Link to Part 2

Link to Part 3, Section 1

Link to Part 3, Section 2

Link to Part 3, Section 3

Link to Part 4

The Dollar:

Several times in this year’s lengthy final message we’ve cited the potential for a rising U.S. dollar to be a headwind for a number of sectors, as well as foreign equities, in the year to come.

Our view is that a relatively strong U.S. economy, aided by the potential near-term positives of corporate tax reform, not to mention an infrastructure spending package (should it happen), along with a higher interest rate regime, and a Fed that is no longer reinvesting all of the income from its massive balance sheet, are factors that stand to support the dollar — if not see it rising — going forward.

Interestingly, however, currency experts seem to disagree. Bloomberg’s December 26th article Picking FX Winners for 2018 captures the sentiment:

Following the dollar’s worst year in more than a decade, foreign-exchange strategists see few signs of optimism for the U.S. currency in 2018.

Funny thing is, at the beginning of 2017, the prevailing sentiment among the currency crowd was one of optimism. They felt that the rally in the dollar that began with the presidential election would carry into 2017 on the back of tax reform, infrastructure spending, deregulation, an improving economy and higher U.S. interest rates. Which actually pretty well describes today’s setup; and now they’re bearish! Hmm…..

(My “Hmm” aside, conventional valuation metrics indeed show the dollar overvalued relative to most foreign currencies (supporting the present consensus). It’s just that, as in the stock market, valuations are virtually never, by themselves, good timing indicators. It’s more about overall conditions)

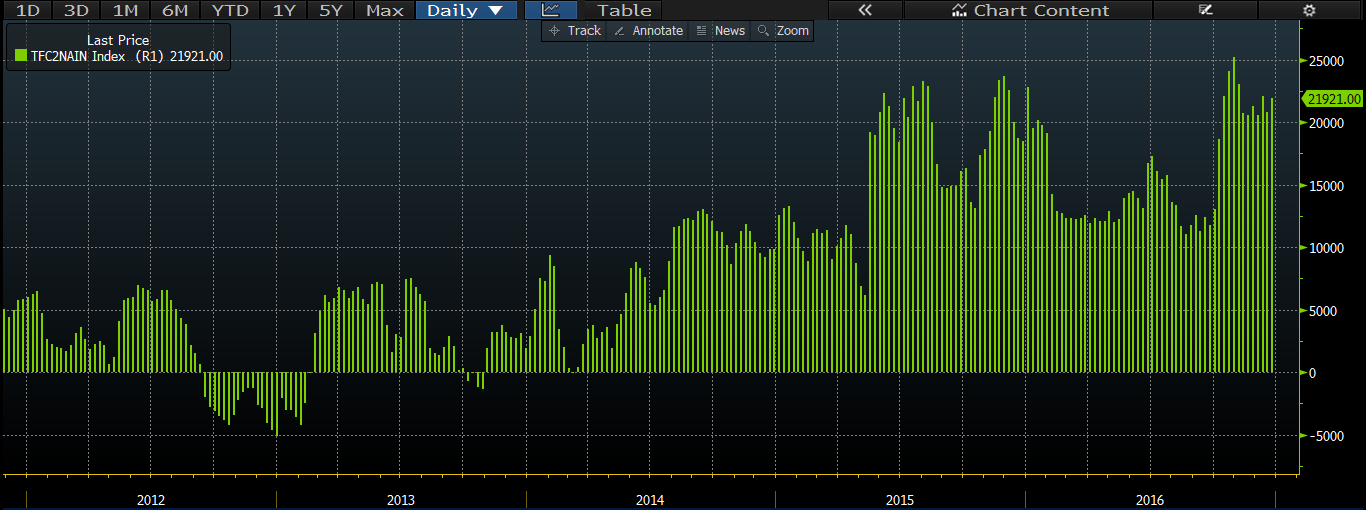

Here’s a 5-year chart (ending 12/31/16) of the net positioning among asset managers who trade futures contracts on the U.S. dollar index: click any chart below to enlarge

Per the chart, futures speculators were long the dollar to nearly the highest degree they’d been in 5 years, heading into 2017.

We actually were not in that camp. While we did not foresee a huge decline in the dollar in 2017, our view was that the Euro, in particular, was poised to do better on what we saw as the potential for a strong rebound in the Eurozone economy. I.e., while it was obvious that U.S. interest rates would trend higher in 2017 versus the Eurozone (conventional thought says traders migrate toward the currency with the highest yield), we expected that money would actually flow to Europe (as well as to the emerging markets) — creating a headwind for the dollar — based on opportunities in its asset markets.

