Part 1: What Makes Us Tick

Of course we’ll do the obligatory roundup of returns, show off our economic indicators, tell you what sectors we like and don’t like going forward, and see how our opinions of a year ago played out. But how do we get it all started in a way that’ll inspire you to remain engaged throughout this year’s yarn?

For starters, here are what we believe to be the essential characteristics of really good investment managers. And, we’re proud to say, we believe they capture the spirit of what we do/how we think here at PWA:

Are you bewildered by how well the market has held up against 2017’s political and geopolitical winds? Of course such winds were prevalent in the days of Jesse Livermore as well. Here’s what he learned:

“Not even a world war can keep the stock market from being a bull market when conditions are bullish, or a bear market when conditions are bearish. And all a man needs to know to make money is to appraise conditions.”

He was acutely aware of the habits of the investors and traders around him. He had to be, for he knew that the whims of ego-driven, emotional and impatient individuals at times created the most profitable market setups. Plus, they forever reminded him of the many ways not to trade markets:

“It is the way a man looks at things that makes or loses money for him in the speculative markets. The public has the dilettante’s point of view toward his own effort, the ego obtrudes itself unduly and the thinking therefore is not deep or exhaustive. The professional concerns himself with doing the right thing, rather than with making money, knowing that the profit takes care of itself if the other things are attended to.

If I said to the average man “sell yourself five thousand steel” he would do it on the spot. But if I tell him that I am quite bearish on the entire market, and give him my reasons in detail, he finds trouble in listening. And after I am done talking he will glare at me for wasting his time expressing my views on general conditions, instead of giving him a direct and specific tip — like a real philanthropist of the type that is so abundant on Wall Street, the sort who loves to put millions in the pockets of friends, acquaintances and utter strangers alike.”

And, in the end, he learned that patience was an essential ingredient to his success:

“After spending many years in Wall Street and after making and losing millions of dollars I want to tell you this: It never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight!”

We can’t express enough — per the following excerpt from an earlier blog post — how we sympathize with Livermore’s point: “The professional concerns himself with doing the right thing, rather than with making money, knowing that the profit takes care of itself if the other things are attended to.”

Earlier this year, after playing basketball, I stumbled onto an analogy that I believe best describes how we approach the managing of client portfolios. Which, by the way, also describes how we can sleep at night while accepting such a colossal responsibility. Here’s from our May 21 blog post:

I play a lot of basketball, and, as my son and the dudes I play with will attest, I like to attempt three-pointers. In that success enhances the enjoyment of virtually any endeavor, I knew from the start (my late start [not surpassing the 5’5″ mark till after highschool and, thus, being a wrestler during my formative years]) that if I was to score enough to justify my itchy trigger finger, I had to learn good shooting fundamentals. While I’m fully aware that 100% from the field is infinitely beyond my reach, I know that if I can stay in rhythm, if my form is sound and if I practice good shot selection, my odds of maintaining a respectable enough percentage to keep me from being the lowly last pick come time to select the teams increase dramatically.

Different players bring different talents to the game. There’s a young man we play with, we’ll call him Bartholomew (just in case he happens to stumble upon this blog post) who possesses exceptional ball handling ability and plays the point beautifully. Surprisingly, however, his outside shooting leaves much to be desired. So much so that when he launches a three his teammates cringe; hoping the ball finds nothing but air. Now why would his own teammates want Bart to miss his shot, in embarrassing fashion no less? Because they know that if he drains it, their odds of winning will decrease exponentially.

You see Bart believes that a shot that goes in has to be a good shot. Therefore, when he makes one he believes that he possesses the fundamental makings of a good shooter — and good shooters shoot. So he shoots and he shoots and he shoots and, in reality not having mastered good shooting fundamentals, he misses and he misses and he misses and, alas, his team loses.

We can sum up basketball shooting as follows. There are:

1. Good shots that go in.

2. Good shots that miss.

3. Bad shots that miss.

4. Bad shots that go in.

#1’s are great. #2’s are fine, unavoidable, and possess a liveable probability rate. #3’s, while costly, are the most predictable and, therefore — being costly — should be readily avoided. #4’s — as explained above — are an utter curse!

Here’s my point:

We can sum up investing as follows. There are:

1. Good investments that make money.

2. Good investments that lose money.

3. Bad investments that lose money.

4. Bad investments that make money.

#1’s are great. #2’s are fine, unavoidable, and possess a liveable probability rate. #3’s, while costly, are the most predictable and, therefore — being costly — should be readily avoided. #4’s: I can’t think of a worse case scenario than a new investor hitting a #4 right out of the gate. The perverse feedback from that experience could absolutely send him or her to the poorhouse — as he or she might think that he or she’s discovered a high probability investing method and chalk up the subsequent string of losses to rotten luck. I.e., believing what are in reality #3’s to be #2’s. The emotional imprint from that early “success” may indeed last longer than his or her capital.

Bottom line, while good investments can, and often do, lose money, if we take only shots where the setup makes good sense — i.e., if we take only good shots — and we take them from multiple angles and distances (diversify), we believe that we give our clients the absolute best odds of achieving long-term investment success.

As for how we determine whether a given setup — for an asset class, a sector, a region, and the market overall — is one to embrace or to fade, we’ve developed our own technical and fundamental methodologies that our experience and backtesting suggest do a good job of, as Livermore put it, appraising conditions. Which will provide the basis for much of what you’ll read in parts 2 and 3.

Part 2: General Conditions

While it’s tempting to post herein the charts representing the 73 entries to our predominantly U.S. (12% of the data points reflect global conditions) macro model — which organizes and scores the data that instruct our view of general conditions — in the interest of keeping you interested we won’t. Instead, we’ll offer up recent overall scores and illustrate why a thoughtful analysis of macroeconomic conditions — in addition to robust technical analysis — is critical to our confidence level as we manage client portfolios.

In terms of what our system tracks: 71% of our model is comprised of hard (jobs numbers, housing starts, industrial production, etc.) and soft (sentiment) data related to consumer and business activity, to inflation, to general financial stress, to commodity trends and to “other/general economy”. The remaining 29% is devoted specifically to U.S. equity market internals.

On January 1 of this year our macro score came in at +42, with 69% of the data reading positive, 10% negative and 21% neutral. Hence — along with a bullish technical setup — our optimistic view of equity market probabilities coming into the year.

In case you’re wondering, the setup back in June of 2016 was nothing to sneeze at either; with our macro score coming in at +29, with 56% of the data reading positive, 16% negative and 28% neutral.

Now we’ll dig into why we do so much work on macroeconomic fundamentals.

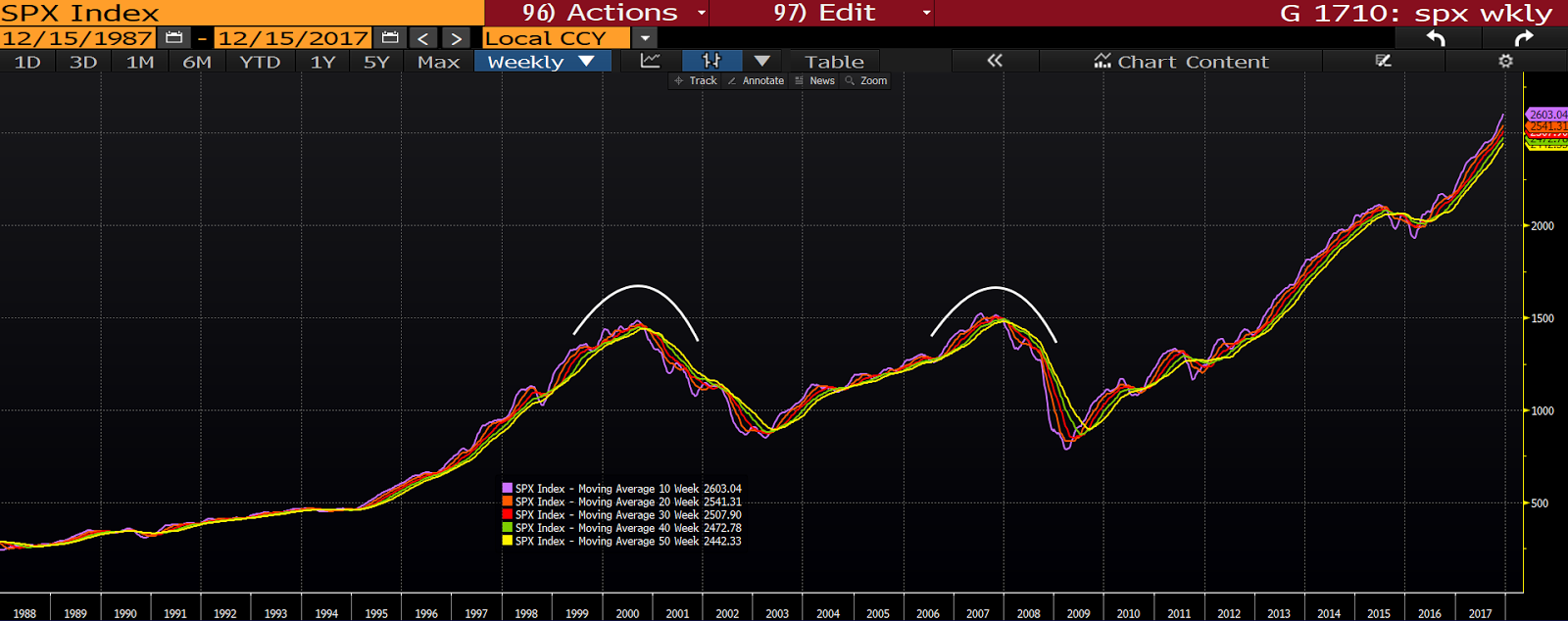

Take a look at this weekly chart of the S&P 500 Index spanning the past 30 years: click any insert below to enlarge…

Now let’s do a little technical work.

