In our latest annual message I made the case for a weaker-trending dollar this year partly based on the prospects for a rotation away from U.S. equities into non-U.S. equities; those found in the Eurozone in particular:

“European stocks are substantially cheaper than are U.S. stocks, and our view that a global recession is not in the 2019 cards suggests that there’s a decent chance that we’ll see a rotation from U.S. stocks to Eurozone stocks during the course of the year; a scenario that would be a net weakener of the dollar vs the Euro.”

While the year’s very young, and flows will indeed come and go throughout, so far we’re seeing just that in exchange traded funds (ETFs). Although, while the Eurozone has indeed seen a net $8 billion dollar swing in its favor versus the U.S., Asia has received the lion’s share of inflows thus far:

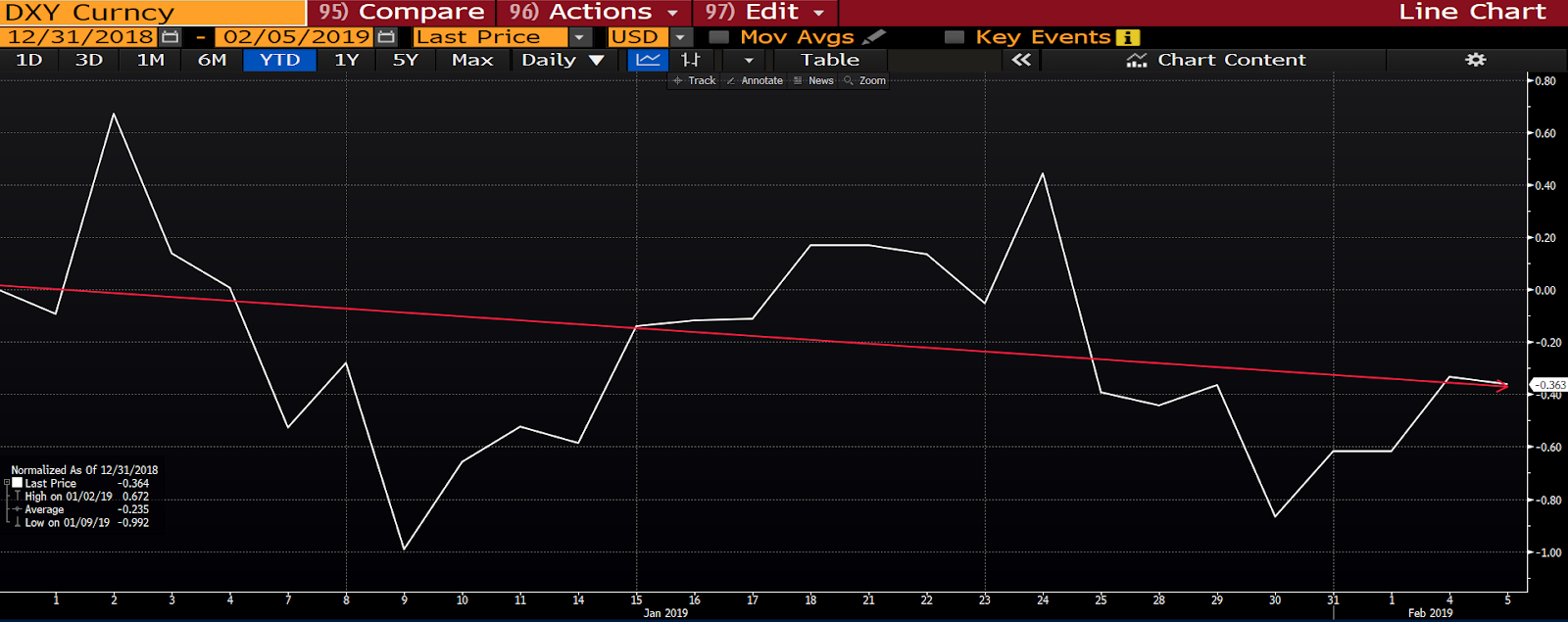

Here’s how the dollar index has fared year-to-date:

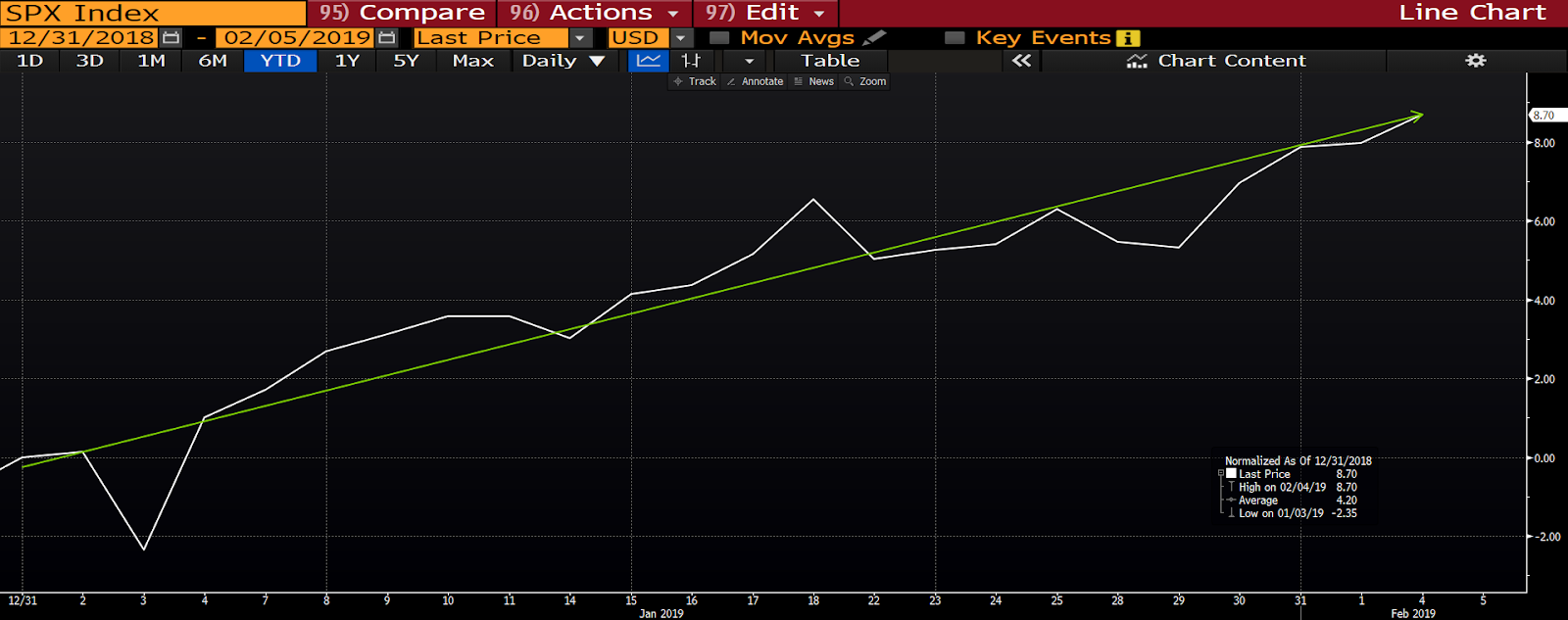

Which, despite the net ETF outflow, has been a positive for U.S. equities: