Three months ago I offered up the highlights of my then six-month thesis. I’ll cut and paste it below, and report (in red) on how its panning out so far:

March 14, 2019:

Question: Per the theory of Reflexivity, should, for example, stock prices fail to overtake the Sept ’18 high before retesting the Dec ’18 low, will they negatively influence the trend to the point of reversal, thus flipping the prevailing bias to negative, and precipitating the next recession and bear market?

Question: Per the theory of Reflexivity, should, for example, stock prices fail to overtake the Sept ’18 high before retesting the Dec ’18 low, will they negatively influence the trend to the point of reversal, thus flipping the prevailing bias to negative, and precipitating the next recession and bear market?

In my current view, no. Odds favor general conditions withstanding what’s likely to occur over the next few months, and, thus, favor stock prices moving above the Sept 2018 highs in the coming weeks.

Stock prices “moved above the Sept 2018 high” on June 19th (roughly 13 weeks after I penned this note).

Stock prices “moved above the Sept 2018 high” on June 19th (roughly 13 weeks after I penned this note).

Per my present 6-month thesis (abbreviation):

1. Accommodative central banks, and governments, will stimulate in aggressive-enough fashion; sufficient to stave off recession this year (and likely next).

Central banks have absolutely turned dovish (stimulating), as anticipated, however I’m less sanguine on my view of recession odds for next year.

2. The U.S. will ink a deal with China that will see a sharp short-lived rally in stocks. That will embolden Trump to threaten hardball with Europe. Global equities (save for China) will immediately tank when markets sense such. Equities tanking will bring the sides together quickly to mend fences and make a deal. Monetary and fiscal easing will have bolstered economic sentiment enough to sustain the relatively short US/EU tiff.

Jury’s still out, but this one (with China) is taking dangerously long to play out, and, as recently as today, Trump is threatening to go hard at the EU.