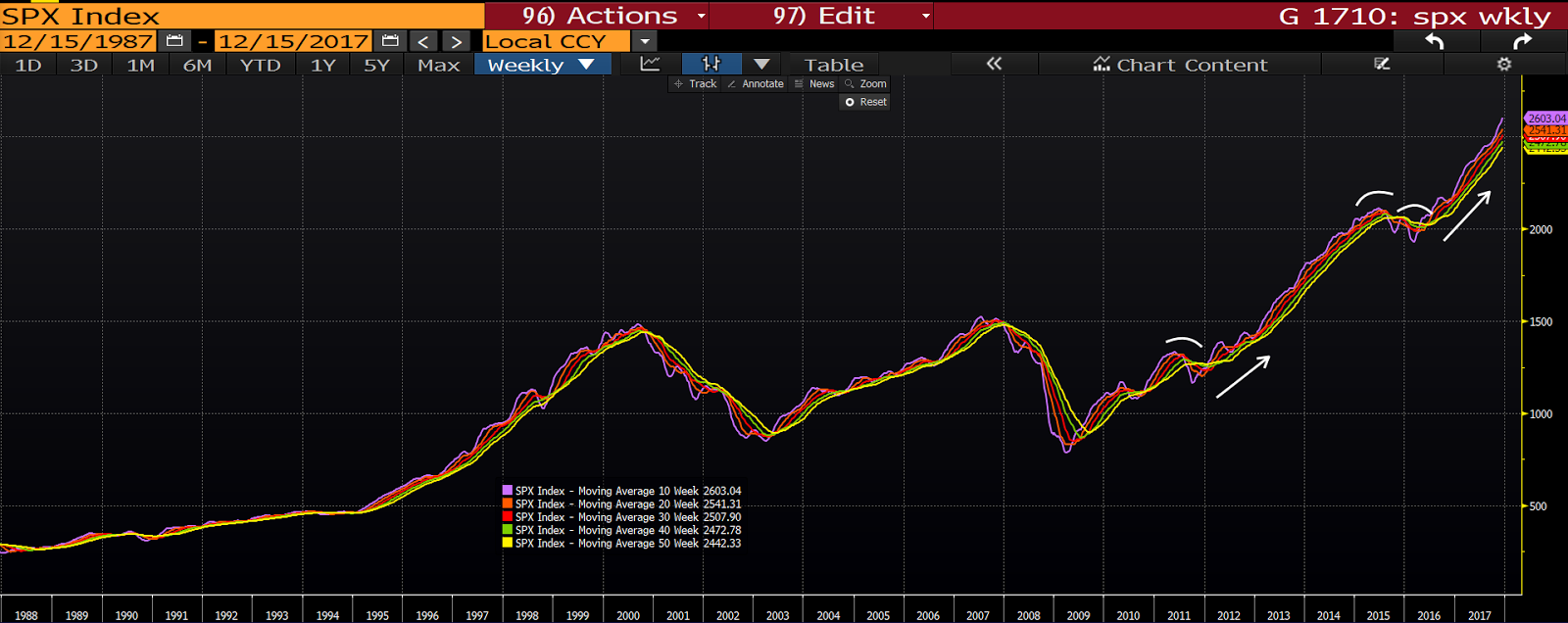

Here’s the same chart with the 10, 20, 30, 40 and 50-week moving averages added:

A look at a given index or security’s moving averages offers the analyst a picture of the prevailing sentiment in the aggregate of all market participants. The most bullish scenario exists when the fastest (shortest-term) moving average is on top, with the slower (longer-term) falling below in sequence — while all are curving upward. A bearish scenario is the reverse, with the slower moving averages atop the faster — while all curve downward.

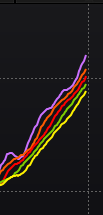

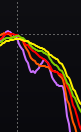

Here again is the 30-year weekly chart, this time with price removed. Notice the rolling over and the reversal of positioning of the moving averages as the stock market moved into two of history’s worst bear markets:

in essence, when the moving averages look like this —

(today, in fact) — probabilities favor stock market gains going forward.

When they look like this —

— look out below!

So there you have it: Easy peasy! Just track a series of moving averages and stay aggressive when the faster are on top and all are positively sloped. And get defensive when the slower are on top and the slope’s negative.

Well, not so fast! What about those times when it appeared as though a rollover was eminent, but then, out of the blue, the market turned higher and the bullish setup resumed:

The 10+% corrections of 2011

, 2015 and 2016

, 2015 and 2016  were painting technical pictures that screamed get defensive. But, alas, those who did no doubt found themselves dumbfounded as the market turned back around just after they repositioned to a more defensive posture. Imagine the emotional struggle as these folks pondered if and/or when to adjust their weightings back to the growthy allocation that their then recently-failed indicators demanded.

were painting technical pictures that screamed get defensive. But, alas, those who did no doubt found themselves dumbfounded as the market turned back around just after they repositioned to a more defensive posture. Imagine the emotional struggle as these folks pondered if and/or when to adjust their weightings back to the growthy allocation that their then recently-failed indicators demanded.So what’s an investor to do? I mean, clearly, the technicals work much of the time, but my how unfortunate the results when they don’t!

This is where macro fundamental analysis comes in.

Here’s the moving average only chart along with our macro model scores back when things were getting dicey. In the two ultimately bear market instances we featured the scores before the moving averages actually rolled over (i.e., when the technicals were still relatively positive). In the two false signal (for long-term investors) instances we ran the backtests at virtually the worst possible times (when the market seemed on the verge of falling apart):

Now you know why our view of general conditions holds sway over the technicals. Even before the market rolled over — ahead of the respective burstings of the tech and real estate/mortgage bubbles — our macro analysis was pointing to a high probability of rough times ahead. While in the midst of three double-digit corrections — that were simply pauses in an ongoing uptrend (or, as a technician would say, “countertrend moves”) — our macro model remained on balance bullish.

Has PWA thus discovered the Holy Grail of asset allocation? Well, absolutely, unequivocally and emphatically NO! Folks — make no mistake — when it comes to financial markets there is no Holy Grail! Anything can happen! Recall from Part 1; “good investments that lose money.” The best we can do is use the tools at our disposal to assess present conditions and act accordingly.

To borrow from a Jesse Livermore quote also featured in Part 1:

“…all a man needs to know to make money is to appraise conditions.

In essence, our investment decisions reflect go-forward probabilities (never certainties) based on the weight of the evidence (never on whims, hunches or nerves). All the while we remain flexible and keep our minds open to all possibilities.

Oh, and by the way, our macro score presently sits at a very bullish +60, with 85% of the data reading positive, 3% negative and 12% neutral. Which explains our presently growthy sector allocation within client portfolios.

