As for what it says about the present state of the economy — it’s full steam ahead!

What’s interesting is, save for the Chicago PMI — notwithstanding the below-the-surface pressure you’ll note below — it’s tamer on inflation than I might’ve guessed at this juncture.

The color of my highlights reflects how I view the message from each point highlighted.

Note: In case you wonder why I colored the decline in the consumer’s bullishness on the stock market green, well, individual investor sentiment has historically been one of the best contrary indicators.

Click each chart to enlarge…

Highlights

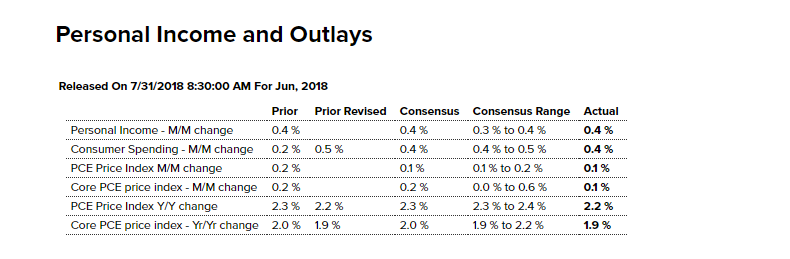

Easing inflation pressure along with healthy consumer vital signs is the message from the personal income & outlays report for June. Both price indexes, the overall and the closely watched core rate which excludes food and energy, posted only marginal 0.1 percent gains in June with year-on-year rates favorable, at 2.2 percent overall and at 1.9 percent for the core, both unchanged from downwardly revised results in May. The movement in inflation is coming back toward the Fed’s 2 percent target line, not away from it.

Personal income rose a useful 0.4 percent with the wages & salaries component also at 0.4 percent. The savings rate was shifted sharply higher in last week’s benchmark GDP revisions in what is a very fundamental sign of health. The savings rate held unchanged in June at 6.8 percent.

The consumer didn’t dip into savings to keep up spending which was a solid 0.4 percent with May revised sharply upwards, from an initial 0.2 percent gain to 0.5 percent. Spending on services rose 0.6 percent in June to offset what is a small disappointment in today’s report which is no change in spending on durables.

The inflation readings in today’s report are complemented by a little less pressure in the employment cost index which was also released this morning. Together, they ease the pressure on the Federal Reserve and may help to keep down any hawkish edge to Wednesday’s FOMC statement.

Highlights

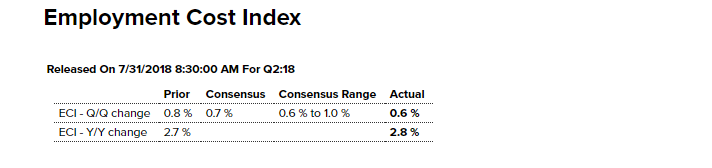

Slowing in wage costs kept down the employment cost index in the second quarter, coming in at a 0.6 percent gain which is at the low end of expectations and down noticeably from the first quarter’s 0.8 percent gain.

Wages & salaries rose only 0.5 percent in the quarter, well down from 0.9 percent in the first quarter in what will be a relief for Federal Reserve policy makers who are on the watch for wage pressures given the strength of the labor market. But there is cost pressure for employers and that’s in benefits which had been behaved but did rise 0.9 percent in the latest quarter.

And year-on-year rates actually ticked higher, up 1 tenth overall to 2.8 percent which is the same result for the wages & salaries component. The benefits component rose 3 tenths to 2.9 percent.

This is a mixed report but the slowing in quarterly wages is a tangible positive and complements the modest inflation readings in this morning’s personal income & outlays report.

Highlights

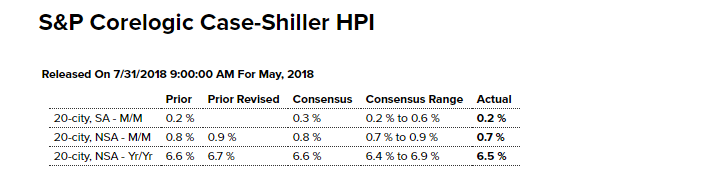

Weakness in the major cities in the Northeast and Midwest is offsetting price strength in the West making for a soft 0.2 percent rise in the Case-Shiller 20-city adjusted index for May, a result that comes in at the bottom of Econoday’s consensus range.

