Now I did subtitle my September 10 blog post “Expect a Rough Patch”, although I’m certainly not here to say “I told you so”.

While that message may have seemed prescient (as the market hit its peak for the year a mere 10 calendar days later), I definitely was not anticipating that by late December we’d be sitting on levels that make this particular “correction” the worst of the present bull market.

9/23 I Repeat Expect a Rough Patch

9/29 Rough Market Currently

10/6 Rough Road Ahead, Amid Still Bullish General Conditions

10/12 (in response to a strong rally): Don’t Call Your Friends Over (to celebrate) Just Yet

10/18 (in response to another strong several day rally) Expect a Test

10/20 (as that rally failed): Expect More of the Same For Now

10/22 Way Too Soon To Buy China’s Bounce!

10/29 When Will It End, And Is This A Good Time To Buy?(our response to that client question was; “we’re not rushing in”)

10/30 (as stocks were attempting a comeback): Hold Your Horses Folks

While the above perhaps make us appear really smart when it comes to assessing near-term market conditions, a number of our November and December posts — as (we now know) the titles reflected patently incorrect near-term optimism as well as, at times, near-term ambiguity — remind us of how critically important are numbers 6 and 7 of the traits listed in Part 1 of this year-end message:

6. An understanding of and appreciation for the uncertainty of markets

7. A flexible and open mind

11/6 Checking One Headwind Off Our List

Our conclusion in the following that the current price action in stocks deviates from overall general conditions speaks to what I wrote about Jesse Livermore in Part 1:

He was acutely aware of the habits of the investors and traders around him. He had to be, for he knew that the whims of ego-driven, emotional and impatient individuals at times created the most profitable market setups.

So how do we do that? We do that by testing the data that matter against the periods that led up to past recessions. And as we perform that function here today, the character of the data on balance (per our proprietary macro index) does not yet signal recession, and remains notably more positive than it was during the whopping 2011 correction, and slightly better than the 12+% draw down of early 2016, yet somewhat worse than conditions during the 2015 correction.

Here’s a small sampling of the data we track (shaded areas are recessions, I circled the areas around the 2011 correction and the back-to-back corrections of 2015 and 2016). I of course cherry-picked examples that emphasize my point, and those that most folks are familiar with and/or can relate to:

First, here’s the S&P 500 Index itself: click charts to enlarge…

Yes, right now the present price action in stocks rivals the worst of what we’ve seen since the last bear market.

But take a look at retail sales:

Online sales (purple) haven’t missed a beat since the last recession, although, as you can see, brick and mortar (white) has definitely had its ups and downs. Presently, however, it remains in a definable up trend. Nevertheless, we currently score it neutral, as it has yet to make a higher high after the last dip. That said, its trajectory looks notably better than it did during the past three corrections, let alone the periods leading into the past two recessions.

For the rest I’ll simply throw up each chart and let you judge whether or not the data should have us running for the exits.

Weekly Jobless Claims:

Unemployment Rate:

Job Openings:

Consumer Confidence:

Institute for Supply Management Purchasing Manager Surveys (manufacturing purple, services yellow):

Small Business Optimism:

Industrial Production:

Truck Tonnage

Rail Traffic

As you no doubt noted in the above, as it relates to the featured charts, present conditions do not remotely resemble recessions past, or even the 2011 and 2016 market corrections.

As for the remaining data we follow (which include indicators of credit risk, commodities trends, financial market conditions, etc.), and score, while we’ve seen marked deterioration since the beginning of the year, the overall result still has odds favoring continued expansion (and, thus, bull market) over recession (and a protracted bear market) for the foreseeable future: Our index presently scores +20, versus +8 during the 2011 correction, +29 in 2015 and +18 at the bottom of the 2016 correction. As for the past two bear markets, the back tests scored -29 at the 2000 market peak, and -33 at the 2007 S&P 500 all time high.

In summary, our assessment of the present state of stock market affairs is that the price action deviates from the underlying fundamentals. Of course the question here would be, will the price action ultimately reverse and reflect present fundamentals, or will the fundamentals ultimately roll over and reflect the action (the message?) in stock prices?