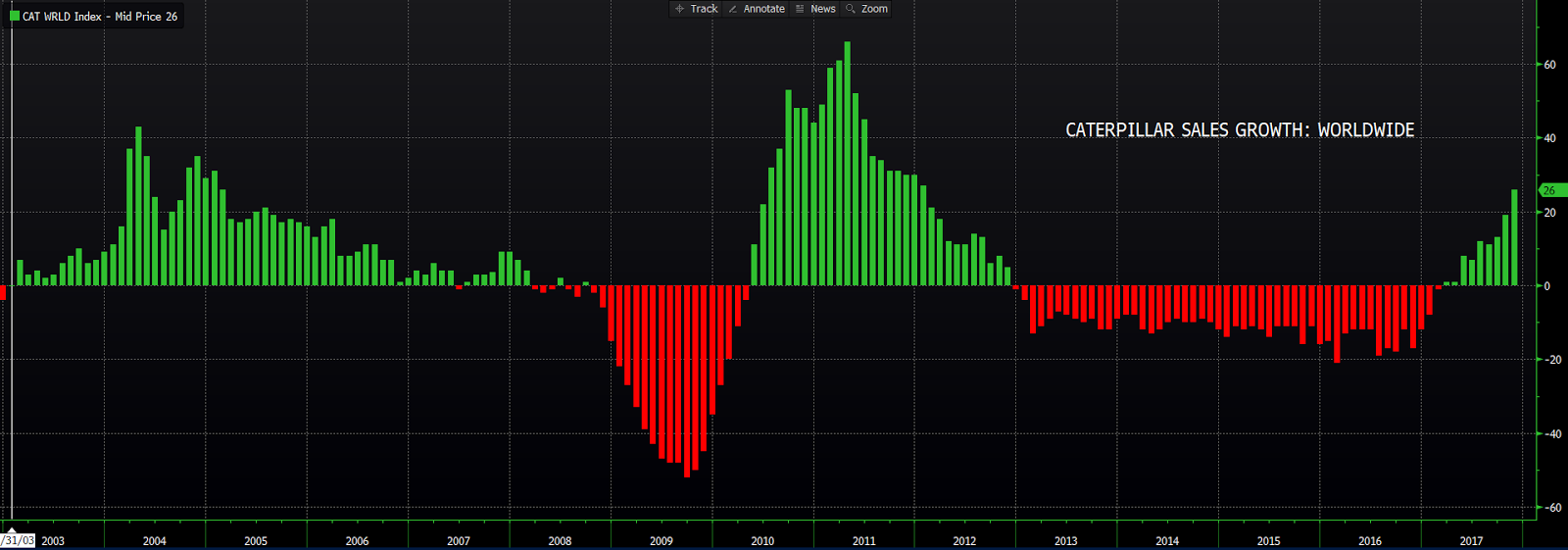

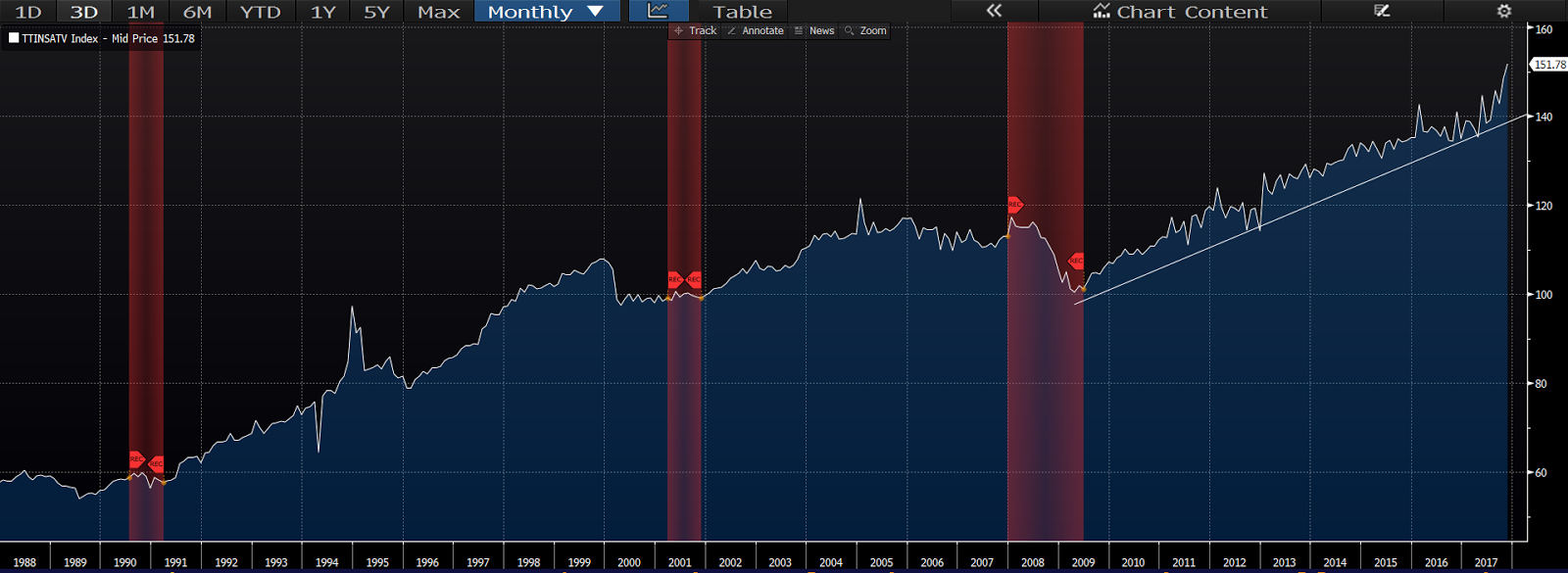

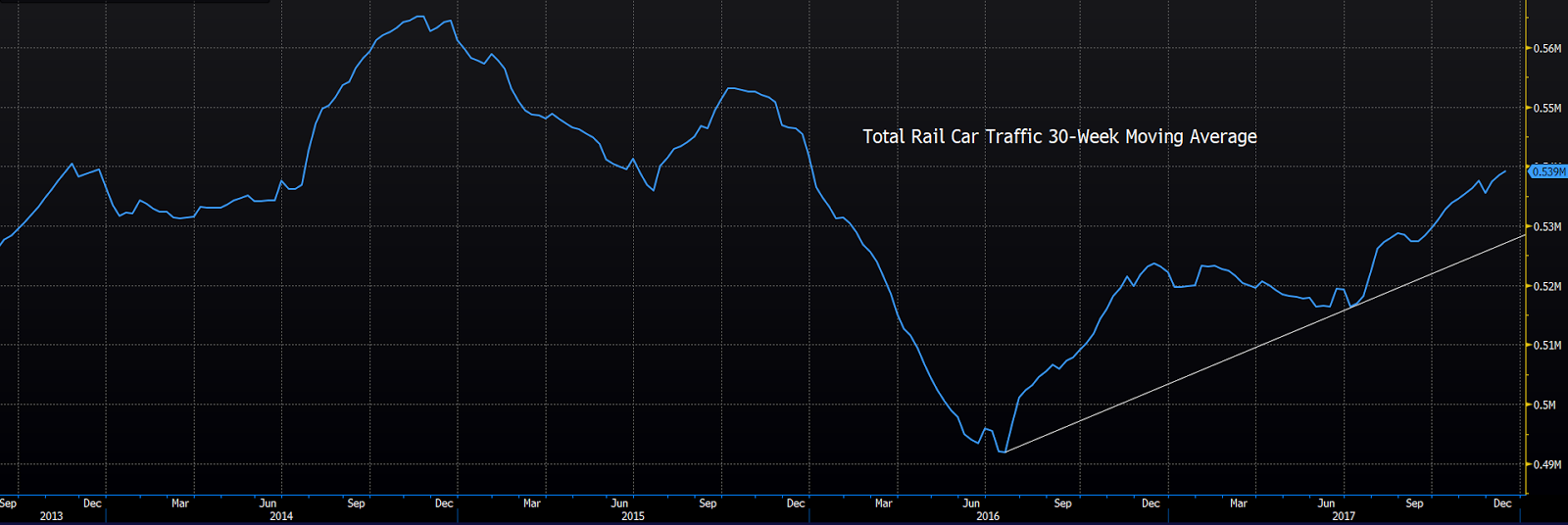

Areas that improved notably (moving from negative to positive) during the year ironically reflect global macro conditions; such as the Merrill Lynch Global Financial Stress Index, Caterpillar global sales, and the trend in copper pricing. The VIX curve (a measure of volatility) also went from negative to positive. The areas that moved from neutral to positive are non-farm payrolls, truck tonnage, railcar traffic, the TED spread (a financial stress indicator), the emerging markets economic surprise index, the Baltic Dry Index (tracks ocean shipping costs for dry bulk materials throughout the world), the CBOE put/call ratio (sentiment) and two U.S. stock market breadth indicators. There are only two areas that show deterioration versus the start of the year; small business capex (expansion) plans and NYSE short interest (sentiment) went from positive to neutral.

Part 3, Sectors

Here they were, along with the year-to-date results (through 12/22) for each:

Financials: Target 20%, YTD Return +20.1%

S&P 500: +19.70%

Now, before you do the math (assuming you haven’t already), and realize that the above target percentages add up to 103%, you should know that those are base targets. We allow for a 2% move above or below those numbers. I.e., a given client’s allocation will only flash a warning signal if, for example, their financial sector weighting (20% on January 1) moved above 22% or below 18%. Also, we tend to push a given sector above or below our target (within the allowed range) depending upon our view of its present prospects. For example, presently we’re allocating financials to the higher end of our current range (today that would be between 18% and 20%) and technology to the lower end (10% to 12% today).

By and large — save for their energy exposure (which we adjusted during the year) — our client portfolios took advantage of the opportunities that presented themselves throughout 2017.

Adjustments we made during the year were as follows:

Reduced financials to 18% early in the year.

Here’s a brief sector-by-sector synopsis of what we view as today’s key fundamental considerations. We want to emphasize “brief”, as we could easily offer up a lengthy research paper for each.

Note, the following relates primarily to the prospects for sectors within the U.S. economy. Our targets are also influenced by our assessment of each sector within other countries — as we maintain target allocations to foreign markets as well. A topic we’ll tackle in Part 4.

Financials:

The financial sector stands to benefit from a number of potential developments in 2018, including the following:

1. Prospects for higher long-term interest rates amid a growing economy: Banks borrow on the short end of the yield curve and lend on the long (higher lending rates [relative to their cost of money] increase their net interest margin — an important earnings component).

2. Prospects for deregulation: The President has made it clear that deregulation will be a hallmark of his term in office, plus, the incoming Fed Chairman has stated his intent to loosen financial regs.

3. Tax Reform: It’s estimated that the 21% corporate tax rate will boost bank earnings by 11.1%.

4. Valuation: On a price to forward earnings basis, financials are second cheapest (to telecom) among the major sectors.

5. Trading volume: 2017 is about to go down as one of the least volatile years in market history. Thus, an important revenue source — securities trading — for major financial firms faced a real headwind for much of the year, as volatility equates to trading activity. While, as discussed in Part 2, we like the macro setup going forward, we believe that the likelihood of a repeat of 2017 (in terms of volatility [lack thereof]) is very low indeed. Thus, the prospects are decent for a pickup in trade-related revenue for the big banks going forward.

As suggested above, we are indeed presently bullish on financials. For now we’re maintaining our base target of 18% of equities exposure (our presently largest weighting) — with a bias to the upper end of our range (i.e., 18-20%)

Technology:

While we remain constructive on tech given the global macroeconomic setup and the current pace of innovation in both products and services, we’d be surprised to see the sector maintain its lead (relative to other sectors) during 2018, for the following reasons:

1. Foreign-denominated revenue: U.S. tech companies, as a group, earn the majority of their revenue outside the U.S.. Therefore, should the prospects for economic growth and higher interest rates in the U.S. result in a stronger dollar going forward, foreign denominated earnings will take a hit when translated in U.S. dollar terms.

2. In a rising dollar environment, U.S. goods are more expensive to foreign buyers. However, we don’t (at this juncture) see this as being a major impediment to international technology sales (plus, a higher dollar is beneficial when we consider foreign-made inputs/components as well as foreign labor). That said, the trading community can be very sensitive to dollar-related dynamics, and we believe it may be especially so heading into 2018.

3. Given the sector’s outsized returns in 2017, we think that it’ll take outsized hits (relative to other sectors) when volatility visits the market, and profits are taken, in 2018.

5. Threat of U.S. protectionism: Tech underperformed other cyclical sectors measurably between last year’s election and the beginning of this year. Our view is that — along with the at-the-time appreciating dollar — the poor relative results stemmed largely from traders reacting to the prospects for a negative impact on the most internationally-centric U.S. companies, should rhetoric become reality. After the inauguration, however, it appeared as though the more aggressive of the Trump campaign’s protectionist propositions would not come to fruition, which remains the case for now. Any new trade barriers erected at this juncture could prove to be significantly negative for the sector, in our view.

Again, we’re not bearish on the tech sector (in fact, we believe there are some very compelling individual stories), we’re simply assessing its prospects for 2018 relative to other opportunities, and for now believe them to be a bit less compelling compared to a year ago.

Industrials

The industrial sector, at 18% of equities, currently ties with financials as our top target weighting heading into 2018. Bottom line: The world is building and America is spending (and taking delivery).

Here’s some proof:

Caterpillar’s global equipment sales are on the rise for the first time in years:

Our truck tonnage chart is showing notable acceleration of late:

As is our chart of total rail car traffic:

Here are some key themes we see impacting the industrial sector going forward:

1. Infrastructure Spending: While much of the world is already heavily engaged in infrastructure investment, the U.S. looks to be just beginning. We were touting these prospects months before last year’s election (when the ultimate outcome was not something we were anticipating), as the Democrats were pounding the table every bit as hard as, if not harder than, the Republicans on the need for infrastructure investment in the U.S.. Thus, passing an aggressive infrastructure spending package will likely be a relatively easy win for the Administration in 2018. Although, not everyone agrees…

2. Transportation: Per the charts above, goods (as are people) are moving across the roads and railways (not to mention airways) of America. Of course this is consistent with our macro model’s presently high score, and, thus, speaks to the present strength of the economy. Transportation companies (ground, rail and air) are well represented in our core industrials ETF.

3. Defense Spending: The U.S.’s major defense contractors occupy prominent positions in the top 20 holdings of our core industrial sector index ETF. These multinational companies stand to gain from defense spending in other nations as well.

4. Tax Reform: U.S industrial companies stand to be major beneficiaries of the drop in the corporate tax rate; with an estimated 16.7% boost to earnings.

5. The U.S. Dollar: A strengthening U.S. economy, higher interest rates and a less accommodative Fed could result in a higher trending U.S. dollar in 2018. Given that there’s a real multinational flavor to many of the companies that comprise the industrial sector, a rising dollar poses a potential headwind. At this juncture, however, we believe that the positives stand to overcome this potential negative, despite what we expect will be a heightened sensitivity to a rising dollar among traders.

6. Protectionism: Now, combine a potentially higher trending dollar with higher barriers to international trade (which has, thus far — notable exception(s) aside — been more rhetoric than realty) and we’ll have a combination that could ultimately put our bullish thesis to the test.

Materials

The basic materials sector, with a 15% of equities target, is uniquely positioned to prosper given the present global economic setup.

Here are some key themes we see impacting the materials sector going forward:

1. Infrastructure spending: See #1 under industrials. Of course all of that construction will require tons upon tons of virtually every industrial material known to man.

2. Inflation: While inflation has been virtually non-existent in the current recovery, our view of the labor market, of commodity trends, of reports from the manufacturing sector, and of the increasing pace of factory capacity utilization, is that its acceleration is virtually at hand. Inflation running a bit above the Fed’s 2% target should not be viewed, at this stage, as problematic, but rather as a driver of increased revenue for the materials sector — as well as being indicative of an economy that is healthily moving into the later-mid stages of expansion. Higher-trending materials prices, amid a pickup in capex spending (investment in productivity-enhancing expansion), suggests that much of that increased revenue would flow straight to the industry’s bottom line. Additionally, such gains in productivity, while making for more profitable companies, may also keep inflation from becoming problematically high in the foreseeable future.

3. Lithium miners: Lithium is an essential element in the batteries that power the mind-boggling technology — from smart phones to self-driving electric cars — of today and tomorrow. Our core materials sector ETF features two of the world’s premier lithium miners in its top 20 holdings.

