6/29/19 Saturday

The Trump/Xi summit concluded pretty much as the market anticipated — a truce — with one even market-friendlier exception; Trump suggested that U.S. companies can indeed sell to Huawei when national security is not at risk (“more details to follow”).

So, no escalation at this point, negotiations to restart right away, trade war tariffs already in effect remain, no time frame for the reaching of a deal, and possible Huawei relief.

My expectations for the stock market:

Short-term:

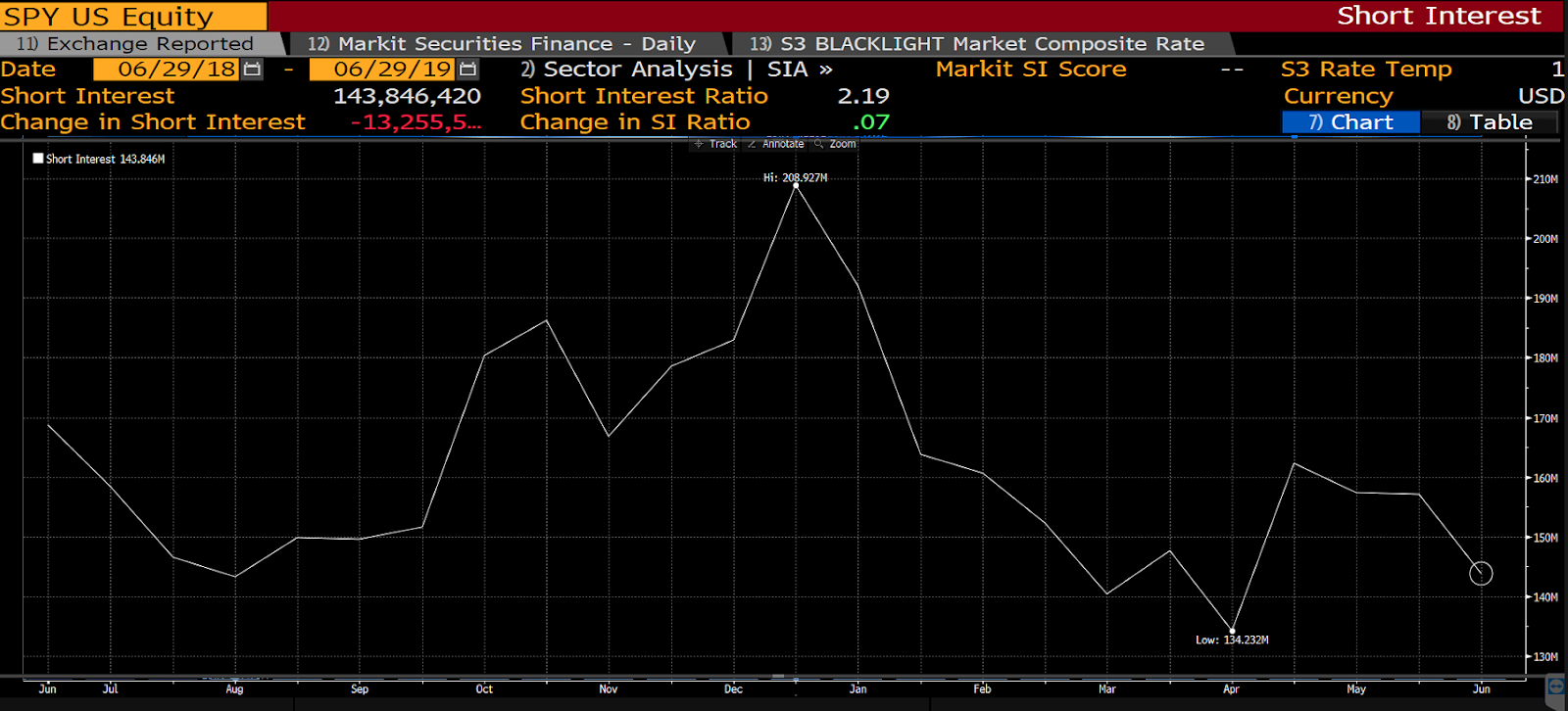

While there’s no doubt a concentration of shorts at current levels that will likely cover come Monday morning, considering SPY’s relatively low short interest level,

