Link to Part 1

Link to Part 2

Link to Part 3, Section 1

Here’s a brief synopsis of what we view as today’s fundamental aspects of the industrial, materials, energy and consumer discretionary sectors. We want to emphasize “brief“, as we could easily offer up a lengthy research paper for each.

Note, the following relates primarily to the prospects for sectors within the U.S. economy. Our targets are also influenced by our assessment of each sector within other countries — as we maintain target allocations to foreign markets as well. A topic we’ll tackle in Part 4.

The industrial sector, at 18% of equities, currently ties with financials as our top target weighting heading into 2018. Bottom line: The world is building and America is spending (and taking delivery).

Here’s some proof:

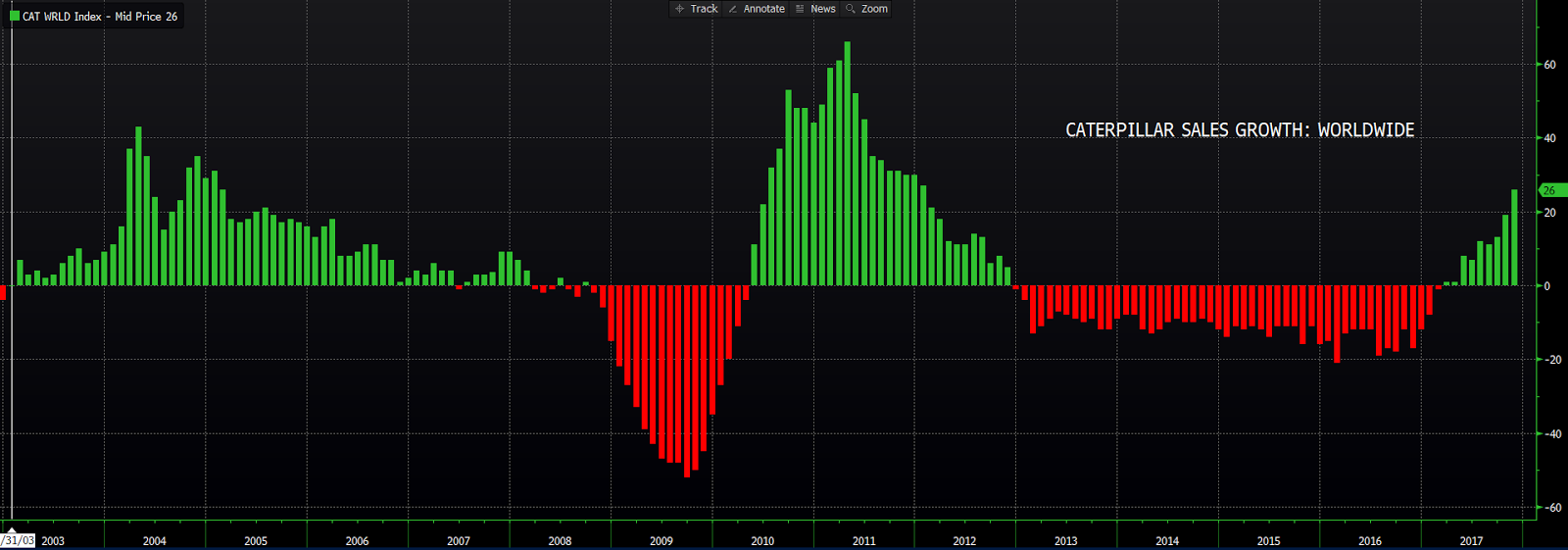

Caterpillar’s global equipment sales are on the rise for the first time in years:

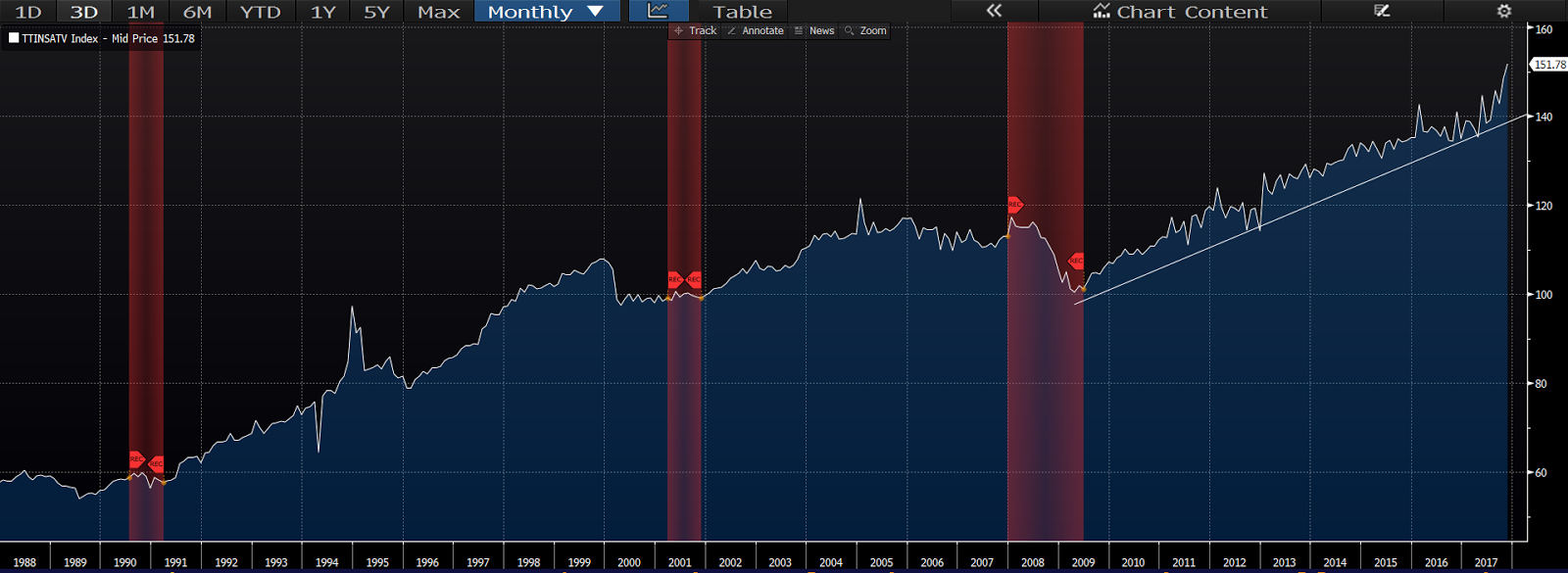

Our truck tonnage chart is showing notable acceleration of late:

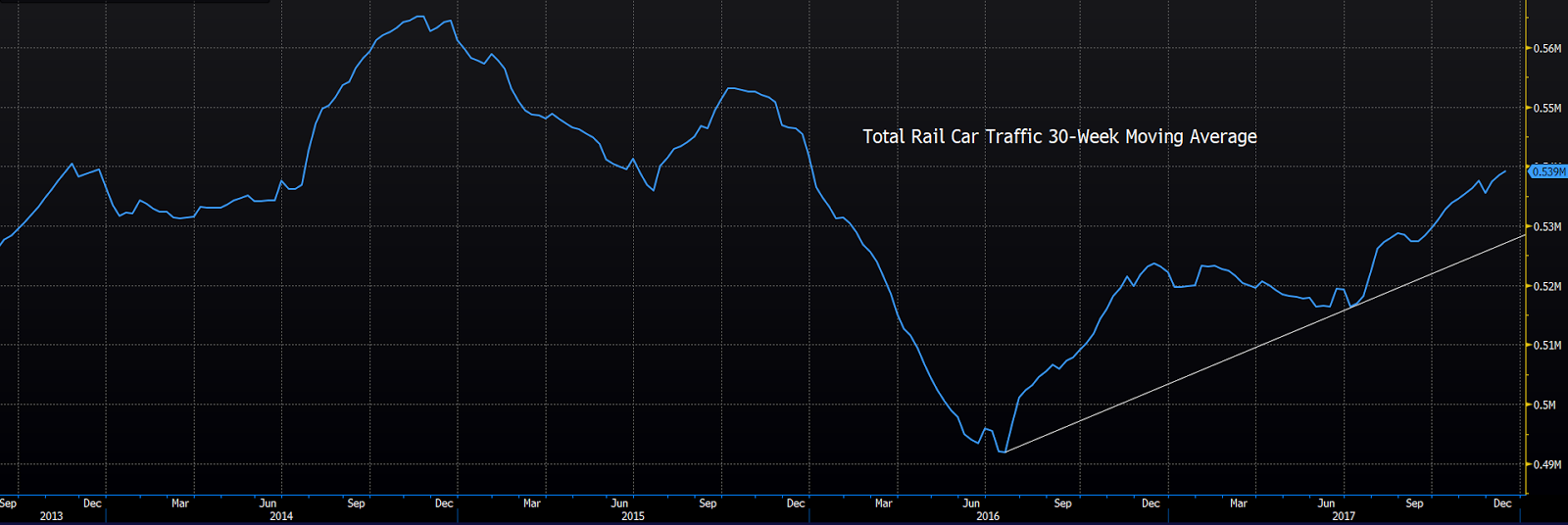

As is our chart of total rail car traffic:

Here are some key themes we see impacting the industrial sector going forward:

1. Infrastructure Spending: While much of the world is already heavily engaged in infrastructure investment, the U.S. looks to be just beginning. We were touting these prospects months before last year’s election (when the ultimate outcome was not something we were anticipating), as the Democrats were pounding the table every bit as hard as, if not harder than, the Republicans on the need for infrastructure investment in the U.S.. Thus, passing an aggressive infrastructure spending package will likely be a relatively easy win for the Administration in 2018. Although, not everyone agrees…

2. Transportation: Per the charts above, goods (as are people) are moving across the roads and railways (not to mention airways) of America. Of course this is consistent with our macro model’s presently high score, and, thus, speaks to the present strength of the economy. Transportation companies (ground, rail and air) are well represented in our core industrials ETF.

3. Defense Spending: The U.S.’s major defense contractors occupy prominent positions in the top 20 holdings of our core industrial sector index ETF. These multinational companies stand to gain from defense spending in other nations as well.

4. Tax Reform: U.S industrial companies stand to be major beneficiaries of the drop in the corporate tax rate; with an estimated 16.7% boost to earnings.

5. The U.S. Dollar: A strengthening U.S. economy, higher interest rates and a less accommodative Fed could result in a higher trending U.S. dollar in 2018. Given that there’s a real multinational flavor to many of the companies that comprise the industrial sector, a rising dollar poses a potential headwind. At this juncture, however, we believe that the positives stand to overcome this potential negative, despite what we expect will be a heightened sensitivity to a rising dollar among traders.

6. Protectionism: Now, combine a potentially higher trending dollar with higher barriers to international trade (which has, thus far — notable exception(s) aside — been more rhetoric than realty) and we’ll have a combination that could ultimately put our bullish thesis to the test.

The basic materials sector, with a 15% of equities target, is uniquely positioned to prosper given the present global economic setup.

Here are some key themes we see impacting the materials sector going forward:

1. Infrastructure spending: See #1 under industrials. Of course all of that construction will require tons upon tons of virtually every industrial material known to man.

2. Inflation: While inflation has been virtually non-existent in the current recovery, our view of the labor market, of commodity trends, of reports from the manufacturing sector, and of the increasing pace of factory capacity utilization, is that its acceleration is virtually at hand. Inflation running a bit above the Fed’s 2% target should not be viewed, at this stage, as problematic, but rather as a driver of increased revenue for the materials sector — as well as being indicative of an economy that is healthily moving into the later-mid stages of expansion. Higher-trending materials prices, amid a pickup in capex spending (investment in productivity-enhancing expansion), suggests that much of that increased revenue would flow straight to the industry’s bottom line. Additionally, such gains in productivity, while making for more profitable companies, may also keep inflation from becoming problematically high in the foreseeable future.