And here’s how the dollar actually performed in 2017:

Here’s how the Euro fared:

Here’s from a May 2017 blog post where we highlighted some confirmation that we were on the right track (although we don’t want to overstate our position: Again, we did not see the big decline in the dollar coming, we simply anticipated events that kept us out of the bull camp coming into the year):

As I’ve been charting here on the blog, while the setup for U.S. stocks looked good coming into the year (still does), the setup for the Euro Zone looked every bit as good, if not better (still does). While stocks and economies don’t — particularly in the short-run — always correlate, the relative (to the U.S.) data coming from the Euro Zone of late support the setup, as well as explain the currency action.

Now, let’s not get ahead of ourselves, currency markets are no easier to predict than are equity markets, so we’re more than willing to concede that maybe this time the currency crowd has it (the dollar will decline throughout 2018) spot on, and that we (the risk is to the upside) don’t. The good news is that if they’re right (and we’re wrong), our clients stand to win. As those headwinds from a higher dollar that we cited in earlier parts of this letter won’t develop after all!

Bonds:

For our purposes here our focus will be on treasuries as a proxy for high quality debt securities. The factors that impact lower quality, high yield (junk) bonds have vastly different implications versus high quality bonds. Plus, generally speaking, the fixed income market is where we look to house the portion of client portfolios where safety (shelter from volatility) is our top priority. We generally look for growth (and volatility) from the equity markets.

We can keep our commentary on bonds short and sweet for now (of course we’ll be providing updates throughout the year):

Folks typically buy bonds for their safety and their income. The latter makes them very susceptible to interest rate fluctuations. For example, say you recently bought a 10-year treasury bond with a yield of 2.4%. Now you’re not at all stuck with that bond for the next decade, you can sell it anytime you like in the secondary market. Thing, is, if interest rates on newly issued 10-year treasury bonds rise to, say, 3% (maybe as folks demand a higher yield to compensate for what they might have earned elsewhere [as the economy improves], or because Congress passes a trillion dollar infrastructure plan and, therefore, the treasury has to attract investors to the greater amount of debt they’ll have to issue to fund it, and so on), who’s going to buy your 2.4% bond? Well, believe it or not, somebody will, but they won’t pay you nearly what you paid for it. I.e., you’ll lose money!

Now, someone — maybe the broker who sold you the 10-yr treasury — might tell you that “you have no risk; all you have to do is keep the bond for the duration.” Well, okay, but imagine all of the income you’ll miss out on if rates stay notably above the 2.4% (an historically low yield) you originally bargained for!

Bottom line: Given all that we’ve stated in this year’s year-end message about economic prospects going forward, we continue to relegate our clients’ fixed income exposure to cash and short-term CDs. However, those prospects could have us finally wading back into the bond market — as prices tank — in the not too distant future. Albeit gingerly at first.

Gold:

Of all the stuff you and I can invest in, gold has to be the most fascinating. It’s amazing to me that a metal that has such little practical application can amass what, in our view, amounts to a large cult following. The passion in which certain pundits pound the table on gold can be startling. Clearly, for them, it’s about ideology, emotion and ego! For us, it’s about reality.

Now, we can argue all day long about the efficacy of a gold standard, while, in today’s real world we aren’t on one. The fact that many folks — and we won’t say illegitimately — pine for the old days, doesn’t, in our view, justify their rabid bullishness on the metal every time the U.S. budget numbers come out, or when they project the national debt 10-years hence. Not that those aren’t legitimate long-term concerns (I’ve devoted many an essay to the subject: Warning! book plug) — or that gold isn’t the ultimate hedge — it’s just that they’re not near-term concerns. For the time being the world still wants what we got. And as long as that remains the case, the dollar’s in relatively good shape, and while gold will absolutely rise and fall on the dollar’s moves, and on the geopolitical conflicts to come, the economic pressures that would result in massive deflation, or hyper inflation, just aren’t on the horizon as we sit here today.

We could go on and talk about gold as a trade. On how speculators are quick to bid the price higher on the odds of a North Korean missile launch, a presidential scandal finding pay dirt, a jobs number missing its estimate, the Fed not raising interest rates as aggressively as previously thought, or any number of other potential events or mishaps — or how they’ll sell it to the ground on the release of a better than expected jobs number, or the resolution of some frightening geopolitical conflict, but, for now, we’ll move on to silver.

Silver:

If I had a silver dollar for every time a client asked us about silver in 2017, well, I’d be a few silver bucks richer today.

