Yesterday afternoon the Fed released its latest “Financial Stability Report“; its findings suggest that the Fed has some concerns over asset valuations and debt levels (related to businesses) in the U.S. economy. On the plus side the report states that household borrowing remains modest relative to incomes, and sub-prime (credit score) borrowers’ debt levels remain “flat”. Banks remain in very good shape, as do insurance companies, and hedge fund leverage “appears to have declined over the past six months”.

The above credit market characteristics jibe with the presently high (safe) score of our own “Financial Stress Subindex”, which is a component of our PWA [Macro] Index.

As for where we spend much of our time, the equity markets, the Fed finds that “prices relative to forecast earnings remain above the median over the past 30 years”. Our weekly analysis agrees there as well, as we have U.S. equities currently scoring neutral (zero) in terms of valuation; i.e., while above average, they are not at historically excessive (or dangerous) levels. We show non-U.S. equities, however, as being attractive (scoring a point in our Financial Markets Subindex).

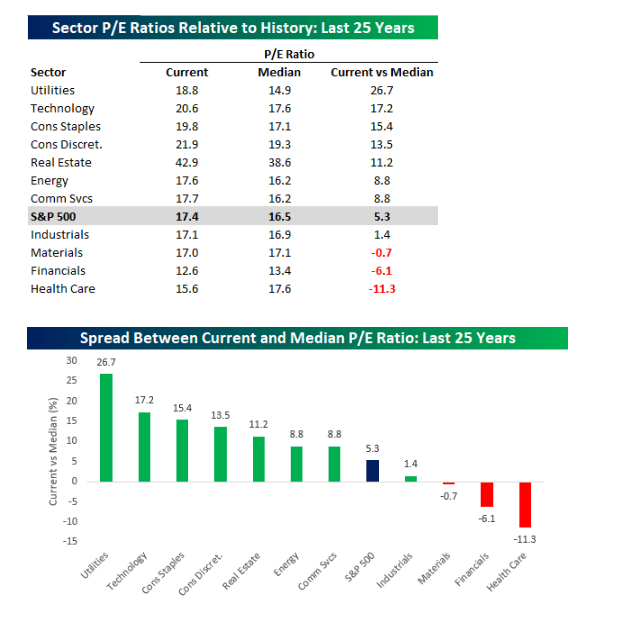

Drilling down on valuaitons, we like that our three top target sector weightings — Financials, Industrial and Materials — represent three of the four most attractive sectors relative to their historical averages.

Take a look: click to enlarge…

Source: Bespoke Investment Group

Healthcare’s historically-cheapest valuation is all about the drubbing the sector has undergone primarily due to the passion (in some circles) surrounding the “Medicare For All” concept.

As for our top three targets, industrials and materials have been restrained by the reality (bottom line hits due to tariffs) and the fear (caution among equity investors) over present trade dispute(s) (although industrials have had a good ’19 thus far), and the banking sector (financials) has been held back (although looking better so far this year) by an investor focus on net interest margins amid a still-low interest rate environment.

Our sector weightings are always a direct reflection of our ongoing macro analysis, which today has odds favoring a continued expansion and, thus, a favorable environment for the cyclical sectors going forward.