In this week’s weekly message we noted that our economic assessment isn’t screaming inflation, but it’s indeed suggesting that the Fed would be well advised to continue to ease up on the gas pedal (nudge rates higher while reducing its balance sheet) going forward.

This morning’s data releases support that notion.

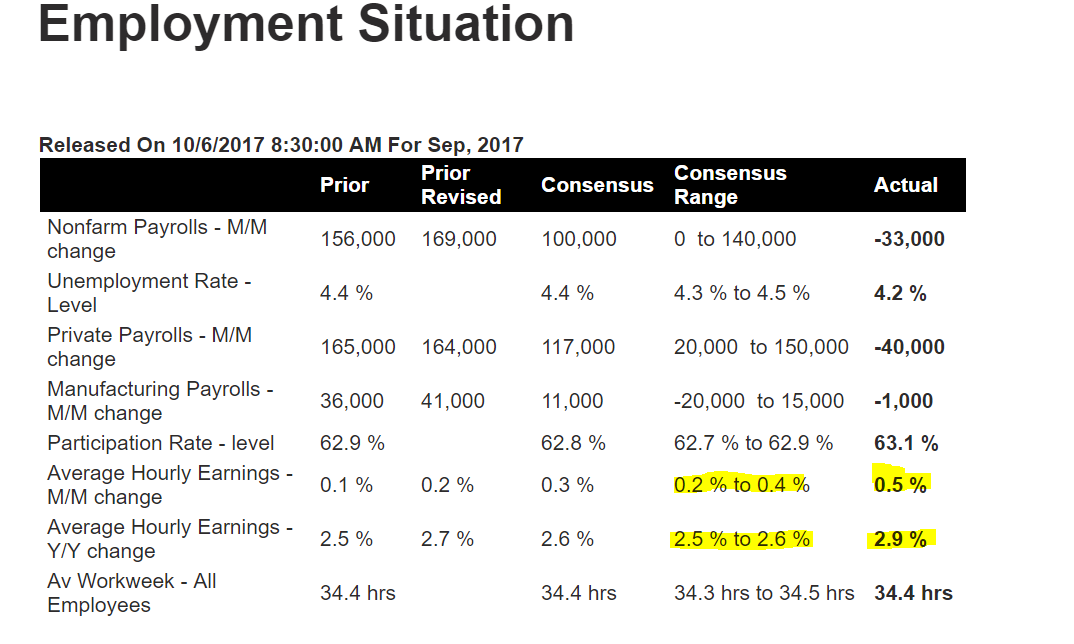

While the September jobs report shows a loss of 33,000, we expect a revised number when the BLS gets the hurricane numbers all squared up. Plus there’ll be the inevitable, and equally non-representative, snapback in the coming months. Looking through the report, however, the tight labor market is indeed showing up in the wage numbers — as should be expected: click to enlarge…

Bloomberg makes our point: emphasis mine…

The hurricanes are one factor that may or may not have skewed payrolls sharply lower, and probably did, but it’s the wage pressures that will make everyone on the FOMC, even the most dovish, suddenly concerned that wage-push inflation has arisen from the dead. The Department of Labor hasn’t offered adequate explanations of these results which puts the focus on individual Fedspeak with the chances of a rate hike at the month-end meeting, let alone the December meeting, now likely in play.

This morning’s other release, Wholesale Trade, adds fuel to the argument. Per Bloomberg:

If overheating is suddenly an issue for the economy, as it may be given the spike in average hourly earnings in this morning’s employment report, then wholesale trade data offer confirmation. Inventories in the sector surged 0.9 percent in August following July and June’s already outsized surges of 0.6 percent each. Sales in the sector are even stronger, up 1.7 percent in August which, despite the jump inventories, pulls the stock-to-sales ratio down one notch to 1.28. Strength in autos is a major factor boosting the data though ex-auto data also show unusual strength, up 0.8 percent for inventories and 1.5 percent for sales.