It’s interesting, folks virtually never ask about silver because the global industrial economy is in growth mode and silver is a widely-used industrial commodity. They ask because they put it in the same class as gold (a hedge against the end days) and someone told them that its long-term relationship to gold says that its presently very cheap. I.e, the gold/silver ratio is historically wide and, therefore (in theory), silver is likely to rise — as things tend to revert to the mean.

Always happy to play devil’s advocate, I typically say to those folks, “well, sure, the ratio can get back to historical norm by silver rising in price, but it can also get there by gold falling.”

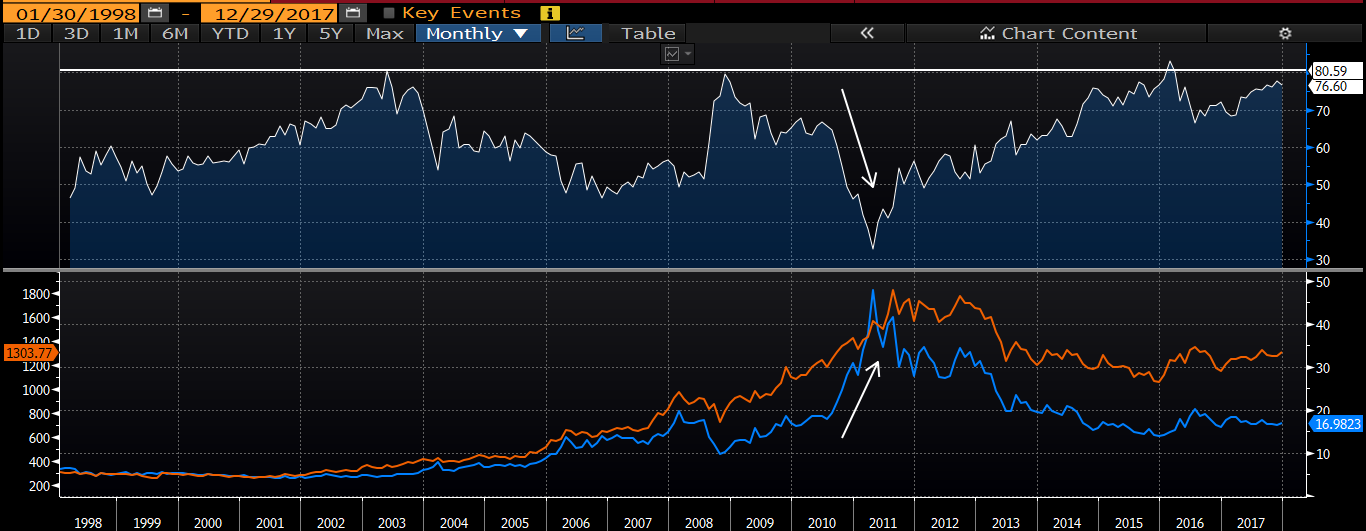

Taking a look at a 20-year chart of the gold/silver ratio (top panel), one can see where the silver bulls are coming from. In 2011, when the ratio was coming off of a level just above where it currently sits, its subsequent contraction indeed occurred due to a serious silver rally (bottom panel; gold in orange, silver in blue):

But here’s the thing, while silver was spiking higher, gold was also on the rise. If you follow the lines in the bottom panel, you’ll find that, directionally-speaking, gold and silver tend to move together. I.e., the odds that silver can rally hard while gold’s on the decline, are quite slim indeed. Therefore, given today’s general economic state of affairs, we believe probabilities favor that the most likely scenario resulting in a contraction of the gold/silver ratio would be an accelerated decline in the price of gold, as opposed to a rampant rise in silver.

Now, all that said, as sure as I’m sitting here this blog post will find its way onto the computer screen of somebody who has dug much deeper than the simple gold/silver relationship we discussed herein. They will, for example, justifiably slam me for not citing the reported huge mismatch between the demand for silver versus its supply in 2011, which of course, they’ll exclaim, resulted in its rapid run higher. The problem is, they won’t be able to explain what happened as silver crashed back to earth amid the essentially same fundamental supply/demand backdrop. Actually, they will, but their explanations will come wrapped in fascinating conspiracy theories involving manipulation by the banking system. Regardless of whether or not their claims carry water, you and I have to live in the real world, and, for the moment, real world intermarket relationships say that a bullish scenario for silver needs a bullish scenario for gold. And, recent rally — and geopolitical/fed policy hiccups — notwithstanding, we don’t see an investible scenario for silver (relative to other alternatives) as we head into 2018.

Lastly, if you feel you must own a precious metal to hedge against the next calamity (not saying that’s a horrible idea by the way), I personally would chose silver over gold. Or maybe buy some of each.

Next up, part 6: Conclusion

Link to Part 6