We think there’s something to be said for the old Wall Street adage, “bull markets climb a wall of worry”; if only for the fact that while there’s worry in the system, there’s uninvested cash in the system. It also jibes with John Templeton’s oft-quoted and forever prescient line:

“Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

Here’s a PWA adage for ya, “bull markets climb a wall of confusion”; which we believe speaks to the situation we presently find ourselves in.

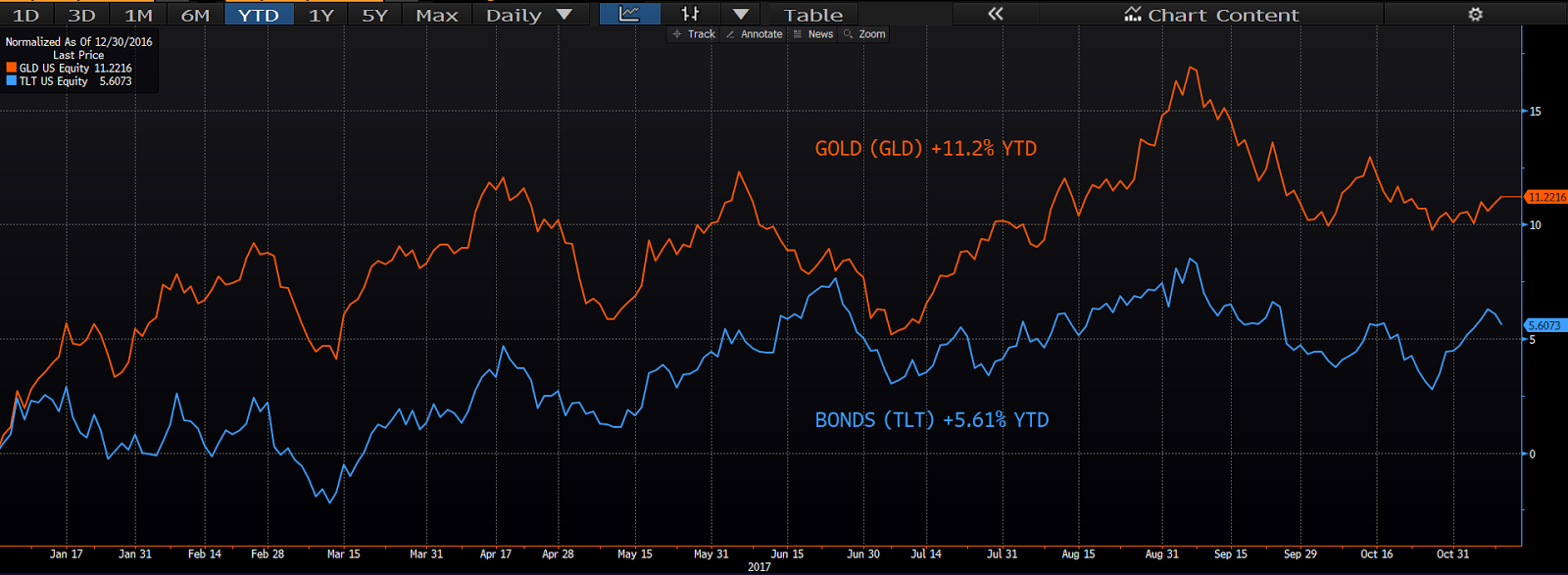

The confusion being evidenced by certain intermarket relationships. Specifically, gold-to-stocks and bonds-to-stocks in an expanding economic environment (yes, this was one of last week’s topics as well). In essence, if the economy is indeed strengthening gold (unless we’re seeing/expecting rampant inflation) and bonds ought to be weakening. But they’re not: click to enlarge…

As for gold, the present confusion has to do with what we believe is presently driving its price action. Which is the prospects, or lack thereof, for higher interest rates and a higher U.S. dollar. Specifically, gold traders’ skepticism about the state of the economy and the resolve of the Federal Open Market Committee.

As for bonds, basically ditto. Although bonds are doubly perplexing in that anything passing Congress — like tax reform or infrastructure — will result in a higher U.S. budget deficit (at least initially) and, thus, a greater supply of treasury debt that’ll need to attract buyers (read higher interest rates). There is of course the counter-argument that says that the Fed raising rates will serve as a weight on the economy that’ll ultimately bring on the next recession and, therefore, folks should indeed be buying the long-end of the curve (longer-term bonds). We can go there later, but for now suffice it say that, at this stage of the tightening cycle, we think that would be jumping the gun a bit.

We should add that, in both cases, there’s a high likelihood that there also exists a priced-in premium for political risk; if, say, for example, tax reform fails.

Well, while sure, we expect some long-overdue volatility would result from such failure, the overall bullish setup that we’ve been discussing herein since before last year’s election, since before any real talk of legitimate tax reform, remains very much intact. Historically-speaking (acknowledging that anything can happen), we’d need to see a marked breakdown in our data — as opposed to a breakdown in political talks — before we fret a looming bear market.

