Much like other head-scratching phenomena (read tweets and other public commentary of an impulsive nature) of the past year+, the latest calls for anything but knee-jerk reaction. It does, however, demand that we assess our various areas of exposure to what in my humble view is the most ill-advised impulse thus far.

Of course you know I’m talking about the pending tariff scheme that was announced against the passionate pleas of his most capable economic and national security advisers.

So that — assessing our exposures — is what we’re up to this morning.

Part of that process is to consider how important our exposure to multinational U.S. companies has been of late.

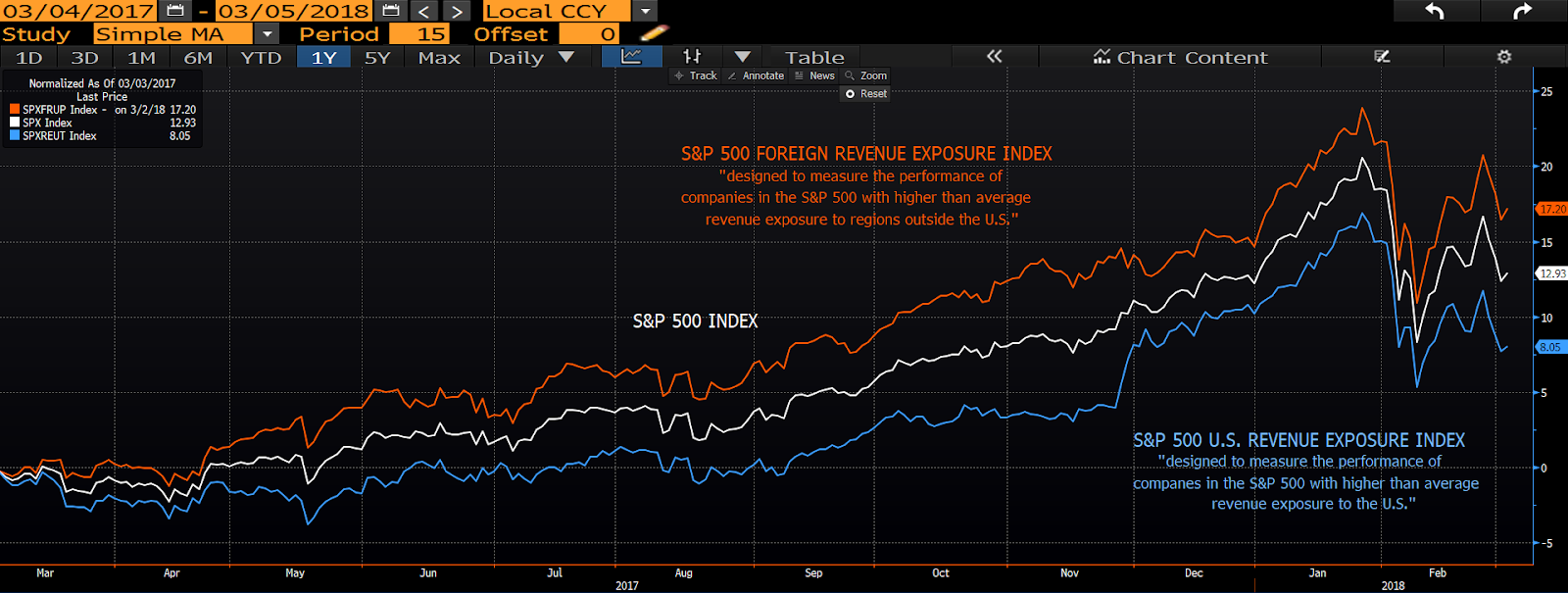

One way we do that is with our chart that compares the S&P 500 Foreign Revenue Exposure Index (designed to measure the performance of S&P 500 components that do much of their business outside U.S. borders), to the S&P 500 itself, as well as to the S&P 500 U.S. Revenue Exposure Index (designed to measure the performance of components with predominantly U.S. exposure). And when we do we can see how important our exposure to U.S. globally oriented companies has been of late.

The more internationally connected companies as a group have outperformed the S&P 500 itself by a whopping 33% (17.20% vs 12.93%), and it’s U.S. revenue-centric components (8.05%) by an astounding 114% over the past year:

Bottom line folks: It’s a big world out there and U.S. companies have been taking full advantage of it! Which by the way is huge in explaining how we (a mere 4% of the world’s population) wield far and away the world’s largest economy.

I’m showing you this to help you understand just one of the reasons why the market is all pins and needles over protectionism…