History suggests that this — a correction amid an ongoing economic expansion — is the stuff strong rallies are made of. And we’ve seen albeit minor hints recently of what might be in store — such as Wednesday’s initial, and extremely short lived, 400-Dow point surge in reaction to the Fed decision, and Friday’s 400-point pop on Fed governor Williams dovish commentary. Not to mention the +1,500-point week we had leading into the President’s untimely, and rally-killing, “I’m a Tariff Man” tweet.

Not to discount other pressing issues — government shutdown, the shocking James Mattis resignation, Fed rate hikes, and so on — but if the trade war makes its way too far into the not too distant future (which, thankfully!, would be a political nightmare [read incentive] for the players), I suspect that we’ll ultimately be staring down some ugly looking charts and a negative score for our index: A scenario that will have us committedly moving to a defensive posture within client portfolios sooner, alas, than we otherwise would have.

—————————————————————-

As for the market technicals, well…. they’re presently ugly!

Here’s our 2-year daily chart of the S&P 500 Index. Note the breakout below what we’d term a consolidation box, then Monday’s penetration of last year’s March to July support level (red line) like it wasn’t even there:

Now that’s the definition of bearish-looking technicals.

To make matters scarier still, compare the above to this two-year chart ending in January 2008:

Here’s the rest of that story:

How about this setup in 2001:

YIKES!!

Now before you go pounding your keyboard with your email with the subject line “GET ME OUT!!” to yours truly, take a look at this 1998 chart:

OOPS! (to the traders who sold it):

How about this one from 1997:

Dang! A disaster for the sellers:

Here’s that 2011 nightmare of a correction:

Well…. a nightmare for the bears:

And, lastly — while there was technically no false breakout below consolidation — here are the back-to-back 2015/2016 corrections:

Again, it paid to be patient:

While we should absolutely pay attention to breakouts from previous support, or resistance, levels, clearly, there’s more work to be done before concluding that action should be taken.