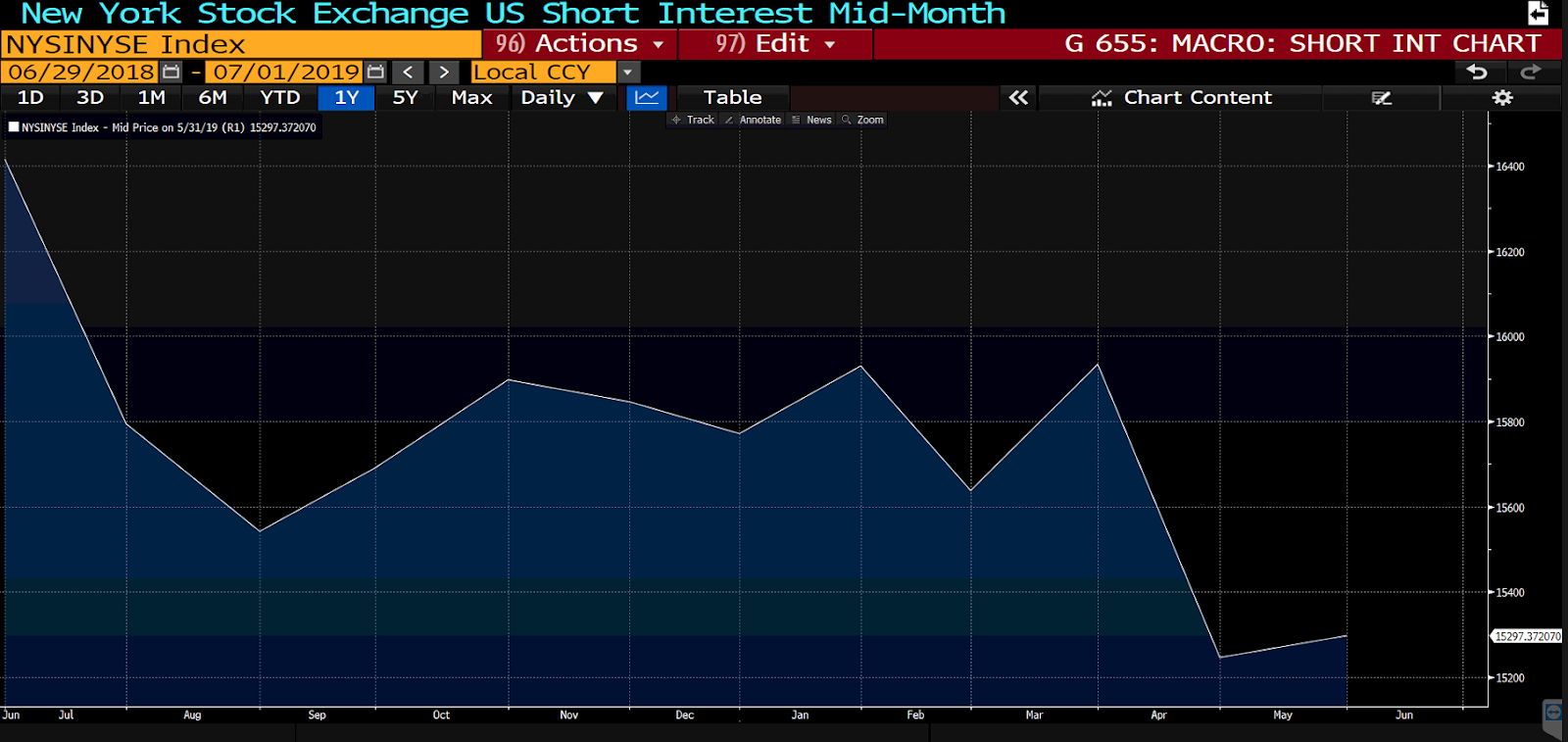

and the same reflected in the latest NYSE Short Interest Report (although it’s a month old),

we’re not looking at a massive short-covering rally.

That said, despite the market’s record high level, individual investor sentiment came in surprisingly below average last week: That denotes skepticism and, thus, cash on the sidelines. In fact, looking at our latest money market fund assets chart (next chart below), there is indeed a lot of cash that can come rushing into stocks right here, if it so desires:

So, good chance for a strong rally to start next week.

Further into, and beyond, next week:

The Fed: I suspect we’ll see the odds of a July cut come down in the futures market, now that trade war escalation is off the table (for the moment). That is bound to temper the extent of any rally. In terms of economic data going forward; the bad-news-is-good-news trade (justifies fed cuts) – and/or the good-news-is-bad-news trade (justifies no cuts) — now gets exacerbated in a big way.

Corporate Earnings and Economic Prospects: The fact that there’ll be no letup in existing tariffs, and no time frame for a resolution, corporate earnings estimates will continue to be ratcheted lower; as more evidence rolls in that, even without escalation, the trade war is doing serious damage to economic, and, thus, earnings (and stock market) prospects. That said, we could see a boost in the earnings estimates of chip-makers, if indeed they’ll be able to sell to Huawei going forward.

Bottom line:

While no escalation and the potential for a Huawei reprieve are bullish, the no-time-frame for lifting existing tariffs leaves the odds of a sustainable move well into all time high territory for stocks relatively low, and the odds of a recession occurring within the next 12 months relatively high.

The political risk associated with the latter makes it highly likely that a tariff-eliminating deal will be struck sometime between now and November 2020. As long as economic conditions hold up, that’ll have me sounding a strongly bullish tone! The risk, therefore, is that Trump waits too long to strike a deal; my guess is that it needs to occur within the next 6 months, 9 months tops. And, this is a huge “and”, he needs to absolutely not threaten a tariff war thereafter with the EU!!