4. The U.S. Dollar: Given the commodity-centric nature of a number of names within our materials ETF, a rising dollar could pose a headwind. In addition, there is sufficient foreign revenue exposure within the group to make a rising dollar potentially problematic. However, as with industrials, we think the presently positive setup for the materials sector stands to effectively mitigate the potential negative effects heading into 2018. That said, as we stated in our summary of the tech sector, we do anticipate a heightened sensitivity to dollar dynamics among traders, it’s just that we believe that sensitivity will be expressed more among the tech names versus other sectors.

5. Tax reform: Materials companies are expected to see a 9.4% boost to earnings as a result of the coming cut in the corporate tax rate.

6. Protectionism: Ditto #6 under industrials.

Energy

The energy sector, with an 8% of equities target, while showing renewed signs of strength of late, has its challenges.

Here are some key themes we see impacting the energy sector going forward:

1. High demand: Energy products will remain high in demand in an expanding global economy.

2. OPEC: OPEC, along with Russia, have agreed to keep 1.8 million barrels of oil per day off the market through the end of 2018. Which has indeed helped out the price of late. However, OPEC’s nemesis, North America, will continue to exploit its efforts to the fullest. I.e., as OPEC cuts (and supports the price) North America ramps up production, effectively quelling the desired rise in price.

3. Profitability: Amid strong demand, and OPEC’s efforts, a price per barrel back below $40 is highly unlikely in 2018. However, at a price much below $50, we should see any expansion in North American shale production slow measurably, as we’ve seen estimates of the break-even price for shale producers of between $40 and $55 per barrel. The share price action of the companies that comprise our core energy ETF are of course highly correlated to the fluctuating price of oil. However, if prices can remain stable above $50, the renewed strength we mentioned above can persist, and it’ll show up in company earnings.

4. Renewables: While the world will continue to consume fossil fuels into the future, anyone who would deny the fact that the industry faces major challenges, as the world pushes to clean itself up, is, well, in denial. Thus, while we’ll indeed see geopolitical, etc.-induced spikes in the price of a barrel from time to time well into the future, the longer-term trend will indeed be a lessening of dependence on fossil fuels and, thus, a massive structural rebalancing that, again, poses major challenges for the industry in the years to come.

5. Tax reform: Energy companies — with a whopping 25.9% boost to earnings — are estimated to be the chief beneficiaries of the corporate tax rate cut. This helps for sure!

6. The dollar: Oil is still traded primarily in U.S. dollars throughout the world. Thus, the price of a barrel is indeed influenced by fluctuations in the U.S. currency. A rising dollar in 2018 can, therefore, become a notable headwind.

Consumer Discretionary

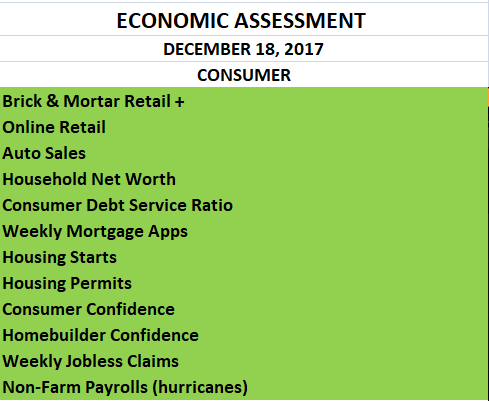

Ironically — thanks to the recent success of brick and mortar retail — for the first time all year the consumer-driven inputs to our macro model are all colored green. Here’s that section from our last update:

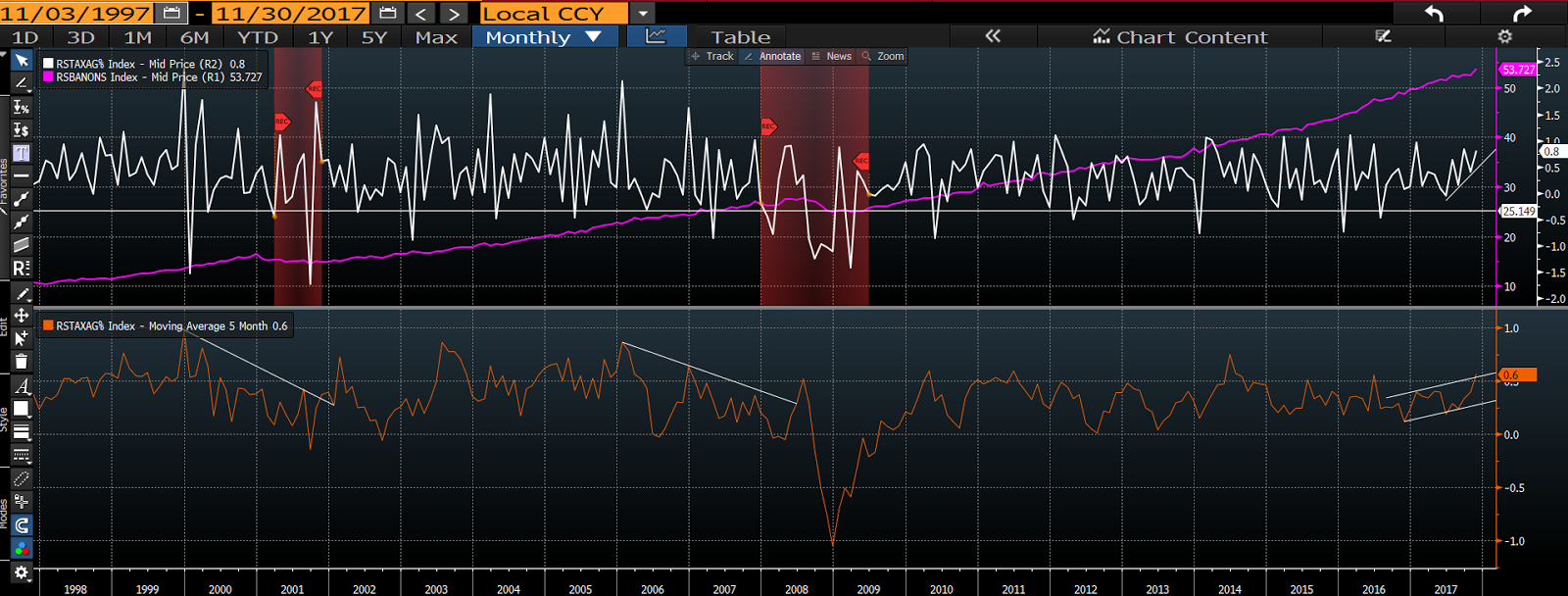

Here’s a look at our retail sales chart (white line is the monthly brick and mortar number, the purple line is online retail, red shaded areas are recessions. The orange line in the lower panel is brick and mortar sales’ 5-month moving average): click to enlarge

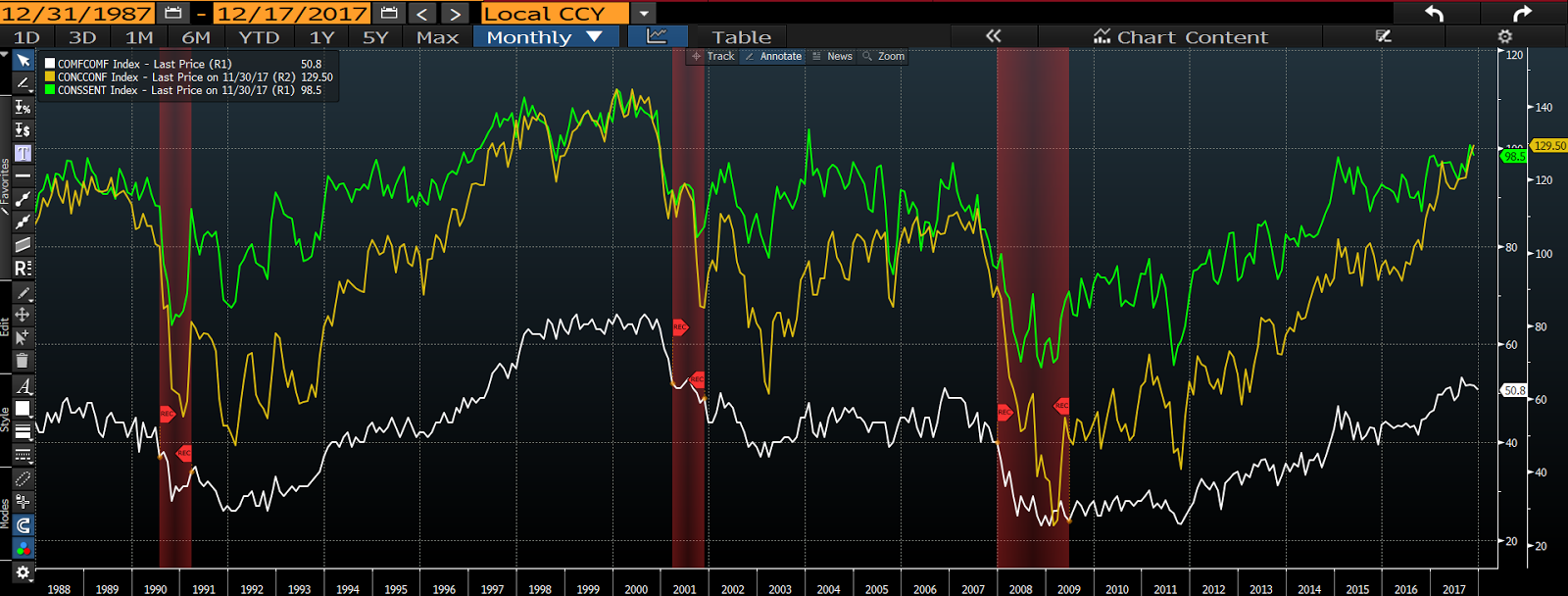

And here’s the latest in consumer sentiment (green and yellow lines are monthly survey results from the University of Michigan and The Conference Board respectively. The white line is Bloomberg’s weekly consumer comfort index. Red areas are past recessions): click to enlarge

I.e., we’re feeling good enough about our base 10% target to the consumer discretionary sector to push it toward the upper limit (12%) in most client portfolios. Our only hesitation — and a slight one at that — is valuation; at 20.4 times next years estimated earnings the sector sits as our third most expensive, behind REITs and energy.

In case you’re wondering why we’re only slightly hesitant regarding a sector that trades above 20 times estimated earnings during the second longest bull market in history, well, as we illustrated back in June, price to earnings ratios are terrible market timing indicators.

Healthcare

The healthcare sector, at 8% of equities, remains a relative underweight in client portfolios. Essentially, while the sector offers much by way of diversity (pharmaceuticals, equipment, hospital and insurers), broadly-speaking we consider it an economically defensive play. While we think there’s enough going on in the space to merit a high single-digit weighting, we feel that other more cyclical sectors offer better opportunities for the time being.

Here are some key fundamental drivers:

1. Age: An aging population requires ever increasing medical attention.

2. Longevity: Folks are living longer, even with chronic disease.

3. Sedentary lifestyles and poor eating habits: Obesity and diabetes are on the rise.

4. Technology: As in other sectors, technological advances in medicine are occurring at a rapid pace. The companies at the forefront make interesting investment prospects.

