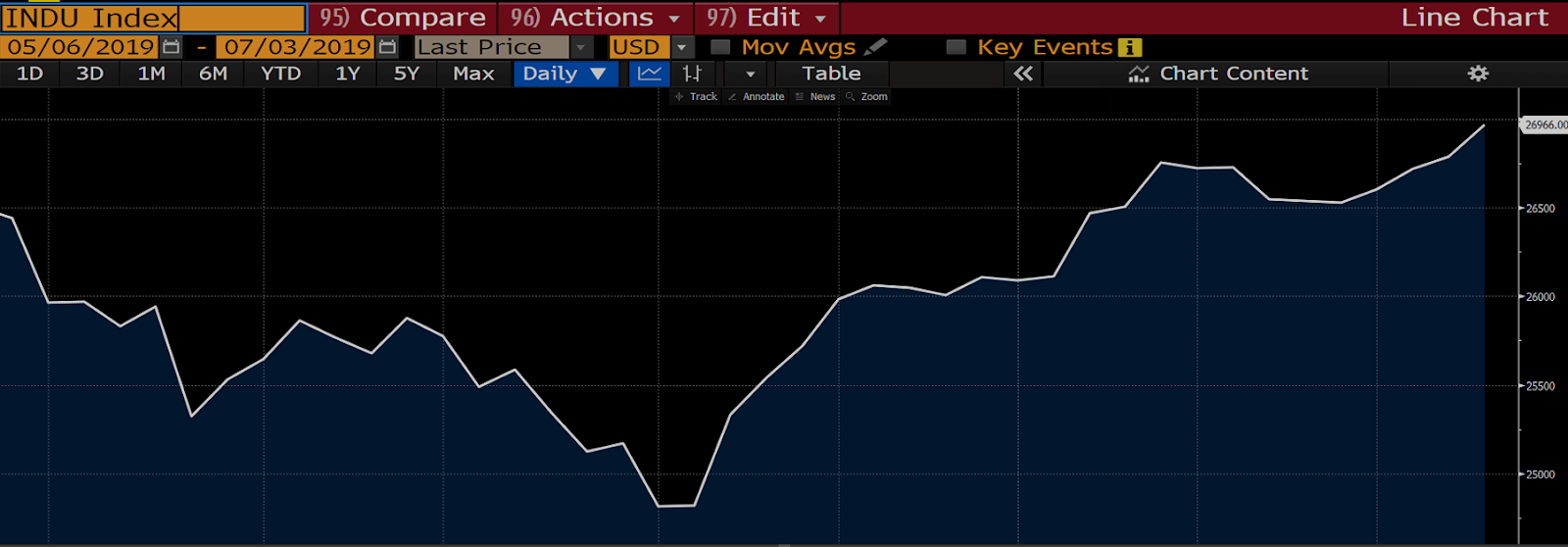

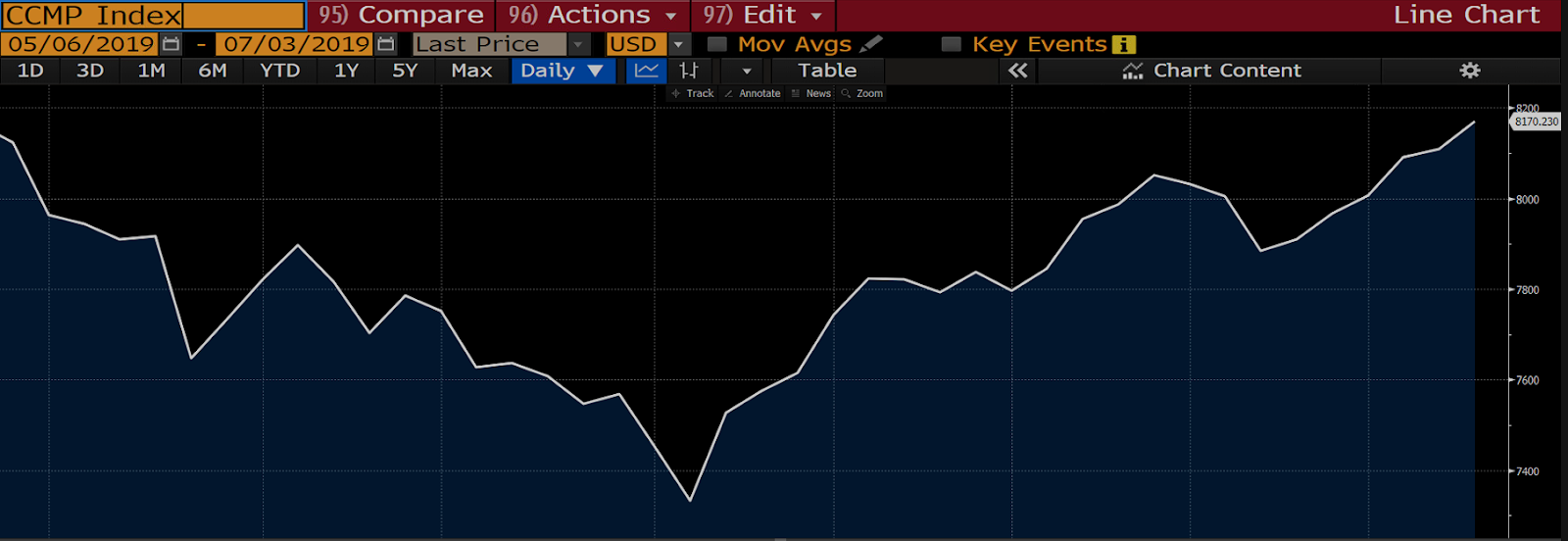

Take a look. click any chart below to enlarge….