3. Lithium miners: Lithium is an essential element in the batteries that power the mind-boggling technology — from smart phones to self-driving electric cars — of today and tomorrow. Our core materials sector ETF features two of the world’s premier lithium miners in its top 20 holdings.

4. The U.S. Dollar: Given the commodity-centric nature of a number of names within our materials ETF, a rising dollar could pose a headwind. In addition, there is sufficient foreign revenue exposure within the group to make a rising dollar potentially problematic. However, as with industrials, we think the presently positive setup for the materials sector stands to effectively mitigate the potential negative effects heading into 2018. That said, as we stated in our summary of the tech sector, we do anticipate a heightened sensitivity to dollar dynamics among traders, it’s just that we believe that sensitivity will be expressed more among the tech names versus other sectors.

5. Tax reform: Materials companies are expected to see a 9.4% boost to earnings as a result of the coming cut in the corporate tax rate.

6. Protectionism: Ditto #6 above.

The energy sector, with an 8% of equities target, while showing renewed signs of strength of late, has its challenges.

Here are some key themes we see impacting the energy sector going forward:

1. High demand: Energy products will remain high in demand in an expanding global economy.

2. OPEC: OPEC, along with Russia, have agreed to keep 1.8 million barrels of oil per day off the market through the end of 2018. Which has indeed helped out the price of late. However, OPEC’s nemesis, North America, will continue to exploit its efforts to the fullest. I.e., as OPEC cuts (and supports the price) North America ramps up production, effectively quelling the desired rise in price.

3. Profitability: Amid strong demand, and OPEC’s efforts, a price per barrel back below $40 is highly unlikely in 2018. However, at a price much below $50, we should see any expansion in North American shale production slow measurably, as we’ve seen estimates of the break-even price for shale producers of between $40 and $55 per barrel. The share price action of the companies that comprise our core energy ETF are of course highly correlated to the fluctuating price of oil. However, if prices can remain stable above $50, the renewed strength we mentioned above can persist, and it’ll show up in company earnings.

4. Renewables: While the world will continue to consume fossil fuels into the future, anyone who would deny the fact that the industry faces major challenges, as the world pushes to clean itself up, is, well, in denial. Thus, while we’ll indeed see geopolitical, etc.-induced spikes in the price of a barrel from time to time well into the future, the longer-term trend will indeed be a lessening of dependence on fossil fuels and, thus, a massive structural rebalancing that, again, poses major challenges for the industry in the years to come.

5. Tax reform: Energy companies — with a whopping 25.9% boost to earnings — are estimated to be the chief beneficiaries of the corporate tax rate cut. This helps for sure!

6. The dollar: Oil is still traded primarily in U.S. dollars throughout the world. Thus, the price of a barrel is indeed influenced by fluctuations in the U.S. currency. A rising dollar in 2018 can, therefore, become a notable headwind.

The consumer discretionary sector is where folks hang out when they’re feeling good about their present and future financial condition.

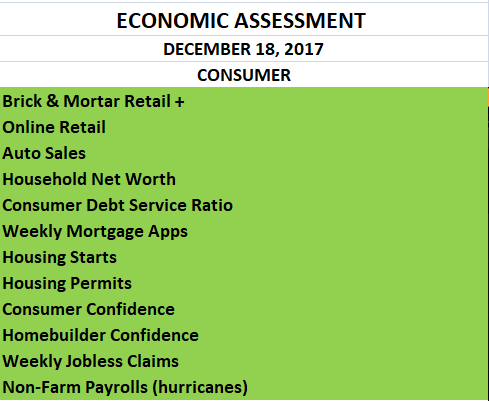

Ironically — thanks to the recent success of brick and mortar retail — for the first time all year the consumer-driven inputs to our macro model are all colored green. Here’s that section from our last update:

