The consensus among financial pundits is that yesterday’s global stock market drubbing was catalyzed by the inversion of the Fed’s favored yield curve signal; the 3-mo/10-yr treasury yield curve.

During “good” times the curve should possess an upward slope (10-yr yield higher than the 3-mo yield), while an inversion of the curve (3-mo yield higher than the 10-yr yield) is a warning sign that the good times may be coming to an end.

The reason why Friday’s flipping of the yield curve may have been such a shocker for stocks is the widely-known (and respected) fact that since 1962 every single recession was preceded by an inversion!

Now, not to throw warm water on such a chilling development, but I have to add that not every inversion since 1962 was followed by a recession. Meaning, there have been occurrences when the curve inverted then re-steepened before re-inverting ahead of a recession.

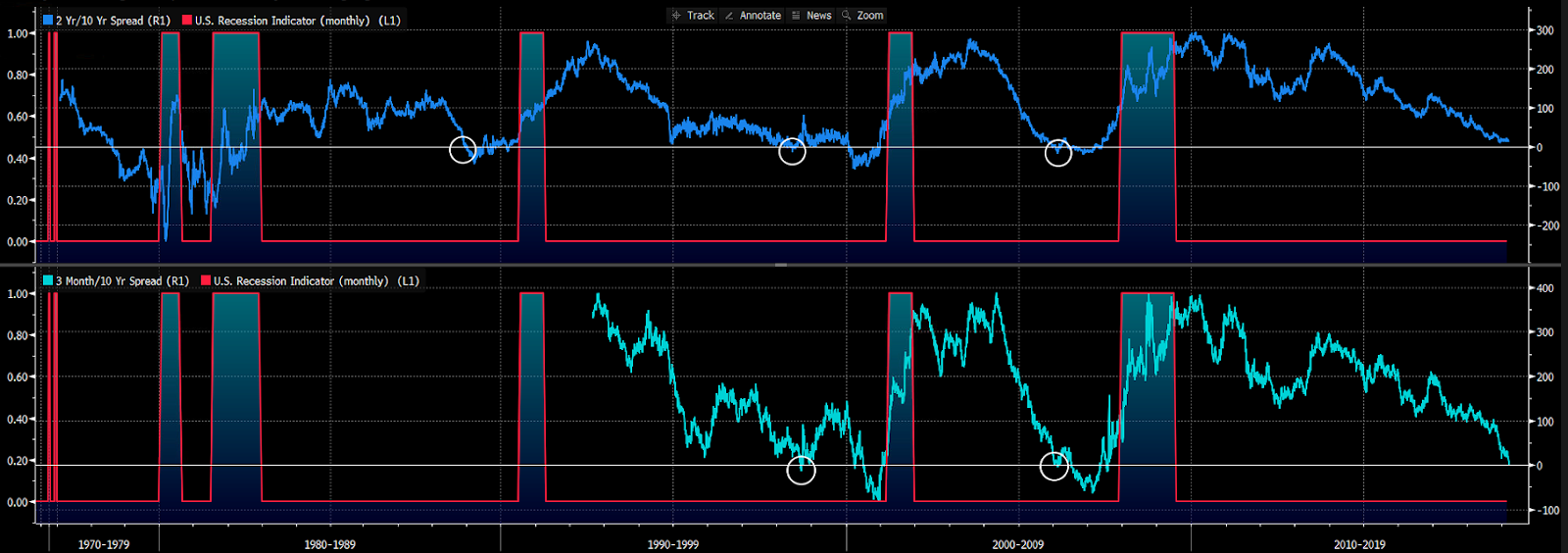

Here are our graphs of the 2-yr/10-yr relationship (top panel) and the 3-mo/10-yr (bottom panel). The 2s/10s is the one we include in our macro index; plus, our database offers us a longer look at that particular curve. A dip below zero occurs when the long-term yield moves below the short-term (inversion). I circled the inversions that did not presage a recession:

click to enlarge…

Also note, if indeed Friday’s inversion turns out to be a harbinger of the next recession (and bear market), we’re, on average, still 18 months out.

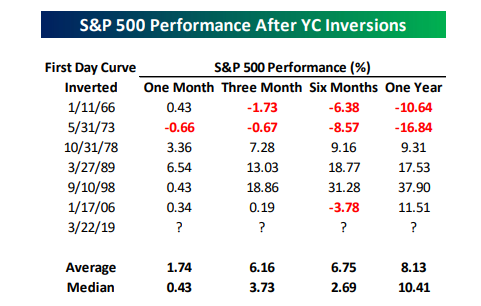

Bespoke Investment Group, in their weekend commentary, addressed the historical implications for stock market returns immediately following yield curve inversions.

