In the dollar section of our 2017 year-end letter we made our contrarian (currency traders were betting the dollar would fall) case that the dollar was likely to trend higher throughout 2018. Here’s our final paragraph where we acknowledge the difficulty in predicting and the would-be benefit if we happened to have been wrong:

“Now, let’s not get ahead of ourselves, currency markets are no easier to predict than are equity markets, so we’re more than willing to concede that maybe this time the currency crowd has it (the dollar will decline throughout 2018) spot on, and that we (the risk is to the upside) don’t. The good news is that if they’re right (and we’re wrong), our clients stand to win. As those headwinds from a higher dollar that we cited in earlier parts of this letter won’t develop after all!”

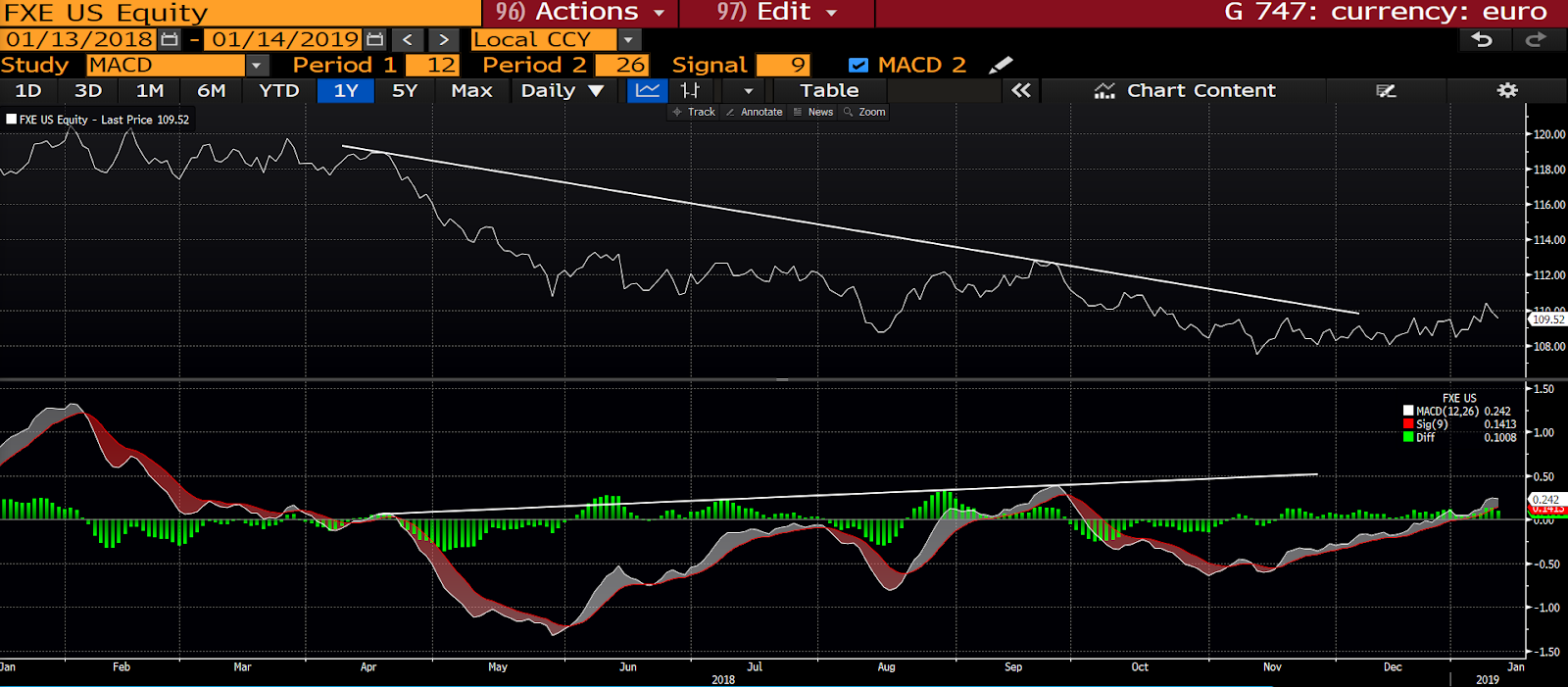

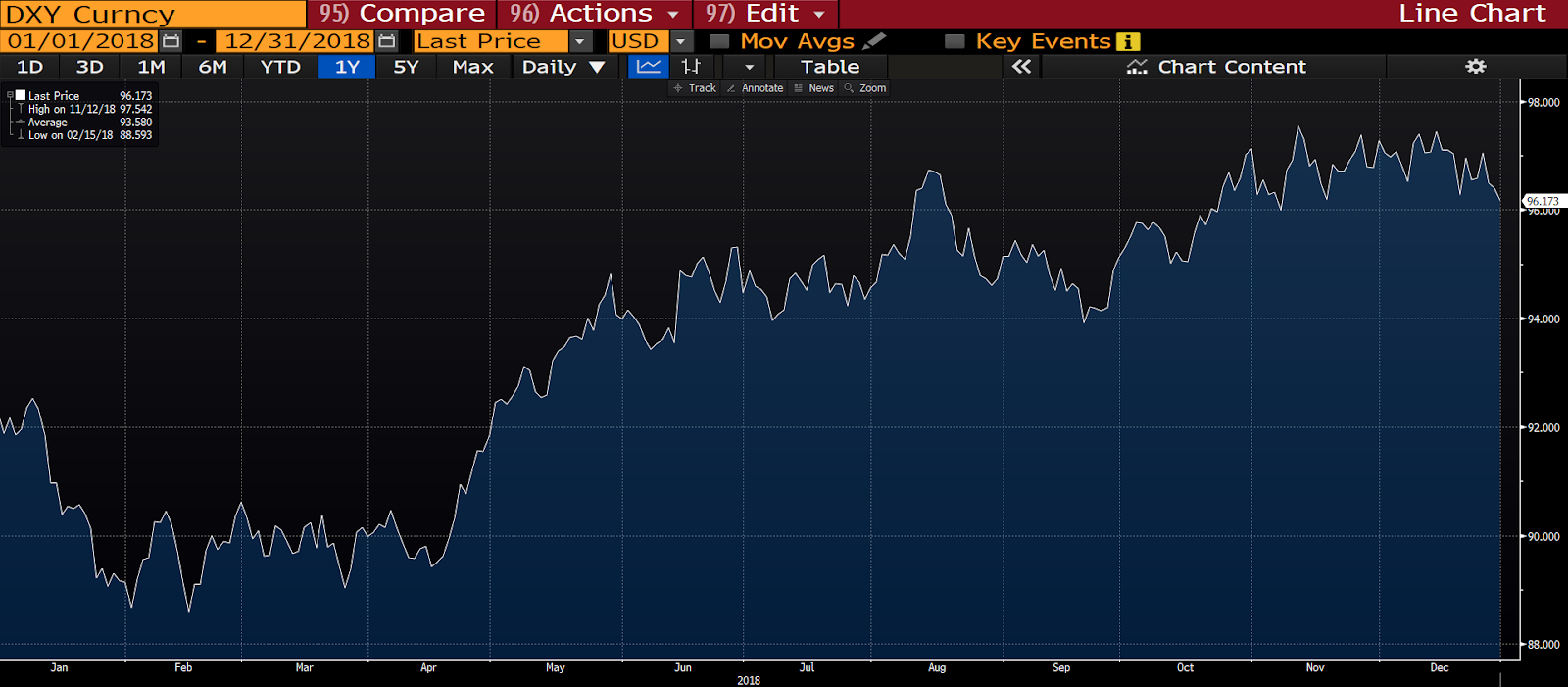

Well, we turned out to be right, and, alas, those headwinds indeed developed; which, along with the other, and more pernicious, risks associated with a trade war, left the stock market without the legs to avoid a steep Q4 correction.

Here’s how the U.S. dollar index fared in 2018:

Ironically, we were somewhat at odds with the currency pros at the start of 2017 as well. In last year’s letter we reminded readers of our position going in:

“….futures speculators were long the dollar to nearly the highest degree they’d been in 5 years, heading into 2017.

We actually were not in that camp. While we did not foresee a huge decline in the dollar in 2017, our view was that the Euro, in particular, was poised to do better on what we saw as the potential for a strong rebound in the Eurozone economy. I.e., while it was obvious that U.S. interest rates would trend higher in 2017 versus the Eurozone (conventional thought says traders migrate toward the currency with the highest yield), we expected that money would actually flow to Europe (as well as to the emerging markets) — creating a headwind for the dollar — based on opportunities in its asset markets.”

And here was the dollar during 2017:

So, ironically, again, here we sit again, with a forward view on the dollar that conflicts with currency speculators. They’re, at the moment, (in the aggregate) thinking the dollar’s due to strengthen.