5. Government: The more government intervenes into the healthcare space the greater the chasm separating the winners and losers. Think in terms of hospitals and insurance companies; the greater the number of folks who are covered the better off the service providers (of course reimbursement rates come into play), yet the more the utilization the higher the claims on insurers.

The utilities sector is considered your quintessential defensive play. It also sports some of the market’s highest dividend payers. The following explains why we remain bearish (0% target) on the sector.

Key themes:

1. Economically defensive: Utilities are known for their defensive nature. I.e., folks gotta keep the lights, the air and the heat on. When the economy is in expansion mode, clearly, the cyclical sectors house the more compelling opportunities.

2. Interest rate sensitivity: Investors tend to buy utility stocks for their high dividend payouts. When interest rates rise, the sector faces stiff competition from the debt markets. I.e., while the utilities sector in the aggregate is paying a 3.34% dividend, yield-hungry, risk-averse investors will have zero qualms about exiting the space when treasuries yields are comparable. In addition, utility stocks tend to carry a great deal of debt on their balance sheets. Higher interest rates lead to hiring borrow costs, thus crimping their bottom lines.

3. Renewable energy: By some estimates, “by the year 2050, renewable energy could source approximately 80% of the world’s energy.” Thus threatening the future of traditional utility companies.

Telecom Services

That said, telecom is actually the one sector that we’ve allowed to move above the top end of its target range (0-2%) without stepping in to rotate out. For one, the two top positions in our core telecom ETF, AT&T and Verizon, happen to be the 6th and 10th largest holdings respectively in our core technology ETF. Plus, telecom is a key component within our emerging markets exposure, which is one place the sector performed quite well in 2017.

After an abysmal year for U.S. telecoms, their relative cheapness and a somewhat improving technical picture presently has our attention. I.e., we may find ourselves upping our allocation in the not too distant future.

Consumer staples

REITS

While in the past we’ve maintained as high as a 10% target weighting to REITS, for now we remain at zero; for the simple reason that they, as a group, have been the definition of interest rate sensitivity. The quarterly correlation coefficient between REITS and the 10-yr treasury yield over the past 5 years has been -0.613. Over the past 12 months it’s been -0.93. Meaning, when interest rates rise, REITS tend to fall in value (big time lately) — and we believe that the risk to interest rates going forward is to the upside.

Once again:

….while good investments can, and often do, lose money, if we take only shots where the setup makes good sense — i.e., if we take only good shots — and we take them from multiple angles and distances (diversify), we believe that we give our clients the absolute best odds of achieving long-term investment success.

In mid 2016 we produced the following video on global investing. We believe it remains timely, instructive, and clearly illustrates the opportunities that abound beyond our borders. It essentially foretold the out-performance we’ve experienced of late from our non-US exposure.

Please take a few minutes and watch. As you’ll gather from the video, and as you’ll see in the updated charts below, the longer-term prospects for global investing remain quite compelling.

Click the wheel to the left of “YouTube” to improve the clarity…

Now, bringing the charts forward:

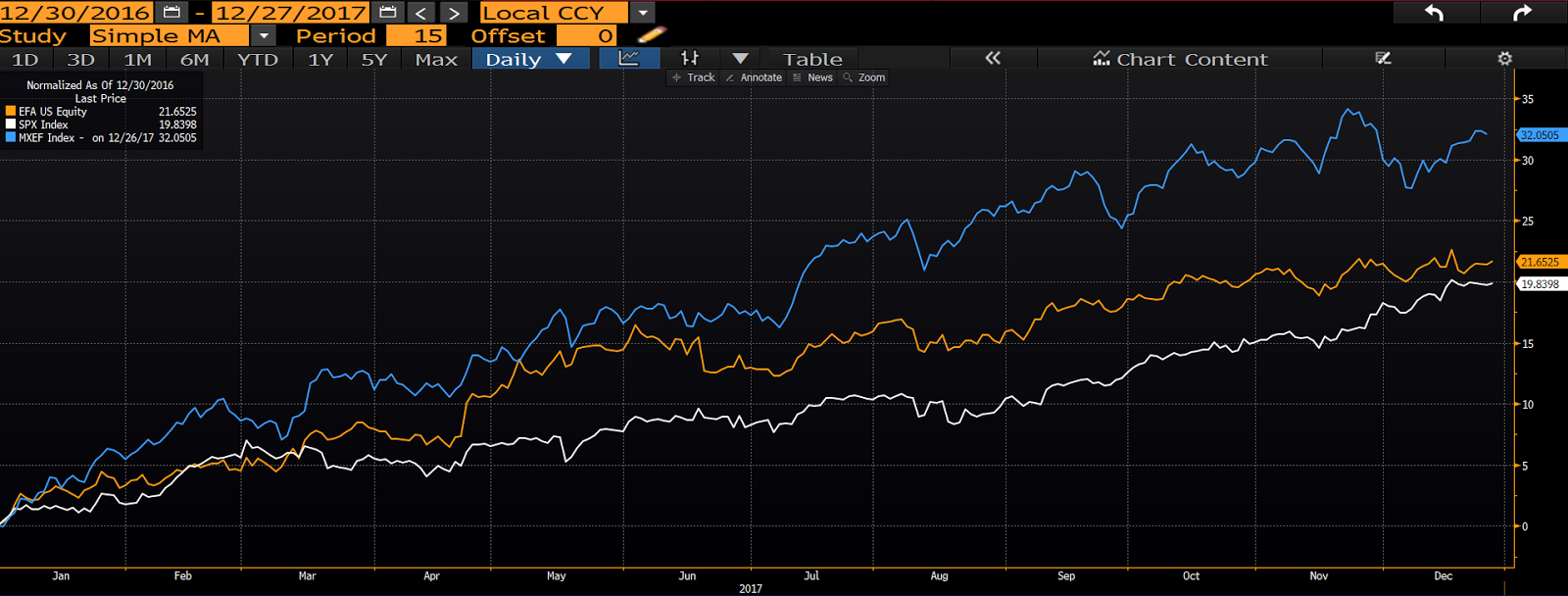

Here’s a look at the performance of the U.S. S&P 500 Index (white line), developed non-US markets (yellow) and emerging markets (blue) in 2017. As you can see, after a long period of under-performance, non U.S. equities were, in the aggregate, the best places to be this year:

Click any chart below to enlarge…

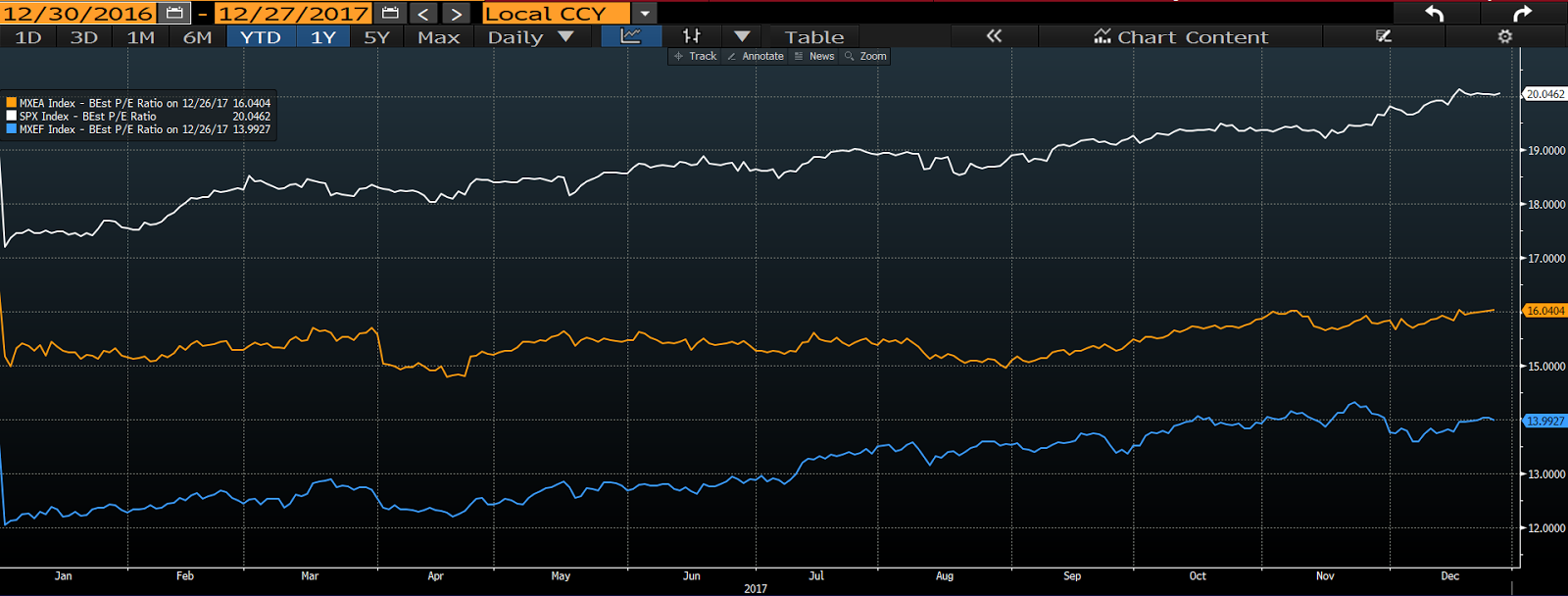

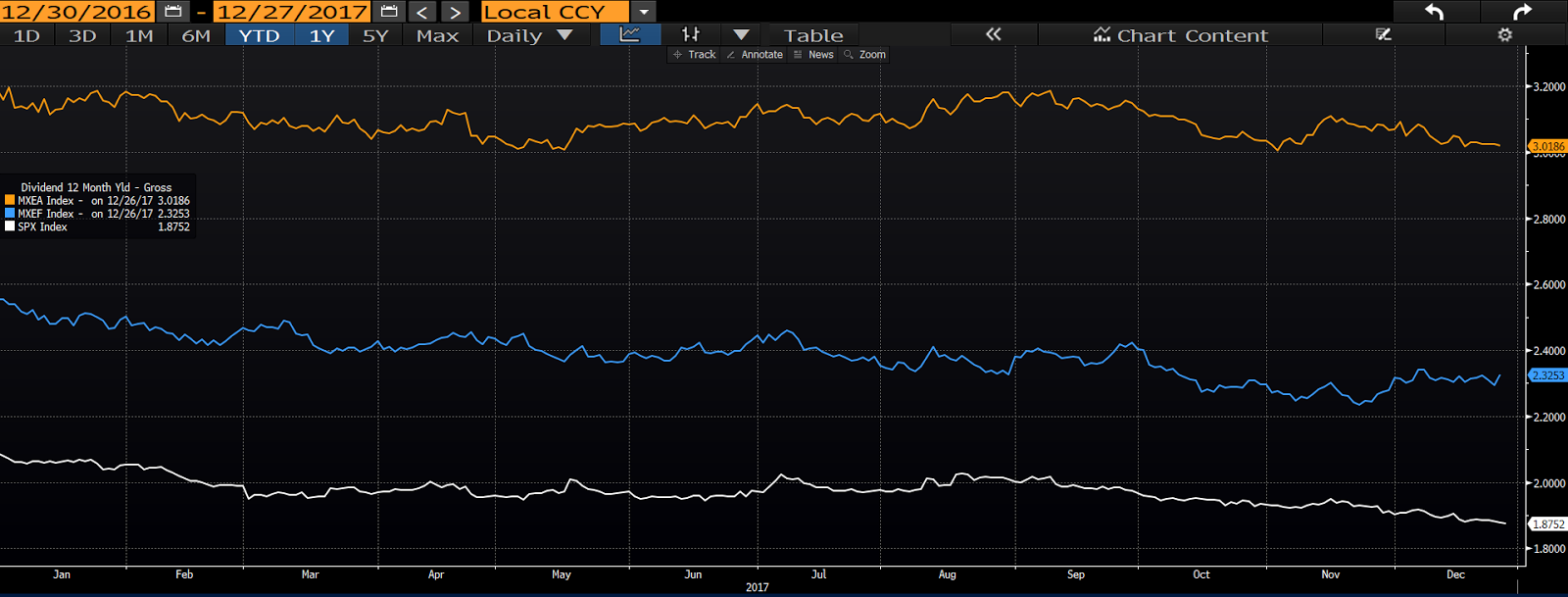

In terms of valuations, non-US markets remain notably cheaper (from a price to earnings standpoint) than the U.S.:

And foreign stocks continue to pay notably higher dividends:

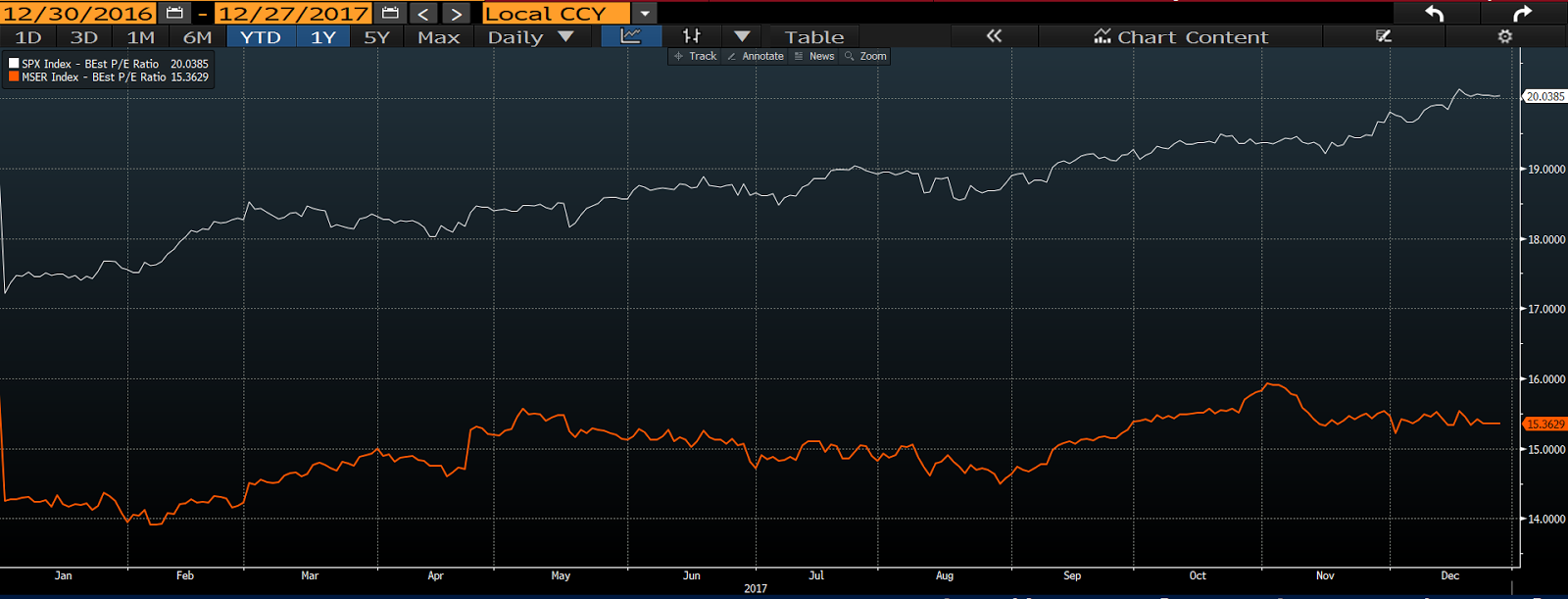

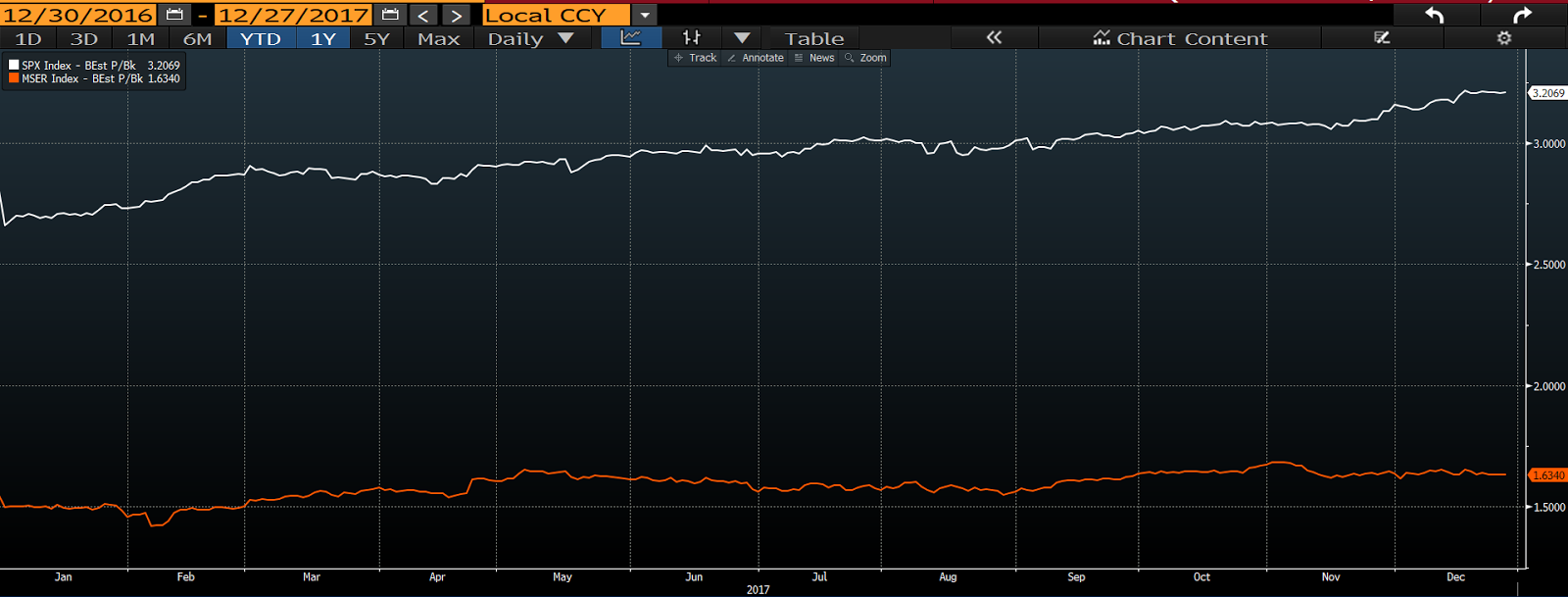

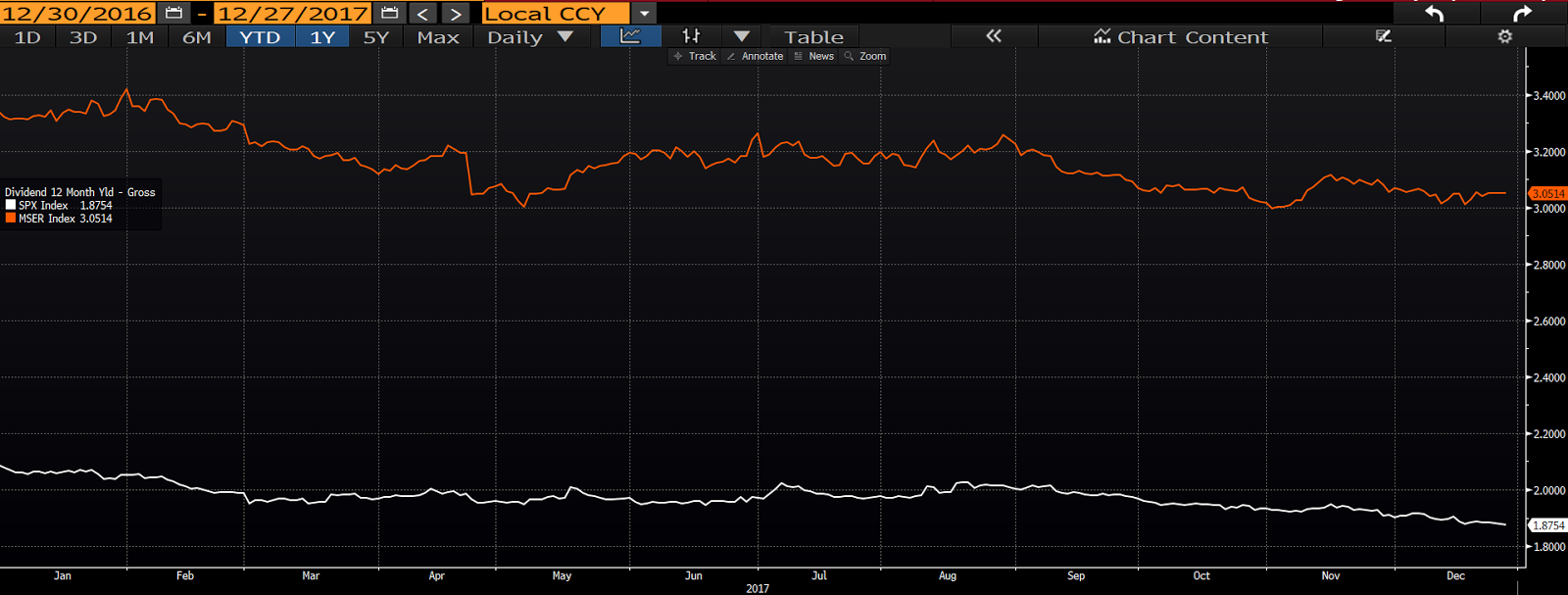

Zeroing in on the Eurozone versus the U.S.:

Eurozone stocks remain cheaper on a price to earnings basis:

Also on a price to book basis:

And from a dividend yield standpoint as well:

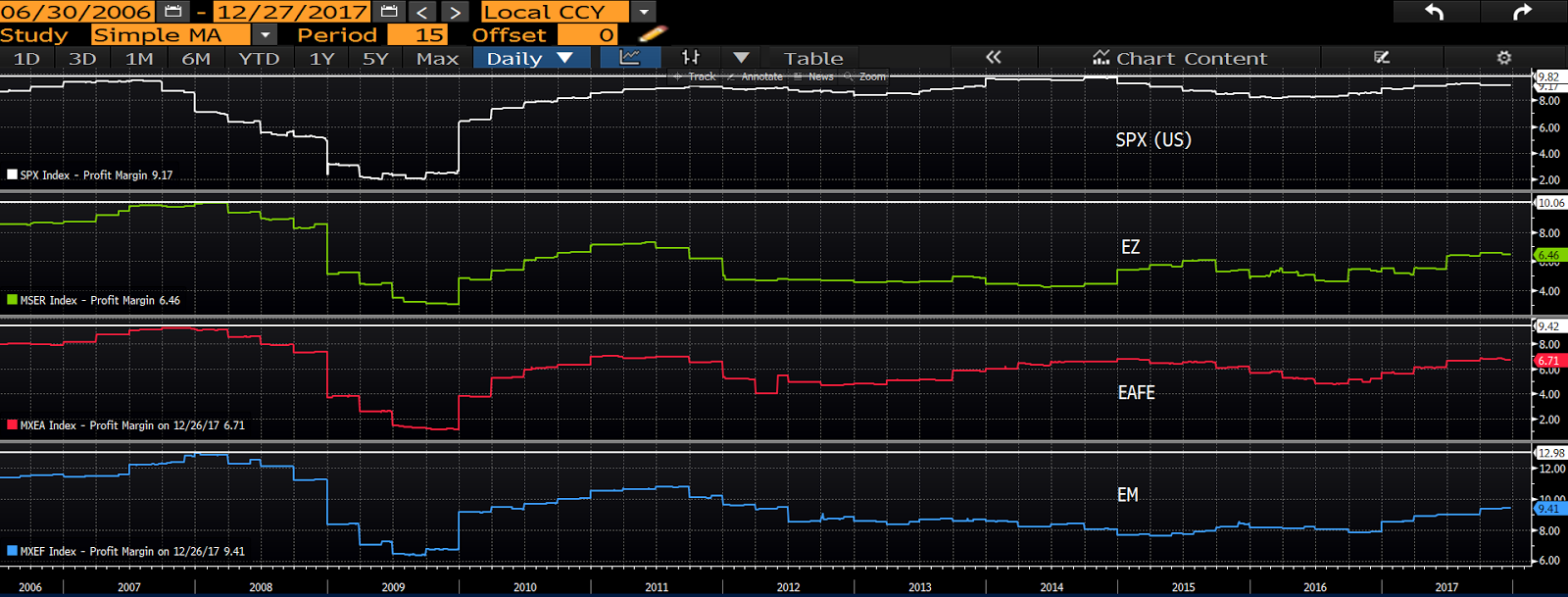

In terms of profit margins globally; the U.S. is still flirting with record margins, as the rest of the world, while now seeing margin growth, still has a ways to go:

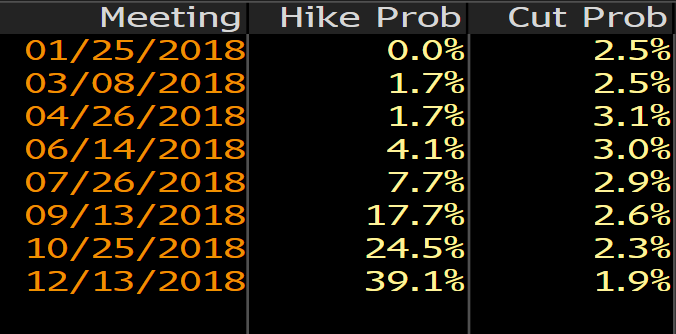

Lastly, the one dynamic that has markedly changed is that after a strong rebound in economic activity the European Central Bank is no longer in aggressive easing mode. In fact, the futures market is now pricing in ECB rate hikes later next year:

Now, all that said, foreign investing involves additional risks that can turn the most compelling long-term thesis into the most palpable short-term turmoil; geopolitical risk being the most obvious.

The other major dynamic occurs within the currency markets. 2017’s declining dollar provided a major boost to our non-US holdings during the year (as foreign denominated profits translated to greater U.S. dollar earnings). Should the dollar reverse and move higher — amid higher U.S. interest rates and an accelerating U.S. economy — it will indeed become a headwind, despite the fact that a stronger dollar will make foreign-made goods cheaper for U.S. consumers (a potential offset to the currency translation risk).

Bottom line: While we’re not quite as near-term bullish on Non-US vs US as we were at the start of 2017, the weight of the evidence keeps us firmly committed to our present base targets.

Part 5: The Dollar, Bonds, Gold and Silver

The Dollar

Several times in this year’s lengthy final message we’ve cited the potential for a rising U.S. dollar to be a headwind for a number of sectors, as well as foreign equities, in the year to come.

Our view is that a relatively strong U.S. economy, aided by the potential near-term positives of corporate tax reform, not to mention an infrastructure spending package (should it happen), along with a higher interest rate regime, and a Fed that is no longer reinvesting all of the income from its massive balance sheet, are factors that stand to support the dollar — if not see it rising — going forward.

Interestingly, however, currency experts seem to disagree. Bloomberg’s December 26th article Picking FX Winners for 2018 captures the sentiment:

Following the dollar’s worst year in more than a decade, foreign-exchange strategists see few signs of optimism for the U.S. currency in 2018.

Funny thing is, at the beginning of 2017, the prevailing sentiment among the currency crowd was one of optimism. They felt that the rally in the dollar that began with the presidential election would carry into 2017 on the back of tax reform, infrastructure spending, deregulation, an improving economy and higher U.S. interest rates. Which actually pretty well describes today’s setup; and now they’re bearish! Hmm…..

(My “Hmm” aside, conventional valuation metrics indeed show the dollar overvalued relative to most foreign currencies (supporting the present consensus). It’s just that, as in the stock market, valuations are virtually never, by themselves, good timing indicators. It’s more about overall conditions)

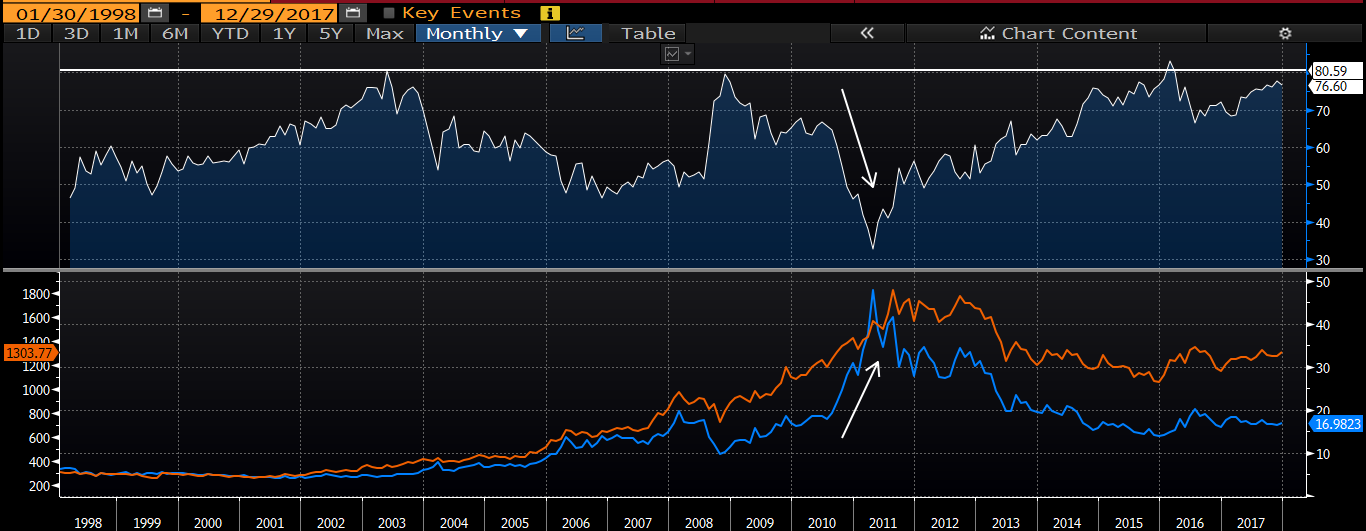

Here’s a 5-year chart (ending 12/31/16) of the net positioning among asset managers who trade futures contracts on the U.S. dollar index: click any chart below to enlarge

Per the chart, futures speculators were long the dollar to nearly the highest degree they’d been in 5 years, heading into 2017.

We actually were not in that camp. While we did not foresee a huge decline in the dollar in 2017, our view was that the Euro, in particular, was poised to do better on what we saw as the potential for a strong rebound in the Eurozone economy. I.e., while it was obvious that U.S. interest rates would trend higher in 2017 versus the Eurozone (conventional thought says traders migrate toward the currency with the highest yield), we expected that money would actually flow to Europe (as well as to the emerging markets) — creating a headwind for the dollar — based on opportunities in its asset markets.

And here’s how the dollar actually performed in 2017:

Here’s how the Euro fared:

Here’s from a May 2017 blog post where we highlighted some confirmation that we were on the right track (although we don’t want to overstate our position: Again, we did not see the big decline in the dollar coming, we simply anticipated events that kept us out of the bull camp coming into the year):

As I’ve been charting here on the blog, while the setup for U.S. stocks looked good coming into the year (still does), the setup for the Euro Zone looked every bit as good, if not better (still does). While stocks and economies don’t — particularly in the short-run — always correlate, the relative (to the U.S.) data coming from the Euro Zone of late support the setup, as well as explain the currency action.

Now, let’s not get ahead of ourselves, currency markets are no easier to predict than are equity markets, so we’re more than willing to concede that maybe this time the currency crowd has it (the dollar will decline throughout 2018) spot on, and that we (the risk is to the upside) don’t. The good news is that if they’re right (and we’re wrong), our clients stand to win. As those headwinds from a higher dollar that we cited in earlier parts of this letter won’t develop after all!

Bonds:

For our purposes here our focus will be on treasuries as a proxy for high quality debt securities. The factors that impact lower quality, high yield (junk) bonds have vastly different implications versus high quality bonds. Plus, generally speaking, the fixed income market is where we look to house the portion of client portfolios where safety (shelter from volatility) is our top priority. We generally look for growth (and volatility) from the equity markets.

We can keep our commentary on bonds short and sweet for now (of course we’ll be providing updates throughout the year):

Folks typically buy bonds for their safety and their income. The latter makes them very susceptible to interest rate fluctuations. For example, say you recently bought a 10-year treasury bond with a yield of 2.4%. Now you’re not at all stuck with that bond for the next decade, you can sell it anytime you like in the secondary market. Thing, is, if interest rates on newly issued 10-year treasury bonds rise to, say, 3% (maybe as folks demand a higher yield to compensate for what they might have earned elsewhere [as the economy improves], or because Congress passes a trillion dollar infrastructure plan and, therefore, the treasury has to attract investors to the greater amount of debt they’ll have to issue to fund it, and so on), who’s going to buy your 2.4% bond? Well, believe it or not, somebody will, but they won’t pay you nearly what you paid for it. I.e., you’ll lose money!

