In addition to an analyst’s upgrade of U.S. chip makers, the chatter this morning is that the trade war is suddenly taking a positive turn; as (in addition to the weekend news referenced below) the White House is entertaining top U.S. tech sector officials today to discuss the Huawei ban (presumably exploring ways to lift it, at least a bit), and there’s rumor that in-person talks will resume in Beijing sometime next week.

Per my internal log entry yesterday (shared with you below), I’m growing more skeptical by the day:

7/21/19 Sunday

In what I would view as the first positive development with respect to the US/China trade conflict over the past couple of weeks, it was reported Sunday morning that some Chinese businesses are requesting exemptions from tariffs on certain U.S. ag products; which conflicts (welcomely) with the recent shift among Chinese negotiators to a far less conciliatory posture versus where they were a few months ago. Chinese state media says this should be viewed as a good faith gesture, and the hope is that the U.S. will reciprocate with relief for Huawei (allowing it access to essential U.S. tech components).

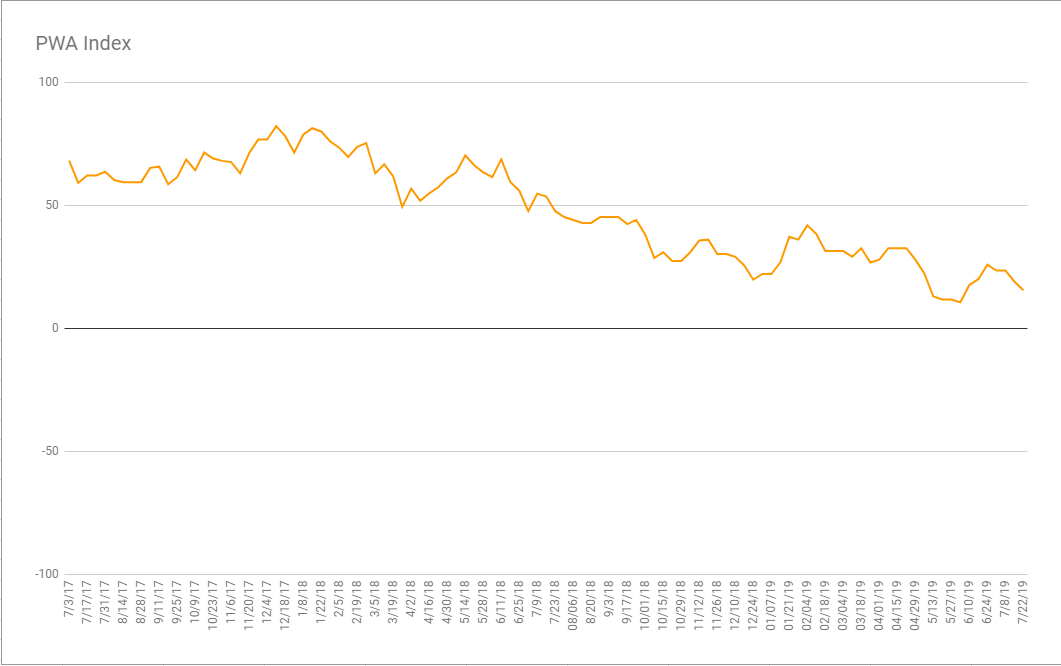

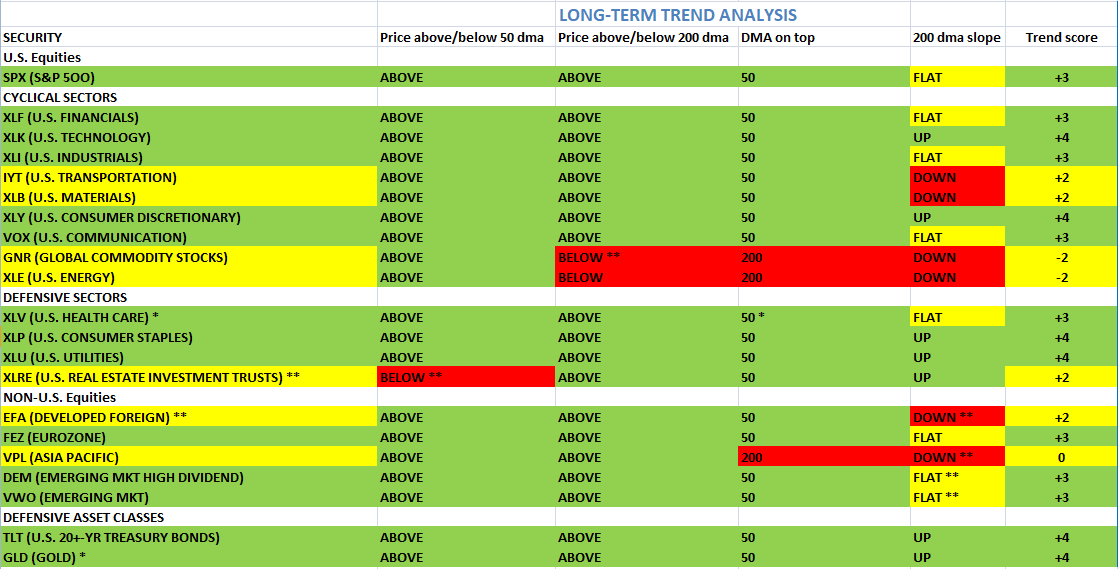

I suspect the market will respond positively when futures trading resumes this evening. Were it not for that news, however, I believe there would’ve been follow-through selling after Friday’s notable intraday reversal (there may still be regardless) – as the daily trend shifted late last week from strong buying at the close (a bullish sign), to strong selling (bearish). Plus, my weekly technical analysis paints quite the negative short-term picture for the cyclical sectors, as well as the major averages here and abroad, while looking more constructive with regard to the defensive sectors, bonds and gold: click any insert below to enlarge…

Despite my near-term bearish bent, there’s no question this market possesses real near-term upside potential. Problem is, what was once a fundamentally sound macro backdrop has morphed into one of real uncertainty spawned by a global surge in protectionism (and populism!) that, unfortunately (and scarily), alas, presently works wonders politically.

As for any stock-market-upside from here, its engine will be the ingrained (and, frankly, faulty) belief that central bankers can and will keep the global economic boat indefinitely afloat via interest rate cuts and, ultimately, via a whole new round of quantitative easing; as opposed to rallying on solid economic fundamentals and the attendant prospects for strong corporate earnings growth that characterized the market as recently as early 2018.

