Link to Part 1

Link to Part 2

Link to Part 3, Section 1

Link to Part 3, Section 2

Link to Part 3, Section 3

If there’s been a common theme over all the years we’ve been blogging, and, for that matter, managing money, it’s that the world is a very big place, and the U.S., in terms of its share of the world’s human capital, is a very small place. While we can debate the causes of the miracle that makes the home of a mere 4% of the world’s population the far and away world’s largest economy, we can’t deny the fact that the human race is becoming more connected by the minute and, thus, the nations and institutions that embrace the interdependence that this global connectivity breeds — while successfully navigating the at times turbulent geopolitical waters — will prosper the most in the decades to come.

In mid 2016 we produced the following video on global investing. We believe it remains timely, instructive, and clearly illustrates the opportunities that abound beyond our borders. It essentially foretold the out-performance we’ve experienced of late from our non-US exposure.

Please take a few minutes and watch. As you’ll gather from the video, and as you’ll see in the updated charts below, the longer-term prospects for global investing remain quite compelling.

Click the wheel to the left of “YouTube” to improve the clarity…

Now, bringing the charts forward:

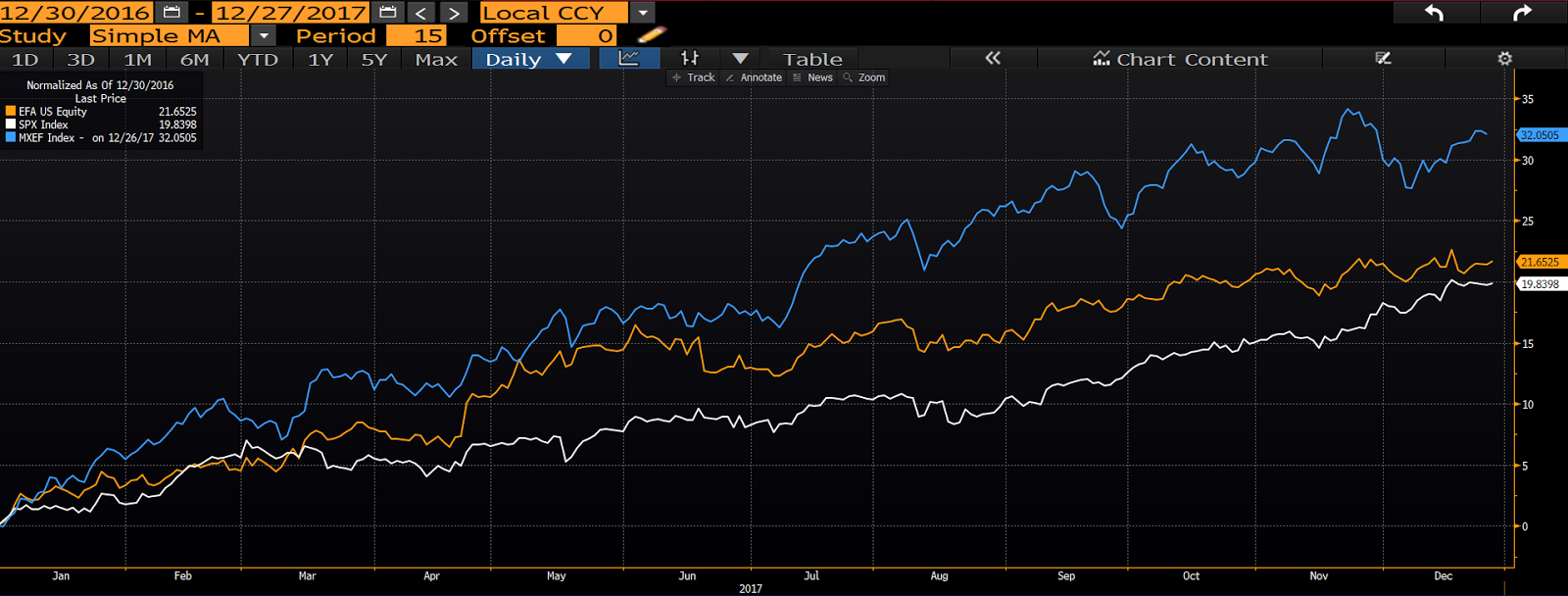

Here’s a look at the performance of the U.S. S&P 500 Index (white line), developed non-US markets (yellow) and emerging markets (blue) in 2017. As you can see, after a long period of under-performance, non U.S. equities were, in the aggregate, the best places to be this year:

Click any chart below to enlarge…

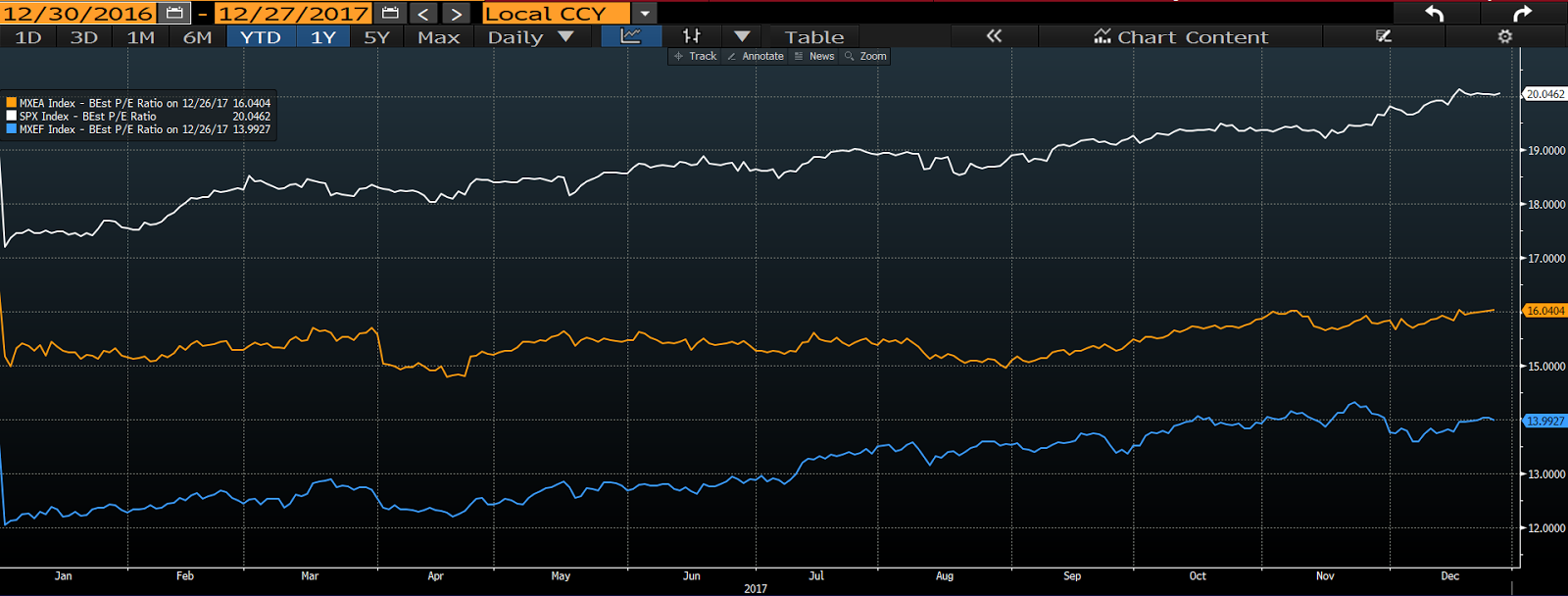

In terms of valuations, non-US markets remain notably cheaper (from a price to earnings standpoint) than the U.S.:

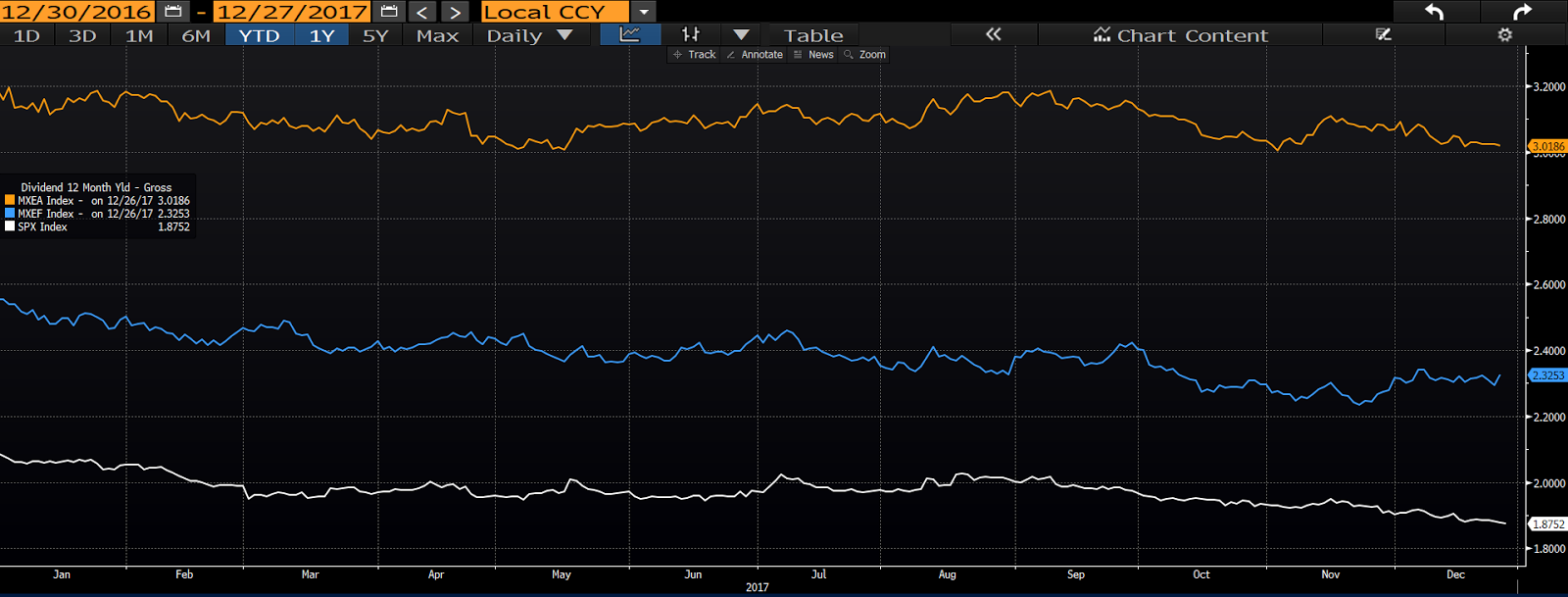

And foreign stocks continue to pay notably higher dividends:

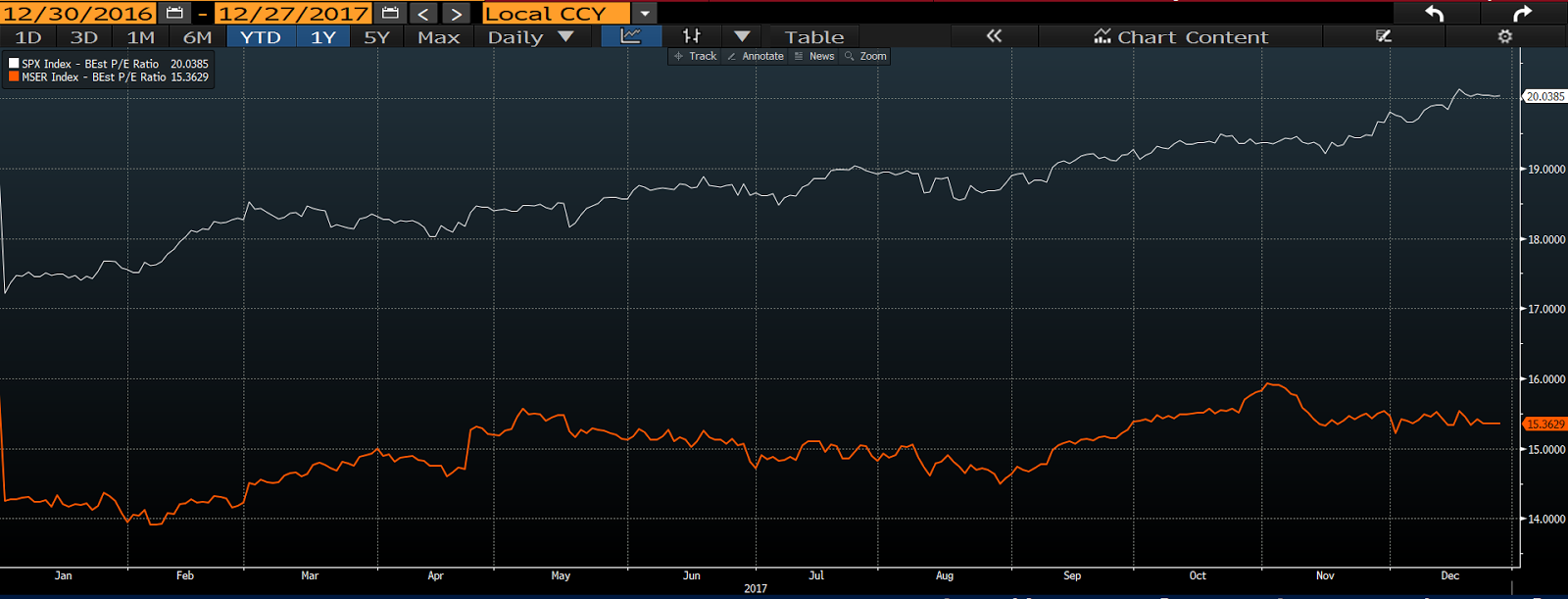

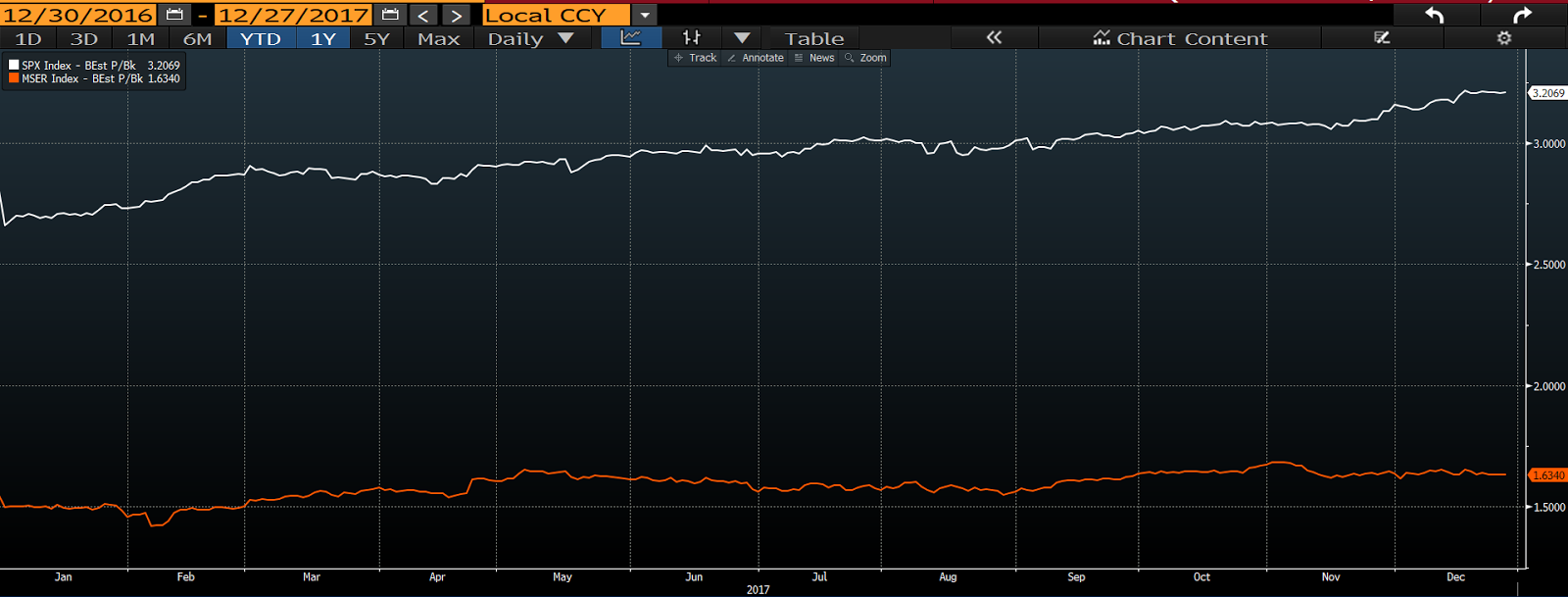

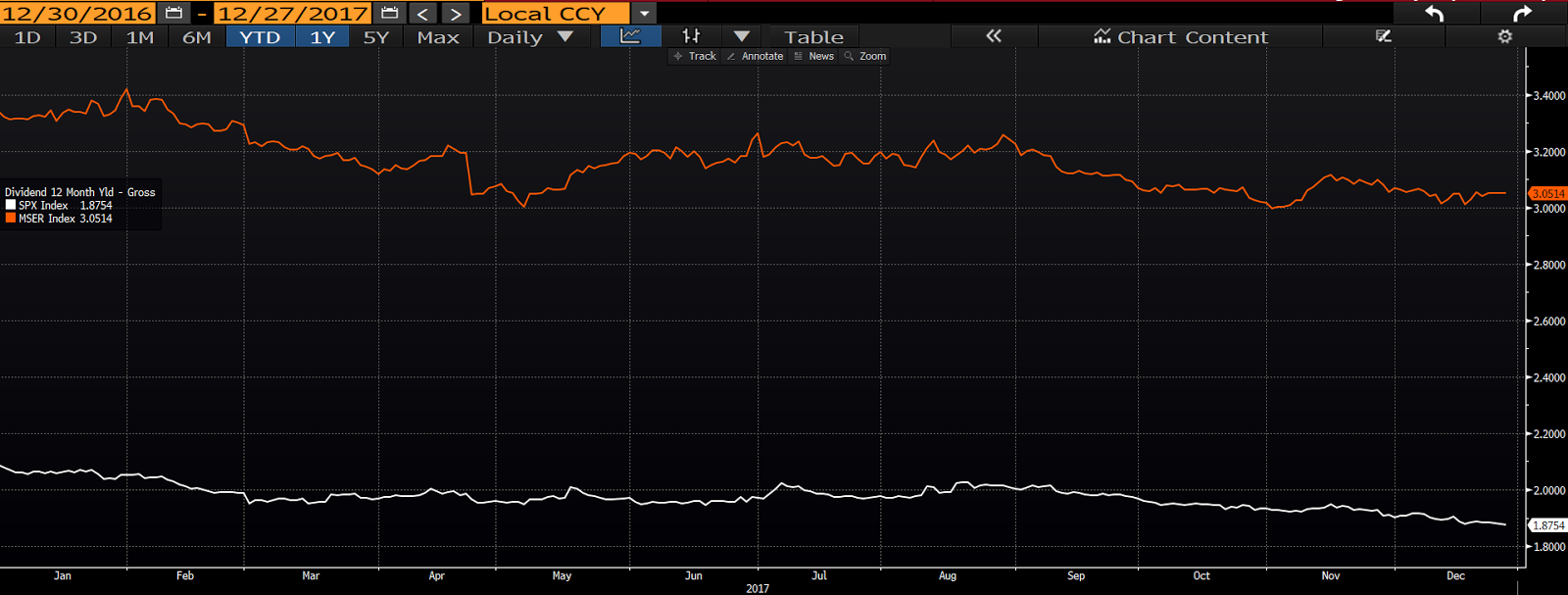

Zeroing in on the Eurozone versus the U.S.:

Eurozone stocks remain cheaper on a price to earnings basis:

Also on a price to book basis:

And from a dividend yield standpoint as well:

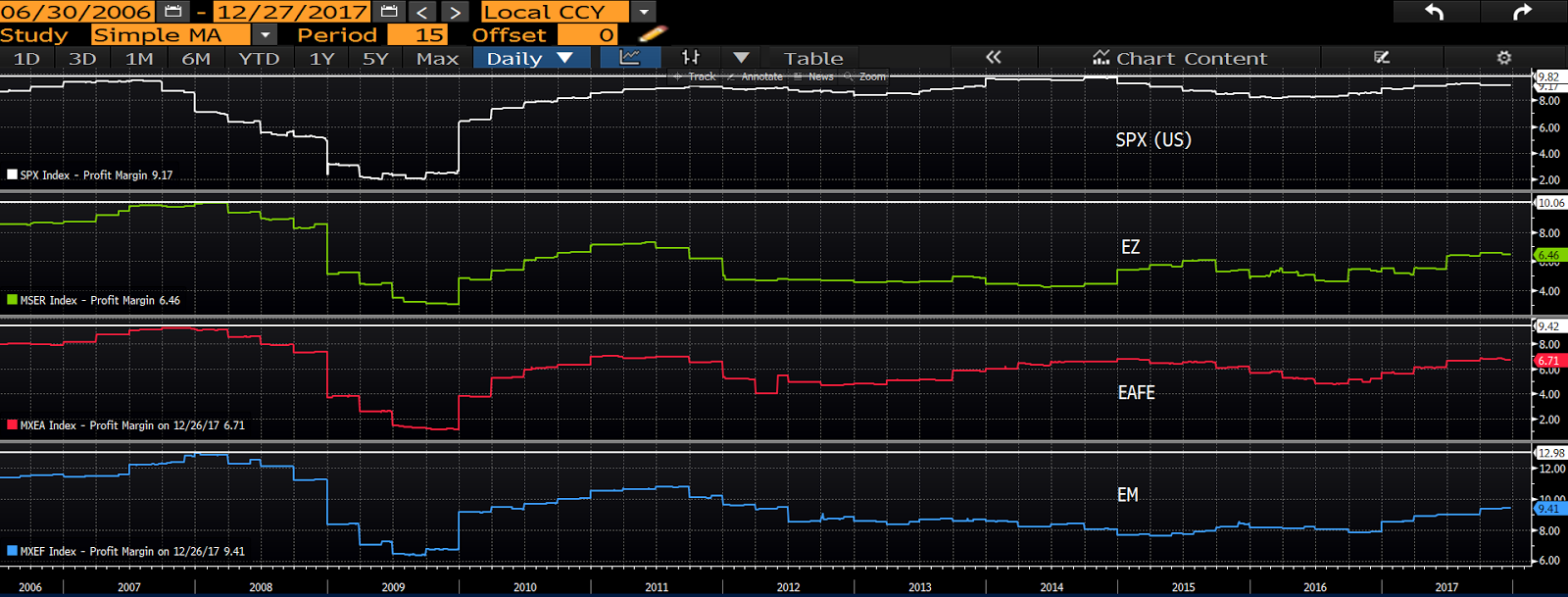

In terms of profit margins globally; the U.S. is still flirting with record margins, as the rest of the world, while now seeing margin growth, still has a ways to go:

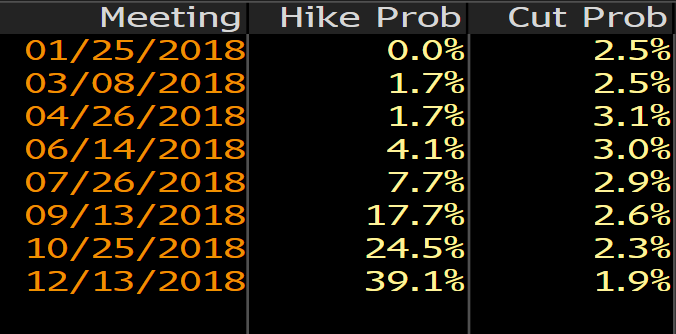

Lastly, the one dynamic that has markedly changed is that after a strong rebound in economic activity the European Central Bank is no longer in aggressive easing mode. In fact, the futures market is now pricing in ECB rate hikes later next year:

Now, all that said, foreign investing involves additional risks that can turn the most compelling long-term thesis into the most palpable short-term turmoil; geopolitical risk being the most obvious.

The other major dynamic occurs within the currency markets. 2017’s declining dollar provided a major boost to our non-US holdings during the year (as foreign denominated profits translated to greater U.S. dollar earnings). Should the dollar reverse and move higher — amid higher U.S. interest rates and an accelerating U.S. economy — it will indeed become a headwind, despite the fact that a stronger dollar will make foreign-made goods cheaper for U.S. consumers (a potential offset to the currency translation risk).

Bottom line: While we’re not quite as near-term bullish on Non-US vs US as we were at the start of 2017, the weight of the evidence keeps us firmly committed to our present base targets.

Next up, Part 5: The dollar, bonds, gold and silver…

Link to Part 5