As you can see, if indeed, as the overwhelming message from the financial media suggests, Friday was all about the inverted yield curve (not my opinion btw), we probably should resist running for the exits just yet:

As I suspect you’d agree, prudence demands that one not take one indicator as market-timing gospel, rather, one should address it in the context of the overall macro picture.

Our PWA [Macro] Index scored a +27 this week, off 6 points from last week. Our financial markets subindex declined as a result of somewhat weakening stock market breadth on a sector-by-sector basis, along with a decline in overall short interest (folks betting on a fall); the latter being a contrarian indicator (generally, the more the bears there are [outside of recessions], the more the potential fuel to push stocks higher on any snippet of good news). The inverted yield curve took our financial stress subindex down a bit, while falling commodity prices along with a declining Baltic Dry Index (tracks the cost of shipping raw materials across the world’s oceans) shaved 4 points off of our economic subindex.

Here’s a two-minute video illustrating the historical importance of our analysis:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Per the video, our analysis does not yet have us moving to a defensive posture.

On top of the yield curve news — and widely reported in the media — Germany posted an abysmal (recession-ish) manufacturing Purchasing Managers Index (PMI) first thing Friday morning; further calling global economic conditions into question. Interestingly, Germany’s services PMI came in firmly in expansion territory; a development completely ignored in the financial press.

While I suggested above, that, in my view, Friday’s selloff catalyst was not the yield curve, or Germany, I do believe that they absolutely added to — and validated — the angst the world is feeling over the prospects of further disruptions of trade flows, supply chains, and, thus, the waning of general economic sentiment directly resulting from the ongoing U.S./China trade war, and the serious threat of coming trade tensions between the U.S. and Europe.

Make no mistake, if indeed we’re not nearing the end of this unique bout of protectionism, the global economy, and equity markets, will have a very tough time of it going forward. The good news is that the political risk of such a scenario is monstrous! Which strongly suggests that such a long-term scenario is unlikely to unfold. But, boy, we’ll be keeping our eye on it!!

Bottom line for now: A generally okay macro backdrop, decent valuations, sufficient pessimism (potential market fuel), and amazingly dovish central banks sets a nice stage for stock market performance going forward.

Here again (originally shared with you on 3/13) is my abbreviated current 6-month base case (with followup commentary in blue):

1. Accommodative central banks, and governments, will stimulate in aggressive-enough fashion; sufficient to stave off recession this year (and likely next).

The Fed just announced that there’ll be no rate hikes this year, and that they’ll be ending their balance sheet roll-off in the fall.

2. The U.S. will ink a deal with China that will see a sharp short-lived rally in stocks. That will embolden Trump to threaten hardball with Europe. Global equities (save for China) will immediately tank when markets sense such. Equities tanking will bring the sides together quickly to mend fences and make a deal. Monetary and fiscal easing will have bolstered economic sentiment enough to sustain the relatively short US/EU tiff.

The President has been sounding off about Europe as he signals that a deal with China is forthcoming.

3. Article 50 will get extended, the hard-Brexiteers will soften and a deal will be struck later in the year. The extension will relieve pressure on the pound, UK and EZ equities.

A one-month delay was announced last week.

4. Global equities will trend higher into the fall. Bonds will hold up (yields will hold down) until trade issues are resolved; trending lower (rates higher) thereafter on the prospects for accelerated growth and tighter central banks. The Dollar — despite the prospects for rising U.S. interest rates — will trade lower on the prospects for the rest of the world’s economies/asset markets catching up.

What can go wrong?

1. Trump walks away (with no near-term path for turning back) from a China deal. Hugely bearish for stocks! Recession risk explodes higher and we get busy adjusting client portfolios.

2. A deal gets done, but existing tariffs remain. Not as bad as no-deal, but stocks will nonetheless sell that news.

The President, alas, promised precisely that last Wednesday morning. The Dow closed down 140 points Wednesday (after a huge intraday rally on the Fed announcement), and down 469 points Friday (after a 240-point rebound on Thursday).

3. The coming row with Europe gets under the key players’ skins to the point where they abandon their economic/market-centricity and we have a protracted US/EU trade war; which means general sentiment tanks, taking an already weakened economy with it. And we get busy.

4. Brexit blows up and sparks a cascade in European equities that ripples across the globe. Best case scenario, 10-20% correction; worse case, global sentiment tanks to the point of catalyzing the next recession. And we get busy.

5. #1 or #2 and #4 both occur this year. And we get busy!

We’ll keep you posted.