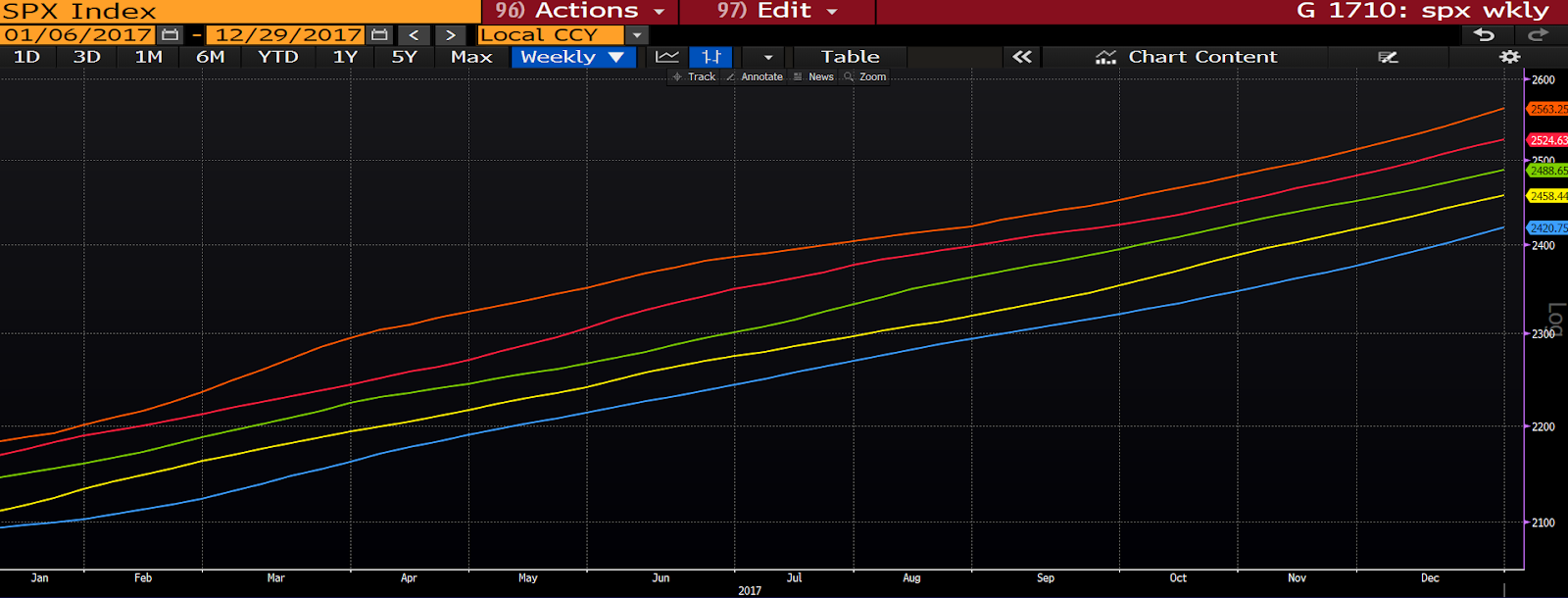

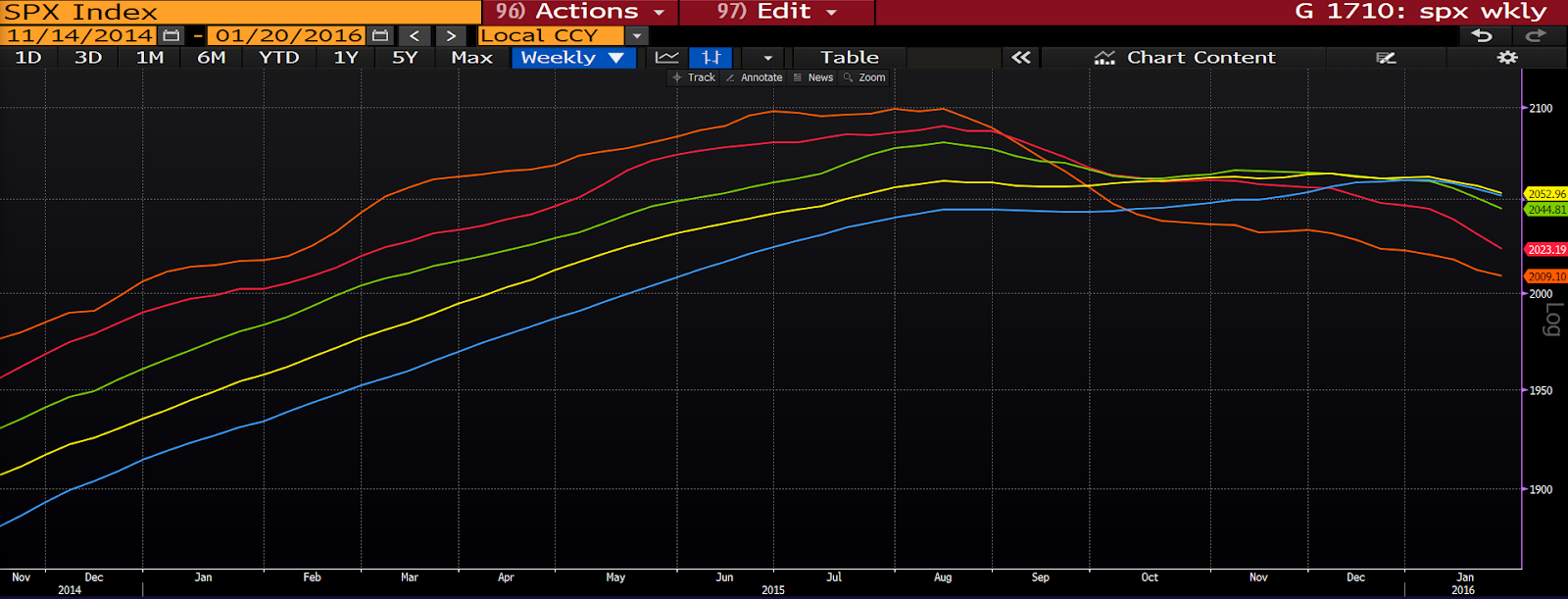

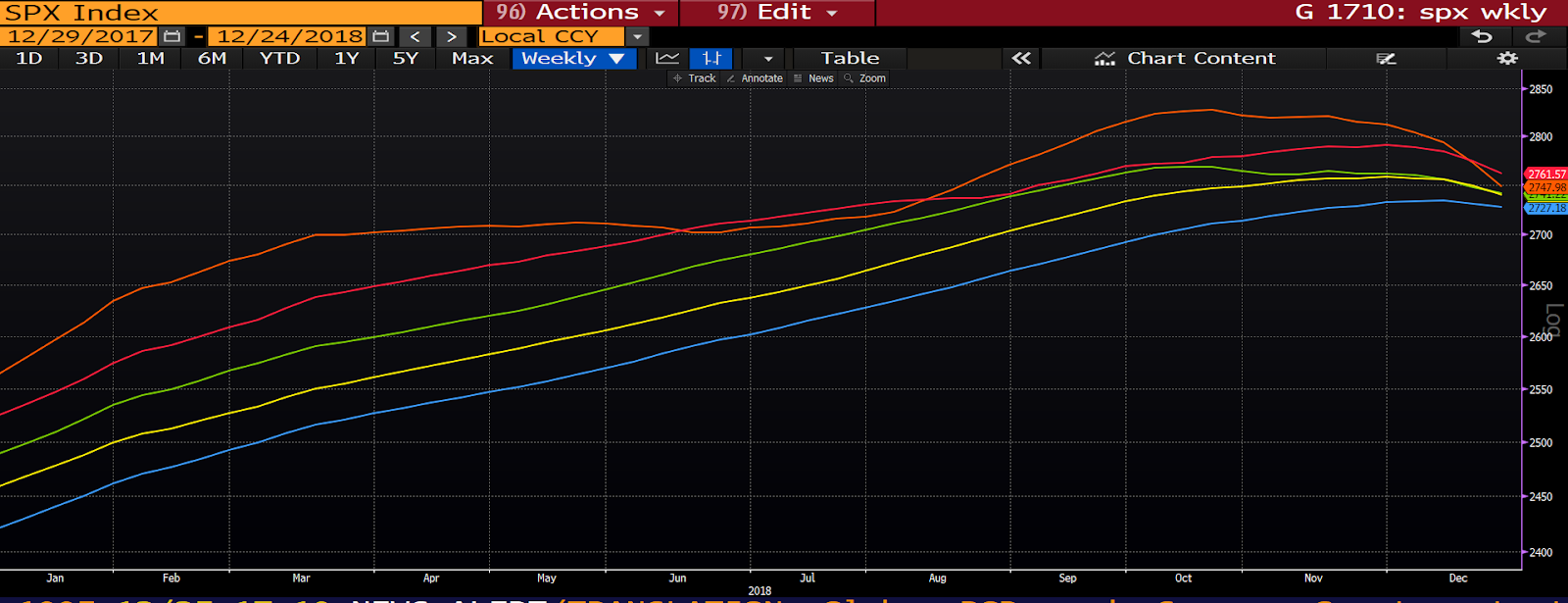

Sticking with the technicals, here’s what a bullish setup (calendar year 2017) looks like using the 20, 30, 40, 50 and 60-week moving averages for the S&P 500 (fastest [shortest] moving average on top, slowest on the bottom, all sloping upward):

