Here’s ECB President Mario Draghi this morning on conditions across the Eurozone:

“Generally speaking, you have resilience in the service sector, and construction sector, at the same time this outlook is getting worse and worse; and it’s getting worse and worse in manufacturing especially, and it’s getting worse and worse in countries where manufacturing is very important. Because of value chains this propagates all over the Euro Zone.”

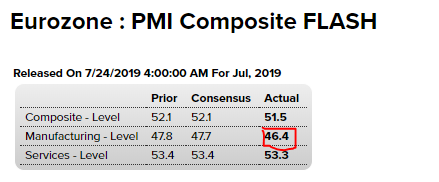

He essentially echoed yesterday’s release of the Flash PMI (Purchasing Managers Index) Survey results for July:

Note: 50 is the line separating expansion from contraction. Like he said, the services sector looks okay, manufacturing doesn’t.

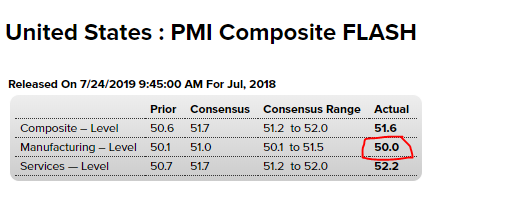

So how about the U.S.?

Well, while U.S. manufacturing conditions aren’t yet recessionary, they’re almost there. Services, on the other hand, are still okay, although not quite as strong as the Euro Zone reading:

This is consistent with my current assessment, via categories within our own macro index: Our economic subindex scores a relatively low +9.62 (0 is our expansion/contraction dividing line), with the consumer component scoring a sold +50, while the business component scores a very weak -20.

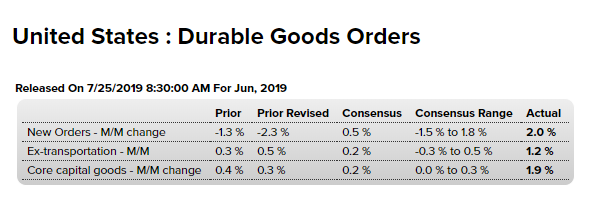

Now, to bring home how difficult it is to gauge the present state of the world, here’s today’s July durable goods numbers, with highlights (i.e., they were good!):

Highlights

If manufacturing is the Federal Reserve’s central focus, they have less to be worried about. Not even the 2.0 percent headline jump in June, which exceeds Econoday’s consensus range, nor the 1.2 percent surge in ex-transportation orders that far exceeds the consensus range, take the spotlight in this report. It’s a rare 1.9 percent jump in core capital goods orders that points to new confidence in the business outlook and the release of prior pent-up demand for new production equipment.New orders for machinery rose 2.4 percent in the month with fabrications up 2.1 percent and primary metals up 0.8 percent. These are all the building blocks to increase future production. Outside of capital goods the good news includes a 3.1 percent order surge for motor vehicles, and to top it off, a 75.5 percent jump for civilian aircraft orders which in prior reports, in part reflecting Boeing 737 troubles, had been depressed. The only real soft spot in June were defense orders where aircraft fell sharply for a second month, down 32.1 percent.

Goods news also comes from readings outside of new orders especially a 0.6 percent June rise in shipments of core capital goods. As the jump in orders for this category points to shipment strength in the third quarter, the strength in June shipments points to strength and perhaps upward revisions for nonresidential fixed investment in tomorrow’s second-quarter GDP report.

Total shipments rose 1.4 percent in June, also very strong, with inventories rising a comparatively modest 0.3 percent which points to the need to rebuild inventories in what is yet another positive.

Although, alas (doubling down on my “difficult to gauge” point), the report wasn’t all good:

Not positive at all, however, is a third straight decline for unfilled orders, down 0.7 percent in June that includes a 0.8 decline for civilian aircraft. This follows aircraft declines of 1.2 percent and 0.5 percent in the prior two months in what may be a 737 effect.

In a further offset, the headline revision to May was a steep 1 percentage point lower and now stands at minus 2.3 percent, with the revision for core capital goods orders 2 tenths lower (from revised data in the May factory orders report) and now at plus 0.3 percent. Yet shipments of core capital goods in May were revised only 1 tenth lower and are now at a still very solid plus 0.5 percent.

But, still, perhaps things are good enough to have the Fed maybe think twice about piling on a ton of stimulus right about now:

Revisions and the Boeing 737 aside, this report is an echo of the strength of last week’s industrial production report where manufacturing posted its strongest performance of the year, and it diminishes the need for Fed rate cuts and will have to be put into broad context or explained away by Jerome Powell at his press conference next week should the Fed indeed lower rates.

And, lastly, the trade deficit widened this month, while both retail and wholesale inventories missed expectations (all components in tomorrow’s GDP number). Perhaps the President’s been given the heads up that maybe tomorrow’s number will come in a bit soft; as he tweeted earlier:

“Fox Poll say best Economy in DECADES!”

Well, the business polls, and, obviously, the Fed, and, not to mention, the PWA Macro Index say different…