So, again — while we’re not suggesting that they’re presently out-gaining stock traders (not nearly!) — gold and bond traders are hanging in, amid a macro environment that, we think, makes their present positioning an unusually risky intermediate/longer-term proposition.

So why our adage “bull markets climb a wall of confusion”? Well, substantial capital flowing to defensive assets while the weight of the evidence leans in favor of higher equity prices, means everyone is not crowded on the equity side of the boat (which would ultimately be your “die on euphoria” scenario). And that’s a good thing!

In closing, here’s a repeat word on volatility.

We think we need to be bracing you a bit for the inevitable, so, in case you had better things to do last week than read our weekly message (but how could that be?), here’s what we had to say on the topic:

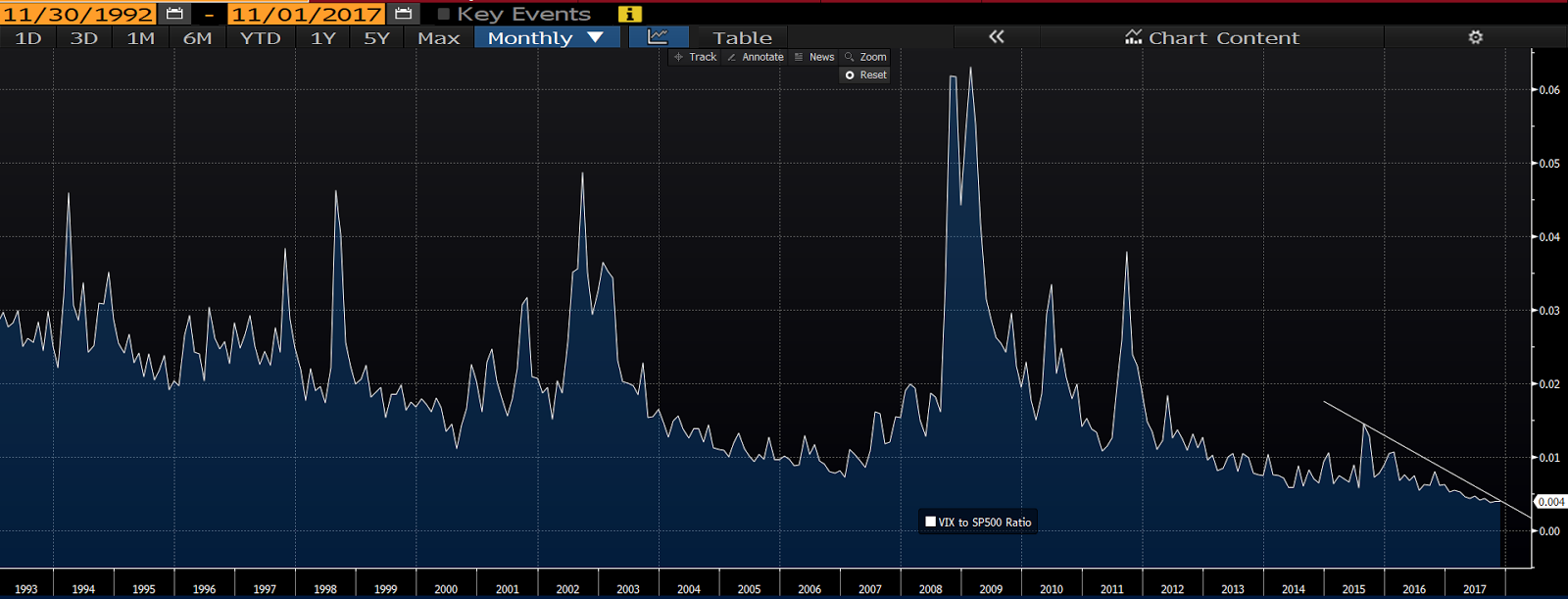

Lastly, you may have noticed that many of our recent Quotes of the Day have focused on investor psychology; specifically, the mistakes most investors make. Reason being, we think it’s of paramount importance that we remind our clients of the reality of financial markets — particularly given the fact that the recent stretch has been one of the least volatile on record. You see, another intermarket relationship worth monitoring would be the one between the S&P 500 Index and the CBOE Volatility Index (VIX).

Here’s an historical look at the VIX-to-S&P 500 ratio: click to enlarge…

While the present setup suggests that volatility should (like gold and bonds) indeed underperform, we think this is a bit much, and we’re concerned that recency bias may infect our clients’ thinking. I.e., when one becomes accustomed to a certain something, particularly a pleasant certain something, one can feel an intense sense of shock when that certain something morphs into a certain something else. Bottom line, the present certain something — historically low volatility — doesn’t jibe with market history, even bull market history. So, don’t be too dismayed when volatility picks up a bit, it’s actually the norm.

Have a great weekend!

Marty