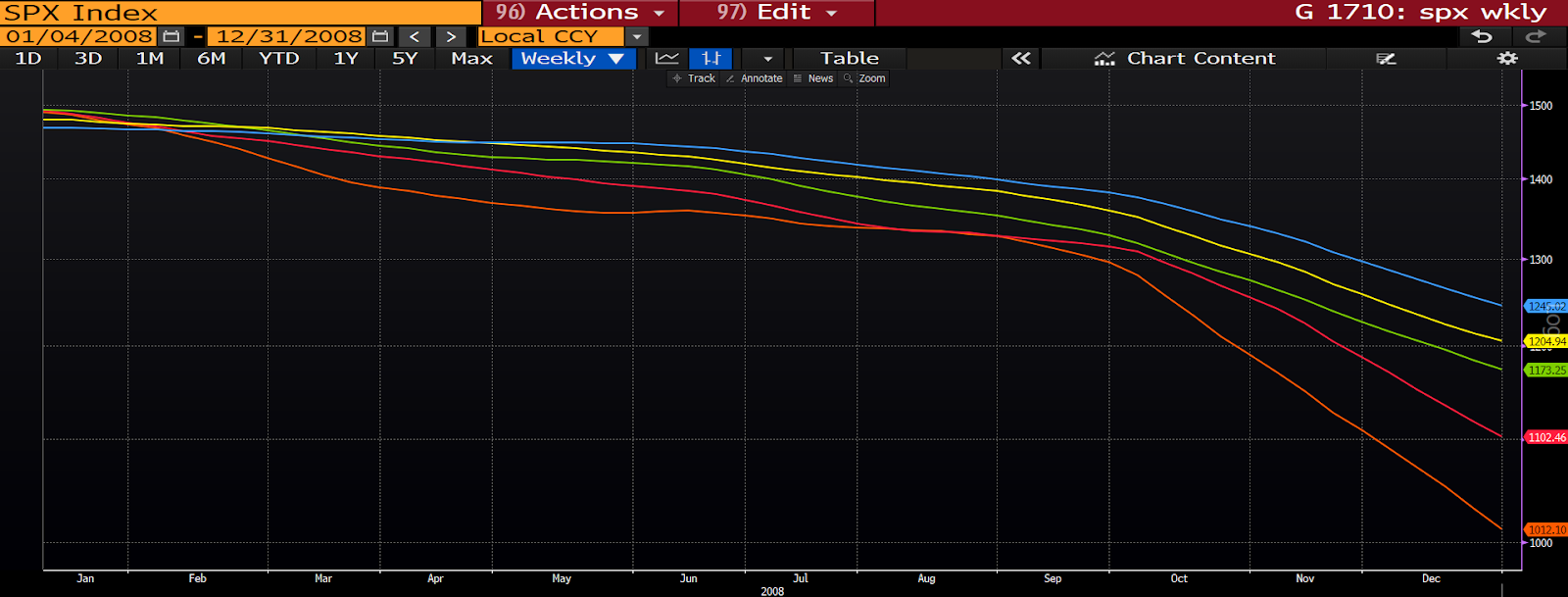

Here’s what a bear market looks like (calendar year 2008):

