Link to Part 1

Long-time clients and readers know that while we pay very close attention to market technicals (price trend, momentum, volume, breadth, sentiment, etc.) when positioning client portfolios, it’s our view of general conditions that holds the greatest sway. The overriding question being, are present conditions conducive to growth in corporate earnings? And, if so, which sectors of the economy are best (and least) positioned given those conditions. Or, if not, which asset classes are best positioned to weather, if not exploit, a less than bullish, or outright bearish, macro scenario.

While it’s tempting to post herein the charts representing the 73 entries to our predominantly U.S. (12% of the data points reflect global conditions) macro model — which organizes and scores the data that instruct our view of general conditions — in the interest of keeping you interested we won’t. Instead, we’ll offer up recent overall scores and illustrate why a thoughtful analysis of macroeconomic conditions — in addition to robust technical analysis — is critical to our confidence level as we manage client portfolios.

In terms of what our system tracks: 71% of our model is comprised of hard (jobs numbers, housing starts, industrial production, etc.) and soft (sentiment) data related to consumer and business activity, to inflation, to general financial stress, to commodity trends and to “other/general economy”. The remaining 29% is devoted specifically to U.S. equity market internals.

On January 1 of this year our macro score came in at +42, with 69% of the data reading positive, 10% negative and 21% neutral. Hence — along with a bullish technical setup — our optimistic view of equity market probabilities coming into the year.

In case you’re wondering, the setup back in June of 2016 was nothing to sneeze at either; with our macro score coming in at +29, with 56% of the data reading positive, 16% negative and 28% neutral.

Now we’ll dig into why we do so much work on macroeconomic fundamentals.

Take a look at this weekly chart of the S&P 500 Index spanning the past 30 years: click any insert below to enlarge…

Now let’s do a little technical work.