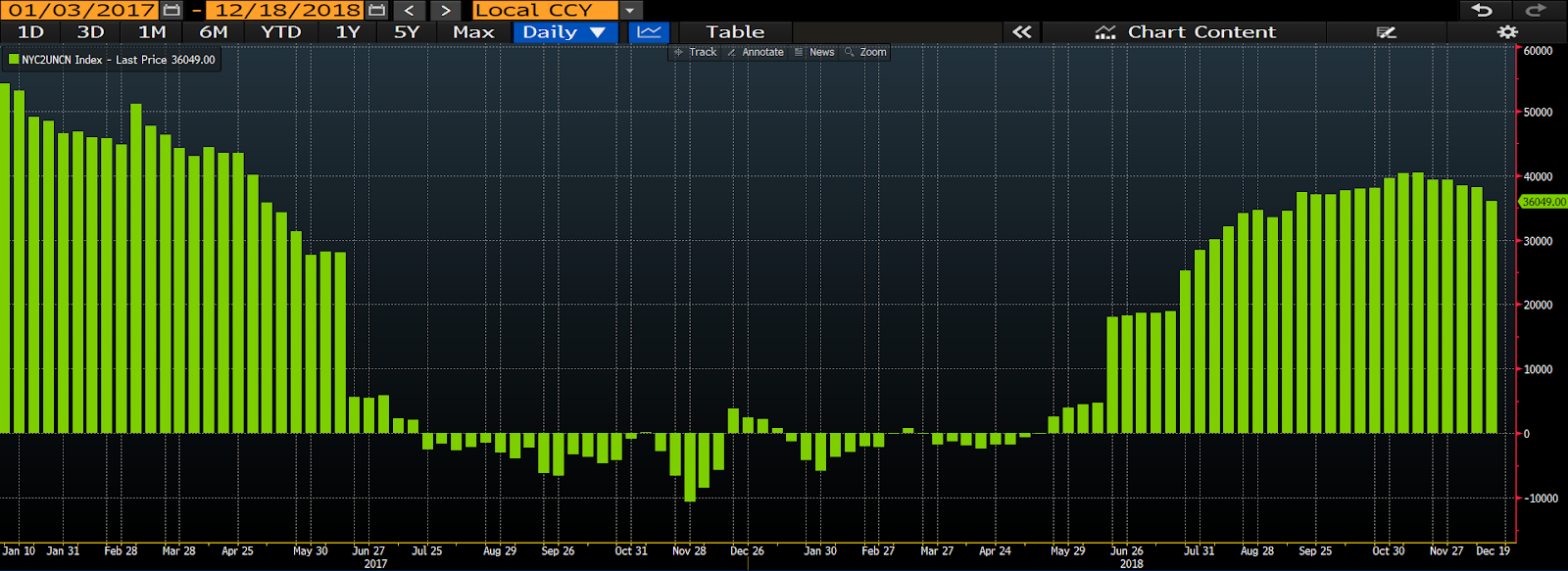

The chart below shows the last 3-year net positioning among non-commercial (speculators) futures traders in the U.S. dollar index. Note the bullishness heading into 2017 (we leaned bearish), the bearishness heading into 2018 (we leaned bullish) and the bullishness today (yes, we’re back to leaning bearish).

Here, in a nutshell, is our reasoning for presently leaning bearish:

- The European Central Bank, given the notable slowdown in Eurozone economic growth of late, has pushed out their projections for anything that would be deemed tighter monetary policy. And while some would say that that, leading to lower than otherwise Eurozone interest rates, would be bearish for the Euro (bullish for the dollar), our view is that it, bolstering the point we make in the next bullet point, will turn out to be net bullish (bearish for the dollar).

- European stocks are substantially cheaper than are U.S. stocks, and our view that a global recession is not in the 2019 cards suggests that there’s a decent chance that we’ll see a rotation from U.S. stocks to Eurozone stocks during the course of the year; a scenario that would be a net weakener of the dollar vs the Euro.

- While it’s a close call, we believe that the economic, and, thus, the political risk associated with a hard Brexit skews the odds in favor of a soft Brexit. That’s a scenario that would be substantially bullish for the pound, as well as the Euro, and bearish for the dollar.

- Emerging market currencies have clearly bottomed and look to be establishing a new up trend. Emerging market equities are notably cheap relative to developed markets and, in an end-of-the-trade-war scenario stand to see substantial inflows during the course of this year. Which is a decidedly bearish scenario for the dollar.

- The Fed has clearly moved to a markedly dovish position relative to where they were just a few months ago. While we presently anticipate a better economy this year than much of the recent data might predict (and, thus, a tighter Fed later in the year), any fear that the Fed was prepared to drain the punch bowl is currently off the table. Lower, or not-rising, U.S. interest rates is yet another bearish weight on the dollar.