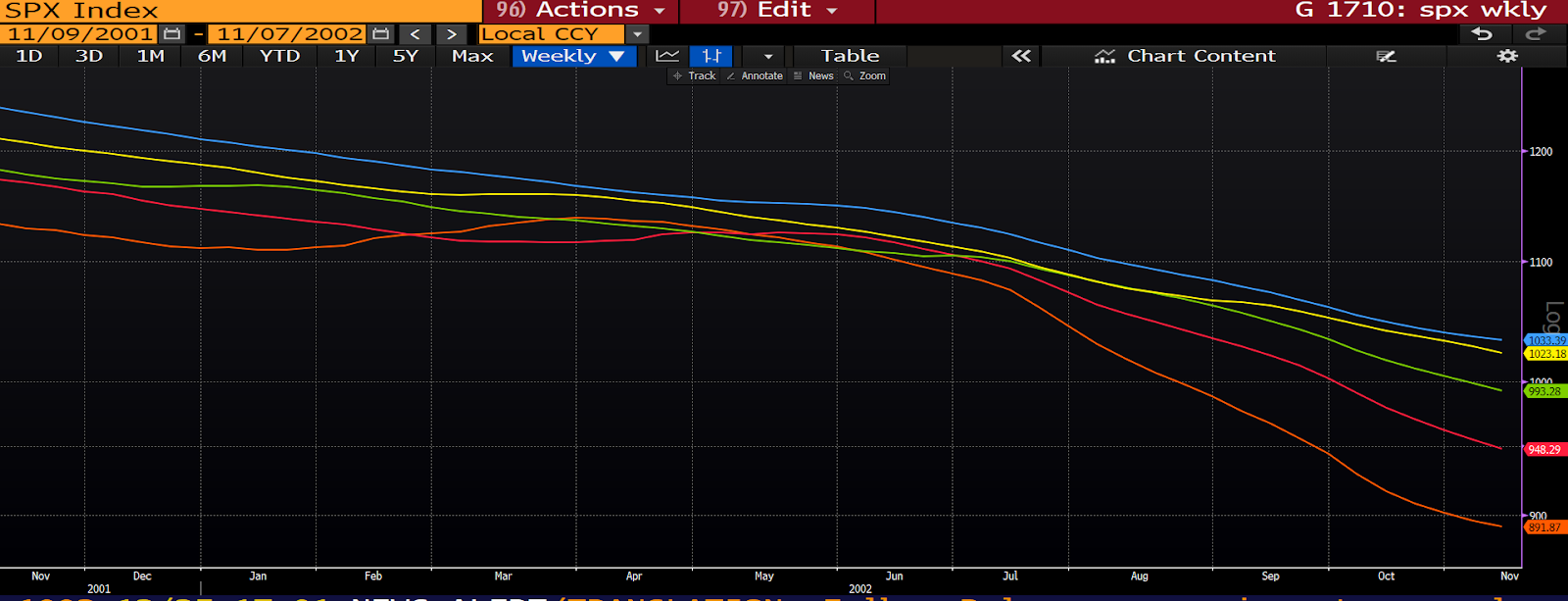

And here’s the look during the previous bear market (early 2000s):