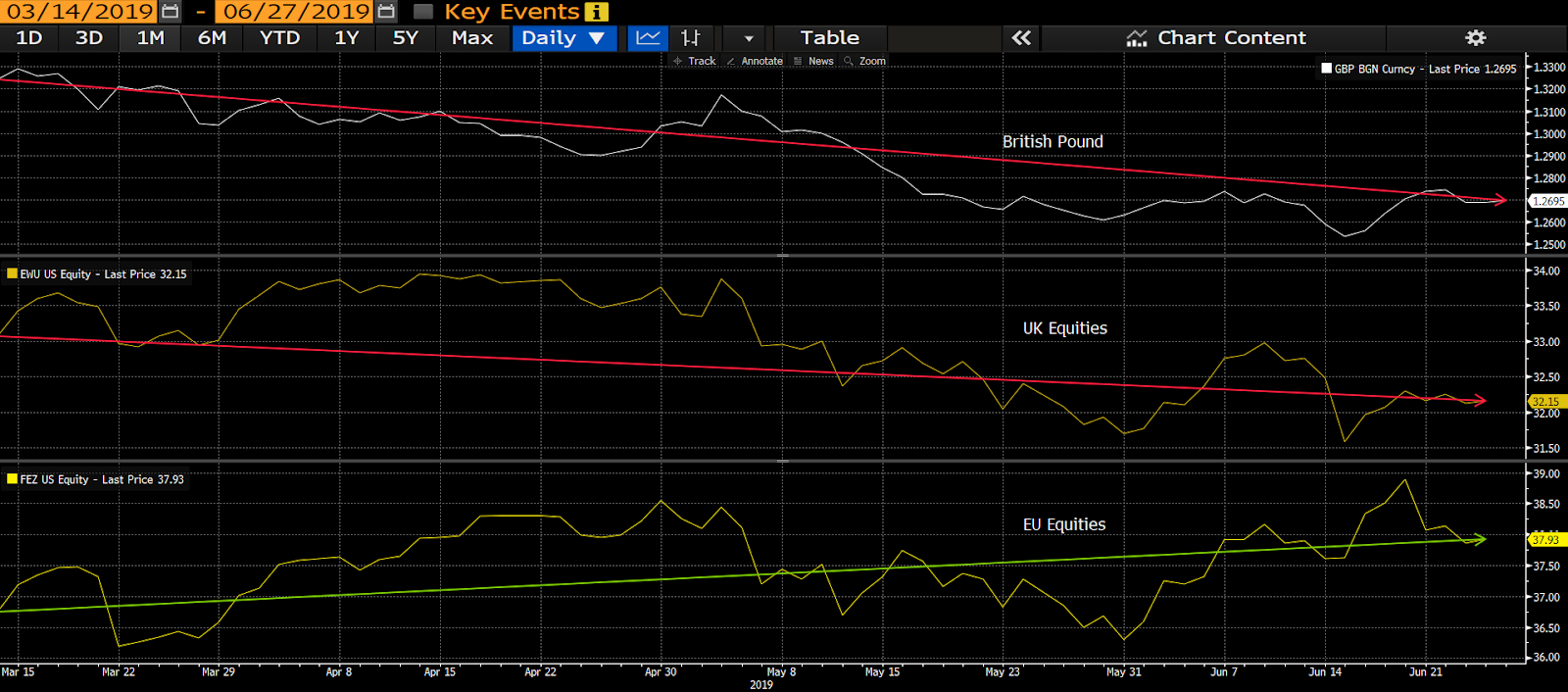

3. Article 50 will get extended, the hard-Brexiteers will soften and a deal will be struck later in the year. The extension will relieve pressure on the pound, UK and EU equities.

Article 50 did get extended, and while it’s gotten dicey, this is still my base case.

Here’s a chart of the pound, UK and EU equities since the date I posted this article (i.e., wrong on the pound and UK equities, right on EU equities [but there’s still 3 months to go]). click to enlarge…

Here’s a chart of the pound, UK and EU equities since the date I posted this article (i.e., wrong on the pound and UK equities, right on EU equities [but there’s still 3 months to go]). click to enlarge…

4. Global equities will trend higher into the fall. Bonds will hold up (yields will hold down) until trade issues are resolved; trending lower (rates higher) thereafter on the prospects for accelerated growth and tighter central banks. The Dollar — despite the prospects for rising U.S. interest rates — will trade lower on the prospects for the rest of the world’s economies/asset markets catching up.

So far so good in terms of equity and bond trends. That’s still my base case for bonds “thereafter” if trade issues are resolved. And, yes, the dollar has been trending lower of late, and Citi’s U.S. Economic Surprise Index (top panel in first chart below) remains way underwater, while the Eurozone’s (bottom panel) — for example — has just turned positive. click to enlarge…

As for the rest of the world’s economies, Citi’s Global Econ Surprise Index currently scores -27.3 versus the U.S.’s -65.9. I.e., the U.S is currently lagging markedly versus the rest of the world in terms of current data relative to economists’ expectations.

Here’s a chart of global equities, U.S. bonds and the dollar (i.e., right on all three [but there’s still 3 months to go]). click to enlarge…

As for the rest of the world’s economies, Citi’s Global Econ Surprise Index currently scores -27.3 versus the U.S.’s -65.9. I.e., the U.S is currently lagging markedly versus the rest of the world in terms of current data relative to economists’ expectations.

Here’s a chart of global equities, U.S. bonds and the dollar (i.e., right on all three [but there’s still 3 months to go]). click to enlarge…

What can go wrong? No changes (alas!)…

1. Trump walks away (with no near-term path for turning back) from a China deal. Hugely bearish for stocks! Recession risk explodes higher and we get busy adjusting client portfolios.

2. A deal gets done, but existing tariffs remain. Not as bad as no-deal, but stocks will nonetheless sell that news.

3. The coming row with Europe gets under the key players’ skins to the point where they abandon their economic/market-centricity and we have a protracted US/EU trade war; which means general sentiment tanks, taking an already weakened economy with it. And we get busy.

4. Brexit blows up and sparks a cascade in European equities that ripples across the globe. Best case scenario, 10-20% correction; worse case, global sentiment tanks to the point of catalyzing the next recession. And we get busy.

5. #1 or #2 and #4 both occur this year. And we get busy!