Now, someone — maybe the broker who sold you the 10-yr treasury — might tell you that “you have no risk; all you have to do is keep the bond for the duration.” Well, okay, but imagine all of the income you’ll miss out on if rates stay notably above the 2.4% (an historically low yield) you originally bargained for!

Bottom line: Given all that we’ve stated in this year’s year-end message about economic prospects going forward, we continue to relegate our clients’ fixed income exposure to cash and short-term CDs. However, those prospects could have us finally wading back into the bond market — as prices tank — in the not too distant future. Albeit gingerly at first.

Gold:

Of all the stuff you and I can invest in, gold has to be the most fascinating. It’s amazing to me that a metal that has such little practical application can amass what, in our view, amounts to a large cult following. The passion in which certain pundits pound the table on gold can be startling. Clearly, for them, it’s about ideology, emotion and ego! For us, it’s about reality.

Now, we can argue all day long about the efficacy of a gold standard, while, in today’s real world we aren’t on one. The fact that many folks — and we won’t say illegitimately — pine for the old days, doesn’t, in our view, justify their rabid bullishness on the metal every time the U.S. budget numbers come out, or when they project the national debt 10-years hence. Not that those aren’t legitimate long-term concerns (I’ve devoted many an essay to the subject: Warning! book plug) — or that gold isn’t the ultimate hedge — it’s just that they’re not near-term concerns. For the time being the world still wants what we got. And as long as that remains the case, the dollar’s in relatively good shape, and while gold will absolutely rise and fall on the dollar’s moves, and on the geopolitical conflicts to come, the economic pressures that would result in massive deflation, or hyper inflation, just aren’t on the horizon as we sit here today.

We could go on and talk about gold as a trade. On how speculators are quick to bid the price higher on the odds of a North Korean missile launch, a presidential scandal finding pay dirt, a jobs number missing its estimate, the Fed not raising interest rates as aggressively as previously thought, or any number of other potential events or mishaps — or how they’ll sell it to the ground on the release of a better than expected jobs number, or the resolution of some frightening geopolitical conflict, but, for now, we’ll move on to silver.

Silver:

If I had a silver dollar for every time a client asked us about silver in 2017, well, I’d be a few silver bucks richer today.

It’s interesting, folks virtually never ask about silver because the global industrial economy is in growth mode and silver is a widely-used industrial commodity. They ask because they put it in the same class as gold (a hedge against the end days) and someone told them that its long-term relationship to gold says that its presently very cheap. I.e, the gold/silver ratio is historically wide and, therefore (in theory), silver is likely to rise — as things tend to revert to the mean.

Always happy to play devil’s advocate, I typically say to those folks, “well, sure, the ratio can get back to historical norm by silver rising in price, but it can also get there by gold falling.”

Taking a look at a 20-year chart of the gold/silver ratio (top panel), one can see where the silver bulls are coming from. In 2011, when the ratio was coming off of a level just above where it currently sits, its subsequent contraction indeed occurred due to a serious silver rally (bottom panel; gold in orange, silver in blue):

But here’s the thing, while silver was spiking higher, gold was also on the rise. If you follow the lines in the bottom panel, you’ll find that, directionally-speaking, gold and silver tend to move together. I.e., the odds that silver can rally hard while gold’s on the decline, are quite slim indeed. Therefore, given today’s general economic state of affairs, we believe probabilities favor that the most likely scenario resulting in a contraction of the gold/silver ratio would be an accelerated decline in the price of gold, as opposed to a rampant rise in silver.

Now, all that said, as sure as I’m sitting here this blog post will find its way onto the computer screen of somebody who has dug much deeper than the simple gold/silver relationship we discussed herein. They will, for example, justifiably slam me for not citing the reported huge mismatch between the demand for silver versus its supply in 2011, which of course, they’ll exclaim, resulted in its rapid run higher. The problem is, they won’t be able to explain what happened as silver crashed back to earth amid the essentially same fundamental supply/demand backdrop. Actually, they will, but their explanations will come wrapped in fascinating conspiracy theories involving manipulation by the banking system.

Regardless of whether or not their claims carry water, you and I have to live in the real world, and, for the moment, real world intermarket relationships say that a bullish scenario for silver needs a bullish scenario for gold. And, recent rally — and geopolitical/fed policy hiccups — notwithstanding, we don’t see an investible scenario for silver (relative to other alternatives) as we head into 2018.

Lastly, if you feel you must own a precious metal to hedge against the next calamity (not saying that’s a horrible idea by the way), I personally would chose silver over gold. Or maybe buy some of each.

Part 6: Conclusion

At last, it’s time to close our year-end message for 2017:

Herein we’ve presented what we believe to be the characteristics of good portfolio managers. We’ve expressed the sense of security we gain in the understanding that while not all good investments make money, if we strive to make only good investments the odds are strongly in our clients’ favor over the long-term. We highlighted the whys and wherefores of the sectors we presently like and those we don’t. We shared our views on the importance of maintaining a global investment mindset. We expounded on why we think that (despite valuation) many currency traders once again may be on the wrong side of the dollar going into 2018 — and how it’s perfectly okay for our portfolios if they’re right this time. And we discussed the not-so-safe nature of today’s bond market as well as our presently not so bullish view of precious metals.

All of that time, effort, analysis and presentation aside, the true beauty of markets lies in their perpetual, and unpredictable, motion. We accept (embrace even) the fact that, while our present positioning is the product of intense technical and fundamental analysis, things will absolutely change over time; some things more rapidly than we may have previously anticipated. And as things change so must our perspectives, and so must our allocations.

Bottom line: At PWA our egos are not invested in our positions; we are indeed forever striving to prove ourselves wrong. It’s not in the least bit important to us that the market continues its bullish march into 2018, as our analysis presently suggests it may (with, by the way, substantially more volatility than we experienced in 2017 [it’ll be uncomfortable, but healthy!]). What’s important to us is that we see things as they are, not as how we, or others, might like them to be.

So, as for our conclusion (pardon the repetition): The macro fundamental setup along with the longer-term technical trends exposed within the charts suggest that probabilities support further equity market gains during the course of 2018. Although we cannot emphasize enough the huge unlikelihood that they’ll occur amid the historic dearth of volatility we experienced in 2017. And, most important, we’re more than willing to change our views on market probabilities, when (not if) conditions call for it.

In closing:

We think it fitting to close our year-end letter with the ultimate timeless market message: We’ll expose, at the core, what truly dictates the pricing of goods, of services and of shares of stocks throughout the global marketplace:

Economists tell us that the dynamics of supply and demand dictate the pricing of market-based goods and services — and market technicians tell us that’s also what determines the price of a share of stock. Of course that makes perfect sense, and it’s critical to the human mind –that is, the human mind thinks that it’s critical to the human mind — to make perfect sense of things. In terms of stocks, we show it on the charts all the time.

For example, take a look at our daily chart of the S&P 500 Index for 2017: click to enlarge…

Following the price from left to right, those horizontal lines depict the price where some would say sellers (supply) and buyers (demand) found equilibrium. However, as you can see, it was always short-lived. Where supply exceeded demand — areas where the price stalled, then backed off (resistance) — we colored our lines red. We created a green line when demand ultimately exceeded supply (when the buyers overwhelmed the sellers) and, thus, the price broke above the previously stalled area (previous resistance).

Note how the green lines rest right atop the red: That would be where regret-ridden sellers — who abandoned their shares at the price where they previously had their way with the buyers — became buyers themselves as they fulfilled their vows to get back into stocks if they ever got back to where they previously sold. In essence, what was once resistance (where sellers overwhelmed buyers) thus became support (where buyers overwhelmed sellers) — which is actually when we create a green line.

That’s very cool, isn’t it? I mean, if you can get your head around the charts, if you can see previous areas of equilibrium, you can make huge money trading against those areas! Right?

Well, let’s throw up another S&P 500 chart.

Here’s March of 2003 to March 2009: click to enlarge…

Following left to right, playing support and resistance areas might have been nicely profitable for the self-proclaimed savvy trader; that is until the real estate bubble burst! My how previous support (briefly equilibrium) proved utterly nonexistent — how sellers overwhelmed buyers — when fear gripped the human psyche.

Review Part 2 for an explanation of how we come to terms with the risk illustrated in the chart immediately above.

Now, despite what the last chart above depicts, despite history, despite, frankly, what our eyes and our experiences tell us, far too many economists and, alas, market analysts would have us believe that the laws of the physical sciences can be applied to economics and to markets (areas that clearly fall within the realm of the infinitely less quantifiable social sciences). That the laws of economics and markets

that we can observe supply/demand curves, determine equilibrium and thus act accordingly. That, in stock market terms, we can chart (as we have above) supply and demand, or, better yet perhaps, we can apply a valuation model to a stock, or a currency, etc., and come up with an investible thesis that is sure to make us wealthy.

Well, as all investors, amateurs and pros alike, have or will come to realize, it’s just not that simple. Nevertheless, the market gurus persist: They explain how the supply/demand conditions of silver for example demand a $30/ounce price, while it continues to change hands in the teens. They dazzle us with discounted cash flow analyses (yes, we do it too) of, say, Apple, and place its true value at $200+/share (for years now), while buyers and sellers are presently content with $170ish.

While it is not our intent to entirely denounce or debunk the value of conventional economic/financial market thought, we just find that a strict adherence to what we view as its conjectures can be most dangerous when it comes to investing one’s money. We think it’s safer, healthier, and ultimately more profitable to couch market pricing as the sum result of the decisions made by the 7 billion human beings who inhabit our planet; to understand that it’s at best difficult to predict, let alone observe, phenomena that is ultimately influenced by our own participation in it.

I.e., it’s the attitudes, the desires, the greed, the fears, the whims of humans at any given moment that ultimately determines pricing — be it of Tesla stock (which utterly defies any conventional valuation model) or cherry tomatoes — within the global marketplace.

Hence, our ongoing, and painstaking, analysis of the data that inform us on what people (consumers and producers alike) are doing, where they’re spending their money and allocating their resources, whether or not they’re working, and how they feel about their present lot, as well as their future. And, perhaps most critically, when it appears as though their collective psyche has pushed stock prices further (in either direction) than what the data suggest their direct experiences justify.

With regard to the latter, the fact that we’ve all witnessed firsthand how folks can act irrationally, how, contrary to conventional economic thought, they don’t always act in their own best interests — how, therefore, their thinking is all-too-often the definition of inefficient — entirely proves that markets are inherently anything but efficient. Academia’s unwillingness to accept this reality speaks to the human mind’s need to make perfect sense of things. Better, and safer, when it comes to the financial markets, to resist that need!

Lastly, speaking of how folks (specifically you readers who happen to be our clients) feel about their present lot, we’d like to borrow the final paragraph from the “Our Purpose” page of our own website:

If our clients live their lives in comfort, if they go about their days without a financial worry, without reacting to or fretting over the inherent volatility of financial markets — if our commitment to them instills, or enhances, that sense of wellbeing — we are indeed successful as a firm.

Thank you for reading!

All of us here at PWA wish you and your loved ones a Happy and Prosperous New Year!