Of course we have no problem with the prospects for a peak in housing, and/or, that the economy is losing steam; in fact we’re forever on the lookout for clues pointing in that direction. However, it appears that at this juncture there’s something else afoot. Which looks to be, simply, a general lack of supply (of course higher mortgage rates are indeed not helping).

Per Bloomberg’s commentary this morning:

Lack of supply is a key factor holding down sales along with rising mortgage rates, at an average of 4.64 percent for 30-year mortgages as reported earlier this morning by the Mortgage Bankers Association. Regional sales data show wide declines especially for the Northeast which had been rebounding in prior months.

And the National Association of Realtors chief economist Lawrence Yun:

“The economy is in great shape, most local job markets are very strong and incomes are slowly rising, but there’s little doubt last month’s retreat in contract signings occurred because of woefully low supply levels and the sudden increase in mortgage rates, the lower end of the market continues to feel the brunt of these supply and affordability impediments.”

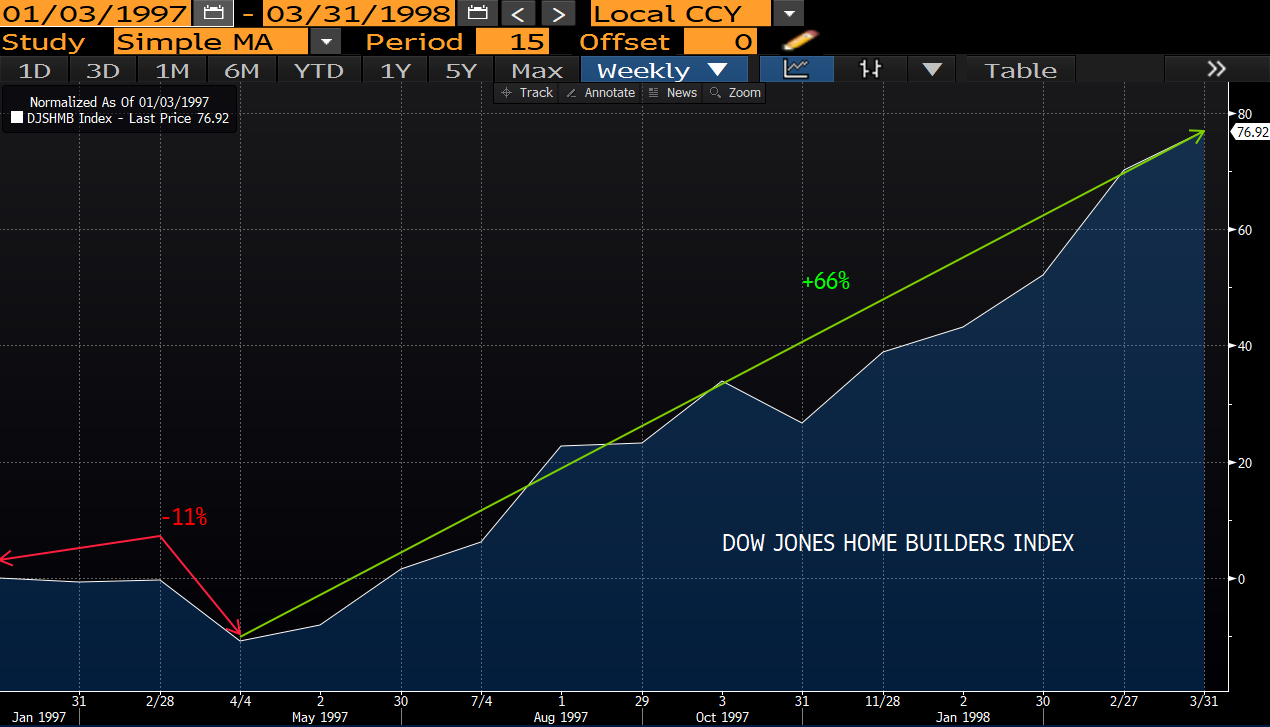

Given the general state of the economy, the employment picture (as Yun points out), and very bullish commentary from home builder surveys, things kinda (save for the near-term prospects for GDP growth) feels like 1997 to us.

Per author Gabriel Burstein:

… home building stocks/building materials stocks follows on long-term scale the quarterly percentage change in the U.S. GDP. A clear divergence appears between the two at the end of 1996. The economy is booming, but fears of the Federal Reserve Bank again using interest rate hikes to slow down the economy keeps home building stocks behind building materials stocks. As it becomes more and more clear that we have a noninflationary growth and as the GDP growth itself slows down, home building confidence pushes home building stocks up and closes down a wide mispricing gap.

Here’s our chart that jibes with Burstein’s analysis:

click to enlarge…

The following headline from yesterday supports our present thesis as well:

Home prices surge 6.3% in December amid critical housing shortage

- U.S. home prices increased 6.3 percent compared with December 2016, according to the much-watched S&P CoreLogic Case-Shiller national home prices index.

- The boom is strongest in Seattle, Las Vegas and San Francisco, which reported the highest gains. Chicago, Cleveland and Washington, D.C., saw the smallest gains.

- None of the top 20 markets saw an annual price decline.

Now, all that general bullishness aside, as portfolio managers we have to assess each holding and determine whether it is in our view well-positioned for the longer-term going forward — short-term volatility never bothers us when the long-term setup makes sense. And, most importantly, whether the size of each position portfolio-by-portfolio fits with our view of each client’s ideal sector weightings as well as their goals and tolerance for risk.

With the above in mind, we’re presently reviewing each portfolio that holds our core home building sector (a sub sector of consumer discretionary) ETF (XHB) and in some instances we may pair it back with the proceeds going to XLY, our core consumer discretionary ETF. XLY offers more diversified exposure (which includes housing-related stocks) to the industries where healthy consumers spend their cash.

Bottom line: While we remain constructive on the housing sector, we need to accommodate for the fact that higher interest rates, tight supply, high land and rising labor costs are headwinds going forward.