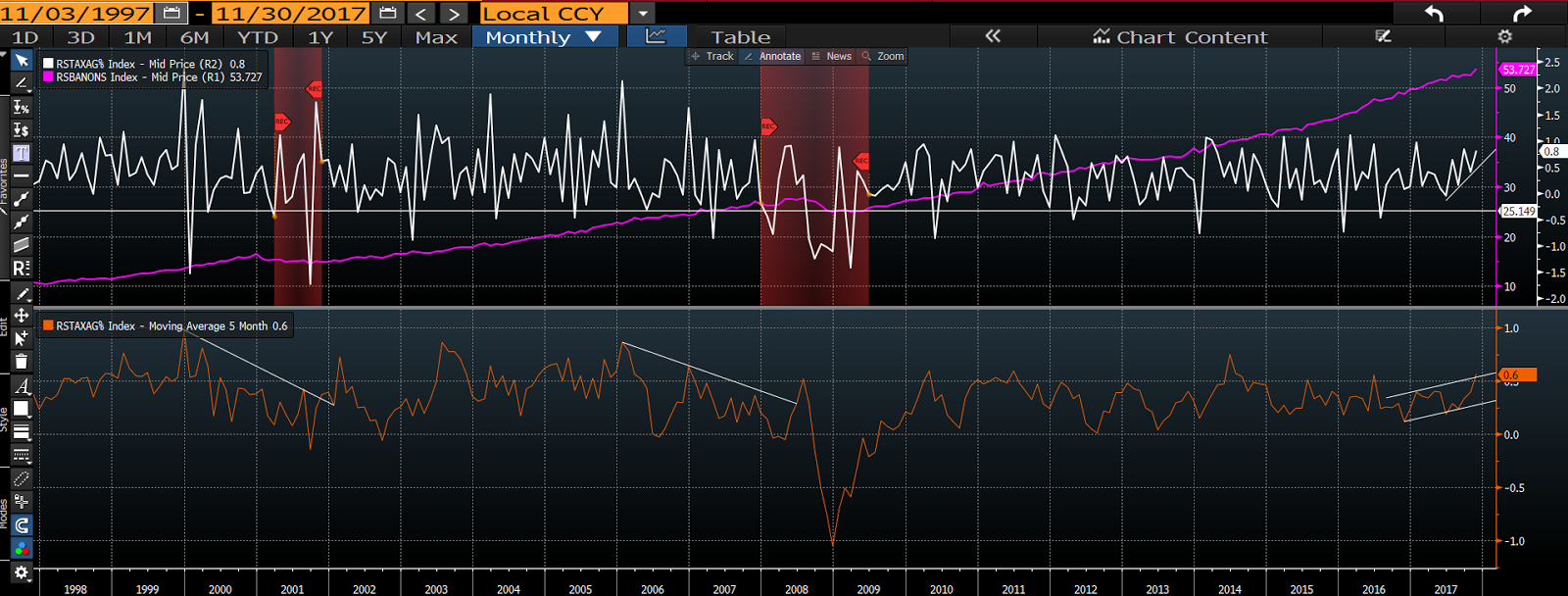

Here’s a look at our retail sales chart (white line is the monthly brick and mortar number, the purple line is online retail, red shaded areas are recessions. The orange line in the lower panel is brick and mortar sales’ 5-month moving average): click to enlarge