I’ve maintained herein, on the blog, and in client meetings that – previous paragraph notwithstanding – macro conditions remain decent enough that if Sino-US relations improve soon, and all of the tariffs added during the Trump Administration are reversed, there’s a good chance that the global economy will avoid recession for now and that stocks can justifiably mount further into all-time high territory well into the early 2020s.

As time goes by, however, and as I continue to assess general conditions and take note of the dramatic shift in how the U.S. approaches the world, and its previously-established trade relationships, I’m becoming more of the mind that shortly after the end of the trade war with China, if and when that occurs, that we’ll quickly hop from the proverbial frying pan into the proverbial fire; as Trump seems utterly hell-bent on inciting new trade wars with other countries (Vietnam and India — two of the world’s fastest growing emerging markets — would be latest he’s hurled threats toward), and, critically, with the European Union itself.

The fundamental problem is that, for a variety of reasons, again, protectionism presently works politically. But the thing is – and, ironically, this in my view is virtually the only thing the market ultimately has going for it – it never works economically.

The critical question, therefore, is how long will traders – in the face of global uncertainty, high valuations, and weakening general conditions – continue to bid stock prices higher solely on the basis of easy monetary policy? Ironically, while the Fed governors are acting with all the best intentions they are unwittingly inflating the next financial asset bubble; one that were it allowed to deflate a bit now would in all likelihood make dispensing with the current trend in tribalism (at least when it comes to trade) politically indispensable; as, frankly, recessions are the ultimate political career killers, and a strong equity market correction would — given present conditions — virtually have to cement strong recession fears in the hearts of traders and, most importantly, in the hearts of politicians.

In a nutshell: While our macro index (below) says the economy’s still expanding (albeit at a markedly slower pace than a year ago), and the long-term trend in the broader market (further below) remains upward, I’m growing more skeptical (over the market’s long-term prospects) by the day…