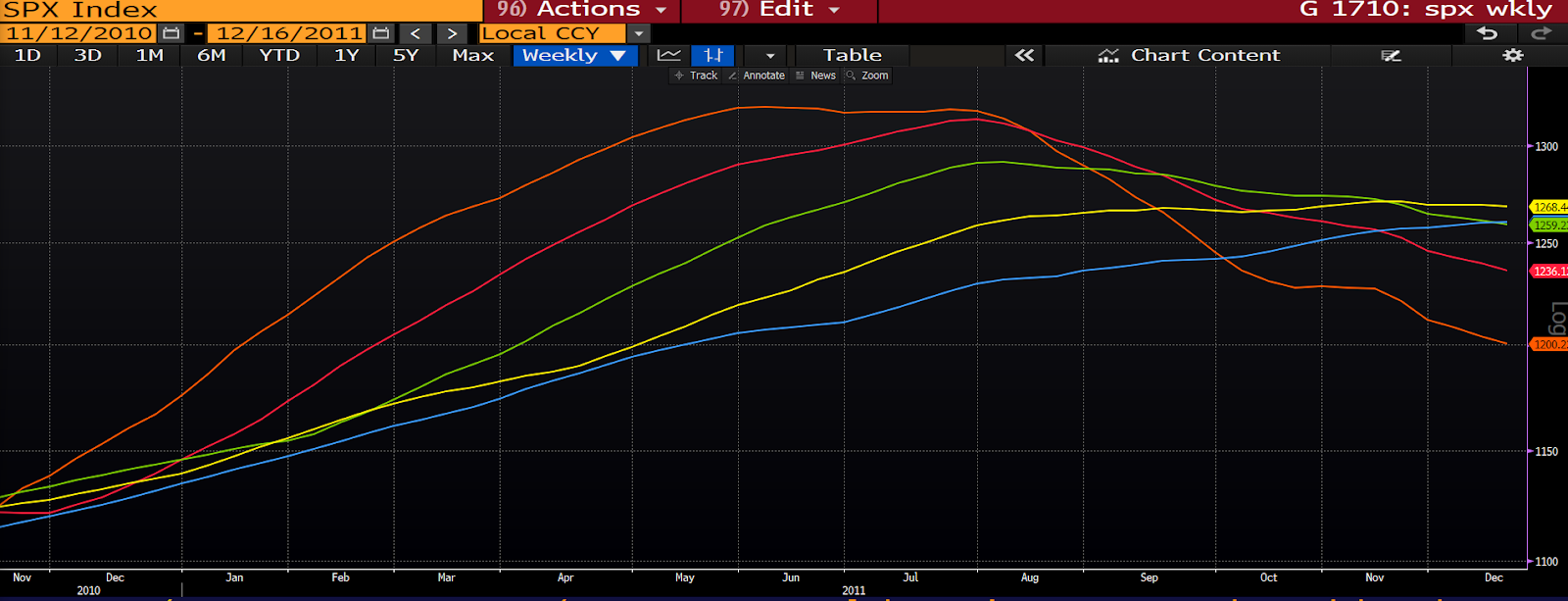

Here’s the concerning (but inconclusive) look during the 2011 correction — that turned out to be a monster buying opportunity:

Here’s an equally concerning look from the ’15, ’16 corrections — that also turned into a great buying opportunity:

And here’s how they line up as we sit here today:

Definitely not a bullish signal, but not nearly as bearish as the setup at this point during even the previous corrections (that turned out to be simply pauses) of the present bull market.

So, from a purely technical perspective, while today’s setup absolutely looks concerning, it would be premature at this juncture to conclude that we are in the throes of the next protracted bear market.

Here’s where general fundamental conditions, our ultimate determining factor, come in.

This 20-year weekly chart of the S&P 500 features the back tests of our PWA Index, with the lead-ins to the featured time periods above circled (corrections in green, bear markets red, current period yellow) — red shaded areas are recessions:

As you can see, the macro data was screaming recession as the market was peaking ahead of the past two bear markets, while the economy held up through all of the corrections (which is why they remained corrections) in between.

Yes, while anything can happen, the present setup morphing into a protracted bear market would be unusual, with history as our guide (although we remain open to all possibilities); which explains why we’re not at this point rotating to a defensive posture within client portfolios.

Lastly, and on a sour note, the following from a Christmas day article from Bloomberg Economics drives home why we see the “trade war” as THE macro risk going forward.

“By Enda Curran and Katia Dmitrieva(Bloomberg) — While 2018 was the year trade wars brokeout, 2019 will be the year the global economy feels the pain.

Bloomberg’s Global Trade Tracker is softening amid a fading rush to front-load export orders ahead of threatened tariffs. And volumes are tipped to slow further even as the U.S. and China seek to resolve their trade spat, with companies warning of ongoing disruption.

Already there are casualties. GoPro Inc. will move most ofits U.S.-bound camera production out of China by next summer, becoming one of the first brand-name electronics makers to take such action, while FedEx Corp. recently slashed its profit forecast and pared international air-freight capacity.

“Any kind of interference with commerce is going to be atax on the economy,” said Hamid Moghadam, chief executive officer of San Francisco-based Prologis Inc., which owns almost 4,000 logistics facilities globally. “And the world economy is probably going to slow down as a result of it.”

Financial markets have already taken a hit. Bank of America Merrill Lynch estimates that the trade war news has accounted for a net drop of 6 percent in the S&P 500 this year. China’s stock market has lost $2 trillion in value in 2018 and is languishing in a bear market.”

Recent data underscore concerns that trade will be a dragon American growth next year. U.S. consumers are feeling the least optimistic about the future economy in a year, while small business optimism about economic improvement fell to a two-year low and companies expect smaller profit gains in 2019.”

The good news is it’s probably not too late (but I fear we’re getting close) to do an abrupt about face (trade war truce) and see equity markets reflect a continuation of what was at the beginning of this year a globally synchronized, robust, economic expansion — although we should doubt, given the damage already done, whether “globally sychronized” and “robust” will be apt descriptions going forward.