You’d think investors would be feeling pretty good right about now.

After all, the earnings season thus far has been all (actually, more than) it was billed to be; 73% of reporting companies have beaten expectations on the bottom line, with growth rates at multi-year highs. As, if not more, importantly, top line beats are coming in at a remarkable 71% clip.

Not to mention the fact that the economy (the U.S. economy in particular) continues to expand at a healthy pace; our PWA Macro Index has increased in 3 of the past 4 weeks, with this morning’s reading coming in at an historically healthy +61.

Yet the market hasn’t been able to make any real headway, despite having set the stage with a double-digit correction heading in.

1. The normal, cyclical, inflection point angst generated by the transition to a higher interest rate regime: A scenario that essentially confirms that the economy is in good shape and that it’s time for the Fed to accelerate the process of reclaiming the liquidity that it pumped into bank reserves in response to the 2008 recession, as well as move to a higher policy rate level from which it can perform meaningful stimulus when needed later.

2. The palpable uncertainty inflicted by Washington’s protectionist actions — and further threats of the same. This couldn’t have come at a worse time for the present bull market, as:

- It essentially introduces an element of tightening (threatening the pace/existence of the expansion) that gets directly in the way of the Fed’s attempts at restocking its ammunition with which to battle the next recession: This tightening is showing up in the expectations components of multiple business surveys; i.e., corporate decision makers have become guarded in their outlooks, citing the threat of a trade war as the source of their uncertainty.

- The already enacted steel and aluminum tariffs are reportedly showing up in input costs (read higher prices/lower profits and/or eventually lower sales).

- The stifling of foreign imports will ultimately lead to less globally-circulating U.S. capital (the U.S. dollars we buy foreign stuff with) with which to buy U.S. government debt, while the treasury takes a hit to income via the latest tax cuts — after passing a monster 2018 spending package — not to mention erecting an emotional barrier between our U.S. treasury auctions and the foreign investors (the traditional buyers of treasuries) who will suddenly feel like trade enemies. I.e., a trade war ultimately risks even higher interest rates.

As for the healthy U.S. economy, here’s a look at the latest manufacturing purchasing managers surveys from the developed world: Click any chart below to enlarge…

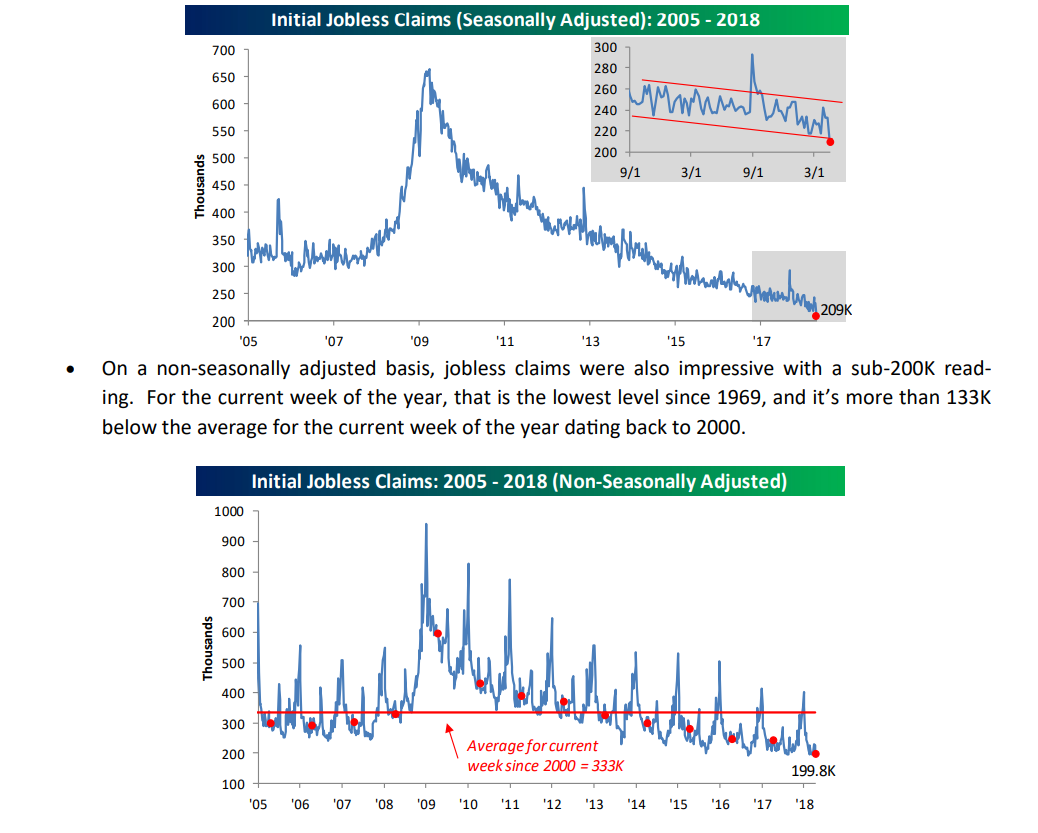

And of course we really need to look no further than the jobs market to determine the state of the U.S. economy: Weekly jobless claims just set a new record for consecutive weeks below 300k. The old record occurred over 40 years ago, when the U.S. population was 100+ million fewer!!

“Economic activity around the world remains positive, but it has clearly downshifted from the burst in activity that we saw in the second half of 2017 with Europe leading the weakness and US/North America holding up the best.”

As for our stated concerns regarding the prospects for foreign trade, here’s from various sentiment surveys captured in our April trends file: Click any snip or chart below to enlarge…

Central banks may be losing their appetite for Treasuries just as supply is set to ramp up. The amount of U.S. government bills, notes and bonds held in custody at the Federal Reserve Bank of New York fell to $3.06 trillion as of April 25, down from a record high of $3.11 trillion reached in March, data released Thursday show. The decline suggests that “some foreign official institutions may be reducing Treasury holdings in response to global trade tensions,” Amherst Pierpont Securities global strategist Robert Sinche wrote in a note Friday.

In summary:

Issue #1 above is actually productive, as the rising interest rate “angst” will weed out some of the excesses, as well as the weak players (fearing a bear market before its time), that/who have accumulated during this long bull market, while setting the stage for what is typically a period of positive correlation between rising interest rates (amid an accelerating economy) and stock prices. Higher rates become problematic later as the cycle begins to peak.

Pragmatically-speaking,

the potential political fallout resulting from economic and equity market pain at the hands

of a U.S.-led trade war would be so severe that it virtually assures that one

either doesn’t come to pass, or comes to pass then comes to truce shortly after

the first shots are fired. At the point of positive resolution – presuming the

macro setup hasn’t markedly deteriorated by then – probabilities (no guarantees) will favor an equity market advance to fresh all time

highs; inspired by strong economic fundamentals and the anticipated earnings

boost resulting from the corporate tax cuts, deregulation and, in some sectors, increased government

spending.

optimistic scenario is based on general conditions remaining supportive of

corporate earnings growth going forward.

election prospects have yet to become a factor.

maintain our long-term bias to cyclical sectors until the data instruct

otherwise…

Marty