Home prices in New York City fell 0.3 percent in the month with Detroit down 0.2 percent. Washington DC was unchanged with Chicago up only 0.1 percent. At the opposite end, Seattle continues its 1 percent monthly clips, rising 1.4 percent in May. Phoenix has also been very strong, up 0.8 percent in the month with San Francisco up 0.5 percent.

Year-on-year rates are led by Seattle at 13.6 percent with Las Vegas at 12.6 percent and San Francisco at 10.9 percent. These rates raise questions whether these are markets are in the bubble zone. On the bottom end are Washington DC at 3.1 percent, Chicago at 3.3 percent, and New York at 4.2 percent.

Total year-on-year prices came in at 6.5 percent, down 2 tenths from a revised April and below Econoday’s consensus which is also the result for the monthly unadjusted gain at 0.7 percent.

Despite the strength in the West, both this report and the FHFA house price index have visibly slowed the last several reports, in line with what has proven, in contrast to all the strength in the labor market and the health in consumer spending, to be a downshift in this year’s home sales.

Highlights

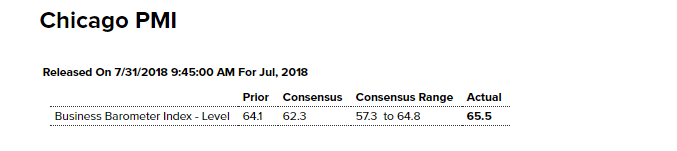

The Chicago PMI continues its torrid pace, at 65.5 in July to top Econoday’s consensus range and the strongest showing since January this year. New orders and production are also the strongest since January with backlogs the highest since October last year.

The pressure is being reflected in prices with input costs at their highest level of the ongoing expansion, since September 2008. The report notes that price pressures are also attributable to recently imposed tariffs on imports. Delivery times remain elevated and are contributing to an inventory draw down of raw materials. Skilled labor is still in short supply but the sample is nevertheless adding staff.

Rising costs and capacity stress aside, the Chicago sample’s confidence is strong with over half expecting third-quarter orders to exceed those of the second quarter.

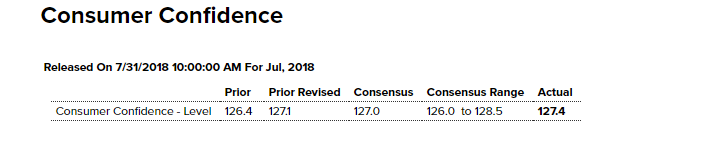

Highlights

Consumer confidence is steady and strong, at 127.4 in July to beat out Econoday’s consensus by 4 tenths. Assessments of the labor market also remain strong with those saying jobs are currently hard-to-get nearly unchanged at 15.0 percent and those describing jobs as plentiful up nearly 3 percentage points to 43.1 percent. These readings are inputs into the present situation component which rose to 165.9 from 161.7 in a gain that points to July as another month of consumer strength.

Unlike the present situation, the expectations component eased back by more than 2 points to 101.7. The dip reflects a little less optimism on income prospects and a little less optimism on future job prospects.

One reading that will catch the eye of FOMC policy makers at this week’s meeting is a 2 tenths rise in inflation expectations to 5.1 percent. This is still a moderate indication for this particular reading but the direction is clearly upward, moving from 4.7 percent as recently as April.

A weakness in the report is a sharp 1 percentage point drop to 5.1 percent in buying plans for homes in what is the latest unfavorable news for home sales. The assessment of the stock market is less bullish with the bulls down more than 6 points to 36.5 percent and the bears up nearly 7 points to 29.4 percent.

It’s hard to make further upward movement in this report given its enormous strength, right at nearly 20 year highs. But the kicking in of inflation expectations is something new and does coincide with very clear inflation pressures being reported by manufacturers all year.