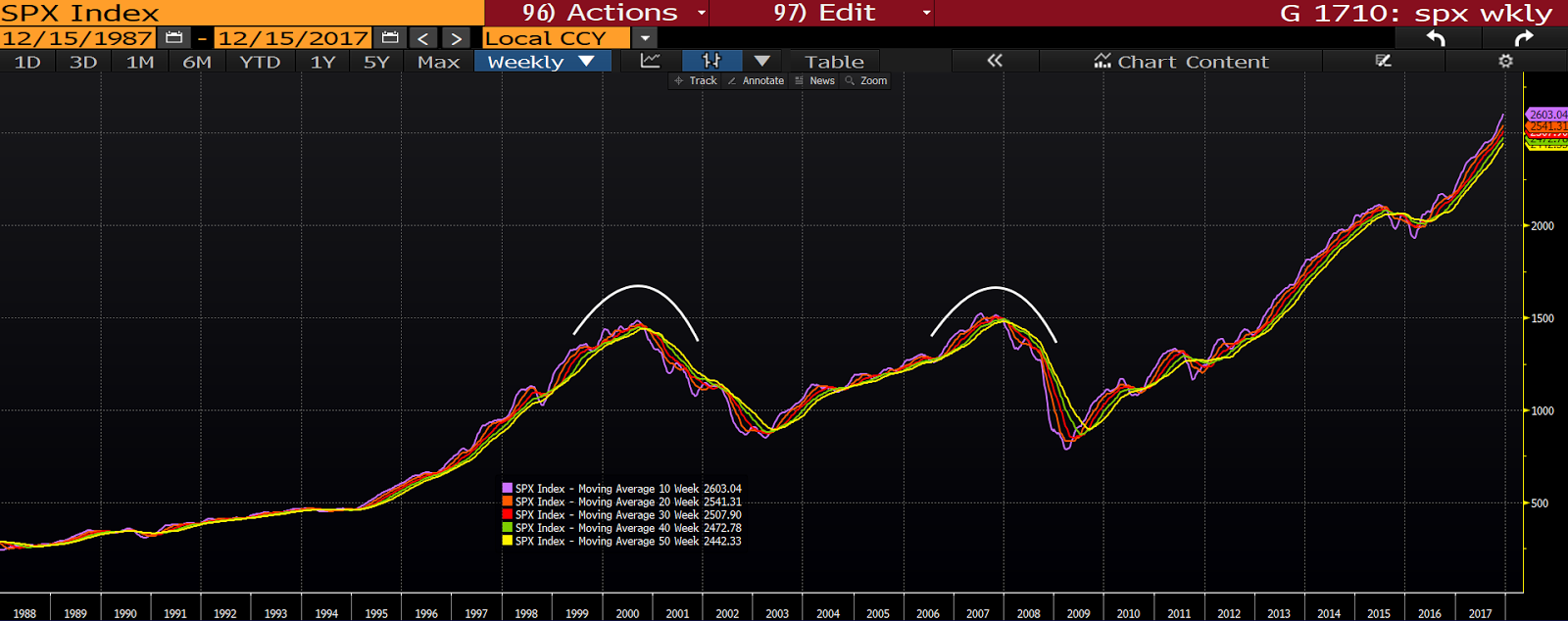

Here’s the same chart with the 10, 20, 30, 40 and 50-week moving averages added:

A look at a given index or security’s moving averages offers the analyst a picture of the prevailing sentiment in the aggregate of all market participants. The most bullish scenario exists when the fastest (shortest-term) moving average is on top, with the slower (longer-term) falling below in sequence — while all are curving upward. A bearish scenario is the reverse, with the slower moving averages atop the faster — while all curve downward.

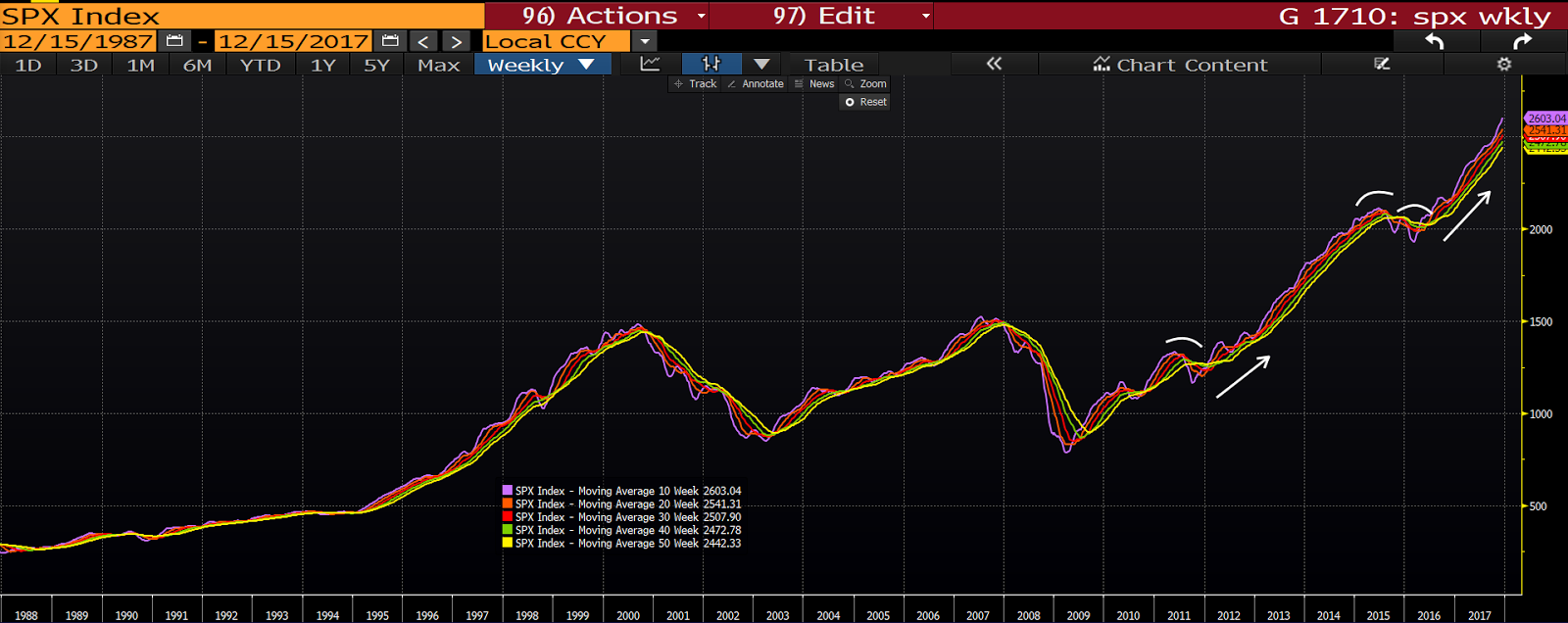

Here again is the 30-year weekly chart, this time with price removed. Notice the rolling over and the reversal of positioning of the moving averages as the stock market moved into two of history’s worst bear markets:

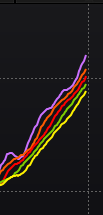

in essence, when the moving averages look like this —

(today, in fact) — probabilities favor stock market gains going forward.

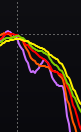

When they look like this —

— look out below!

So there you have it: Easy peasy! Just track a series of moving averages and stay aggressive when the faster are on top and all are positively sloped. And get defensive when the slower are on top and the slope’s negative.

Well, not so fast! What about those times when it appeared as though a rollover was eminent, but then, out of the blue, the market turned higher and the bullish setup resumed:

The 10+% corrections of 2011  , 2015 and 2016

, 2015 and 2016  were painting technical pictures that screamed get defensive. But, alas, those who did no doubt found themselves dumbfounded as the market turned back around just after they repositioned to a more defensive posture. Imagine the emotional struggle as these folks pondered if and/or when to adjust their weightings back to the growthy allocation that their then recently-failed indicators demanded.

were painting technical pictures that screamed get defensive. But, alas, those who did no doubt found themselves dumbfounded as the market turned back around just after they repositioned to a more defensive posture. Imagine the emotional struggle as these folks pondered if and/or when to adjust their weightings back to the growthy allocation that their then recently-failed indicators demanded.

So what’s an investor to do? I mean, clearly, the technicals work much of the time, but my how unfortunate the results when they don’t!

This is where macro fundamental analysis comes in.

Here’s the moving average only chart along with our macro model scores back when things were getting dicey. In the two ultimately bear market instances we featured the scores before the moving averages actually rolled over (i.e., when the technicals were still relatively positive). In the two false signal (for long-term investors) instances we ran the backtests at virtually the worst possible times (when the market seemed on the verge of falling apart):

Now you know why our view of general conditions holds sway over the technicals. Even before the market rolled over — ahead of the respective burstings of the tech and real estate/mortgage bubbles — our macro analysis was pointing to a high probability of rough times ahead. While in the midst of three double-digit corrections — that were simply pauses in an ongoing uptrend (or, as a technician would say, “countertrend moves”) — our macro model remained on balance bullish.

Has PWA thus discovered the Holy Grail of asset allocation? Well, absolutely, unequivocally and emphatically NO! Folks — make no mistake — when it comes to financial markets there is no Holy Grail! Anything can happen! Recall from Part 1; “good investments that lose money.” The best we can do is use the tools at our disposal to assess present conditions and act accordingly.

To borrow from a Jesse Livermore quote also featured in Part 1:

“…all a man needs to know to make money is to appraise conditions.

In essence, our investment decisions reflect go-forward probabilities (never certainties) based on the weight of the evidence (never on whims, hunches or nerves). All the while we remain flexible and keep our minds open to all possibilities.

Oh, and by the way, our macro score presently sits at a very bullish +60, with 85% of the data reading positive, 3% negative and 12% neutral. Which explains our presently growthy sector allocation within client portfolios.

Areas that improved notably (moving from negative to positive) during the year ironically reflect global macro conditions; such as the Merrill Lynch Global Financial Stress Index, Caterpillar global sales, and the trend in copper pricing. The VIX curve (a measure of volatility) also went from negative to positive. The areas that moved from neutral to positive are non-farm payrolls, truck tonnage, railcar traffic, the TED spread (a financial stress indicator), the emerging markets economic surprise index, the Baltic Dry Index (tracks ocean shipping costs for dry bulk materials throughout the world), the CBOE put/call ratio (sentiment) and two U.S. stock market breadth indicators. There are only two areas that show deterioration versus the start of the year; small business capex (expansion) plans and NYSE short interest (sentiment) went from positive to neutral.

We’ll get a little deeper into the weeds in Part 3.

Link to Part 3, Section 1