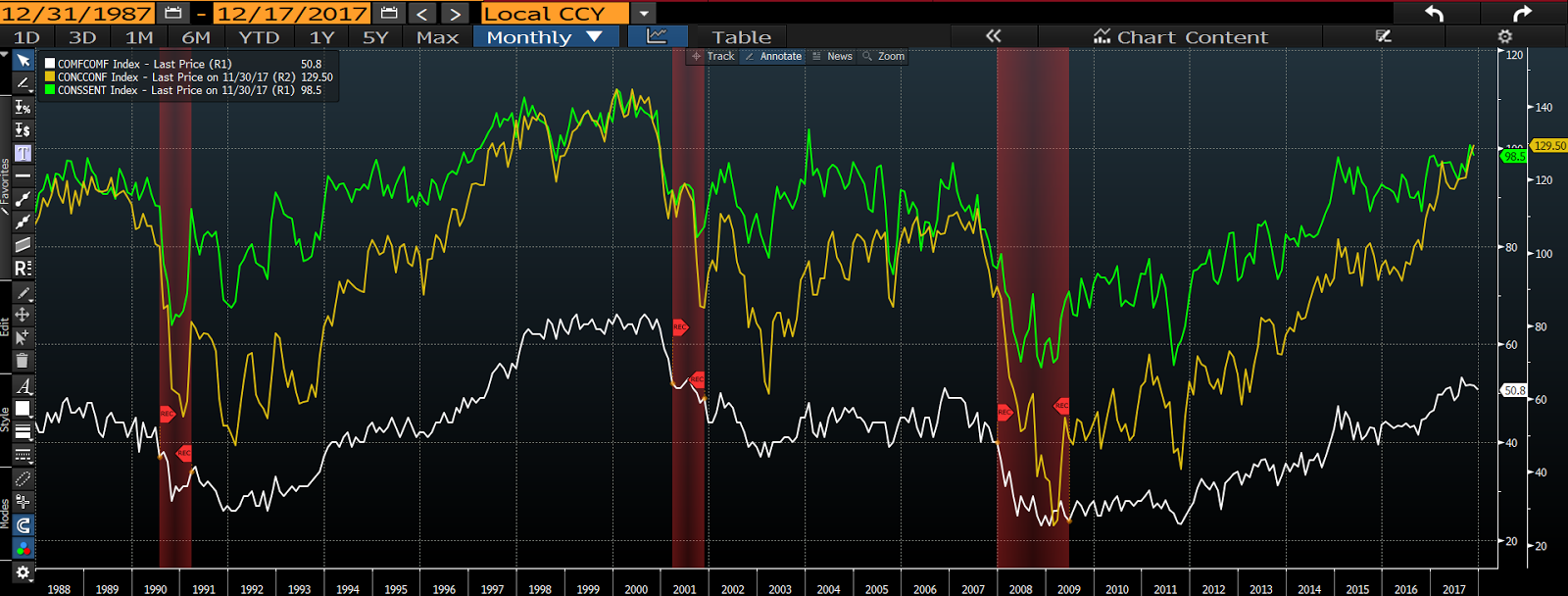

And here’s the latest in consumer sentiment (green and yellow lines are monthly survey results from the University of Michigan and The Conference Board respectively. The white line is Bloomberg’s weekly consumer comfort index. Red areas are past recessions): click to enlarge

I.e., we’re feeling good enough about our base 10% target to the consumer discretionary sector to push it toward the upper limit (12%) in most client portfolios. Our only hesitation — and a slight one at that — is valuation; at 20.4 times next years estimated earnings the sector sits as our third most expensive, behind REITs and energy.

In case you’re wondering why we’re only slightly hesitant regarding a sector that trades above 20 times estimated earnings during the second longest bull market in history, well, as we illustrated back in June, price to earnings ratios are terrible market timing indicators.

Next up, health care, utilities, telecom, consumer staples and REITs.

Oh, and before you (you readers who aren’t our clients) run out and put all you got into industrial, materials and consumer discretionary stocks, remember our basketball analogy from Part 1: Even the very best ‘shots’ will miss the mark from time to time, it’s part and parcel to the business of investing.

Once again:

….while good investments can, and often do, lose money, if we take only shots where the setup makes good sense — i.e., if we take only good shots — and we take them from multiple angles and distances (diversify), we believe that we give our clients the absolute best odds of achieving long-term investment success.