Here’s the S&P 500 since the previous peak:

Here’s the Dow:

Here’s the Nasdaq:

But, here are smallcaps (uh oh!):

And here are transports (“ “!):

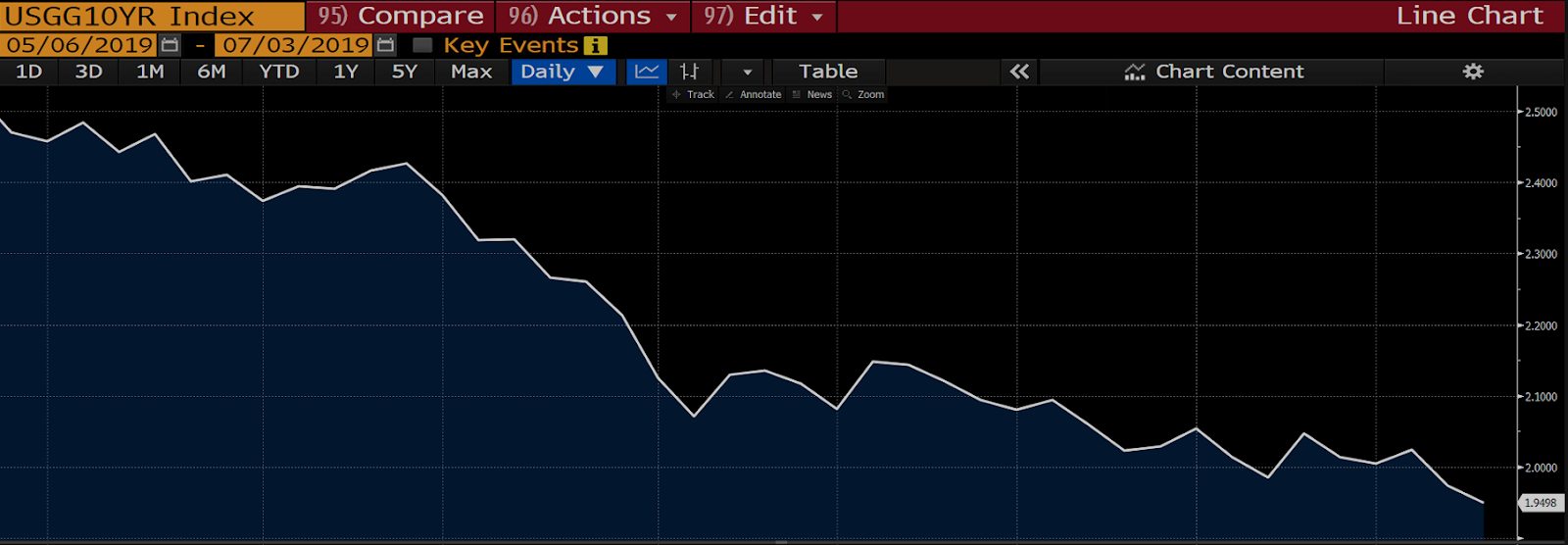

And to illustrate my point regarding fixed income — generally you’d expects bonds selling off (yields rising) in a world where the stock market is screaming into all time highs — here’s the chart of the 10-year treasury yield since the previous stock market peak:

Uh oh! Somethin ain’t right!

For context, here’s the 10-year yield (white) on a chart with the S&P 500 (green) from 1/1/2017 through last year:

Now that makes sense! The stock market, along with interest rates, rising on strong economic data leading into late ’18, then both collapsing on trade war – and the attendant economic – worries.

To pound it (the current contradiction) home, here’s both on one chart since the previous stock market peak:

Again (from the start of June on), UH OH!!

So what gives? Well, it’s simple, traders are betting big that the Fed is going to cut its benchmark rate this month and that the market’s going to like it a lot.

So, is this a thesis long-term investors should feel good about? Frankly, NO! You want the market rising on good economic prospects (i.e., you want confirmation from the benchmark cyclicals), and, believe it or not, you want rates (in confirmation) rising at the same time — if only for the simple reason that the Fed needs much more leverage than it currently has to work through the next recession—when it comes.

And therein lies my present concern; if the economy, as some indicators are beginning to warn, recedes into recession in, say, the next 12 months, it’ll be before the cycle would’ve otherwise called for. Of course that demands that there’s an ugly externality afoot, and, make no mistake, there is; they call it the “trade war”.

The skies absolutely cannot clear until the trade war is resolved, short-term market-boosting rate cuts or not!

Not that it matters for us long-term investors, but if this Friday’s jobs number is “bad”, look for stocks to rally on the news (today’s ADP jobs number missed estimates by 38k!); as it’ll bolster the rate cut case. If it’s really good, look, therefore, for stocks to sell off.

If you’re scratching your head, you should be…

Happy Independence Day!

Marty