Hedge fund legend Julian Robertson fears a forming bubble in the stock market:

“The market as a whole is quite high on a historical basis,” he said. “I think that’s due to the fact that interest rates are so low. But there’s no real competition for the money other than art and real estate.”

“I think we need interest rates to appreciate, to go up, because I think we are creating a bubble,” he added.

Well, yeah, “on a historical basis” the market’s higher than it’s ever been (although valuations are far from the lofty levels of the late 90s [à la the Robertson characterization below]). So, I guess either stock prices have indeed been pushed beyond reason into bubble territory, or the prevailing data, or improved prospects, or pent up demand, or all three, are fundamentally driving the market beyond where it’s ever been.

In any event, an all-time high level, by itself, is anything but a reason to sell, or sufficient evidence that stocks are pushing on the edges of a bubble.

As for Mr. Robertson, I wasn’t kidding when I said “hedge fund legend.” His story, and the story of the rise of his Tiger Asset Management is chronicled beautifully in Sebastian Mallaby’s More Money Than God: Hedge Funds and the Making of a New Elite. The thing is, while he was (may still be) an adept stock picker, he was not (I’m guessing still isn’t) — per the excerpt below — your gifted macro analyst:

The trouble was that Robertson was not equipped to thrive as a macro trader. Jim Chanos, the short seller who worked with both Soros and Robertson, vouched for Robertson’s superior grasp of stocks; but no macro trader would have said the same about Robertson’s grasp of interest rates or currencies.

Anyways, in our view, you can’t credibly go throwing bubble predictions around with nothing more than low interest rates and all-time highs to make your case. You have to locate excessive stress in the system.

In the article linked in our first sentence above, the author states:

Robertson is perhaps best known for predicting the tech bubble in the late 1990s.

Perfect! Now we have some history to consider.

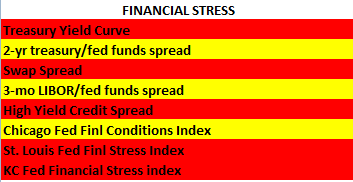

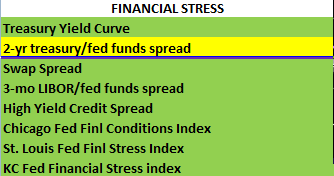

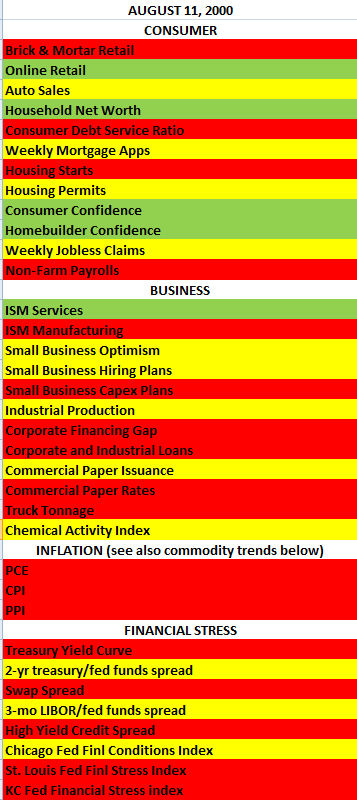

We’ve been back-testing both the technical and macro analyses we perform weekly here at PWA. In that the term “bubble” suggests that there’s serious stress in the system, let’s see what 8 of the financial stress indicators we track (the ones we have sufficient historical data on) looked like (per our color coding) in mid-2000, as the tech bubble was about to burst:

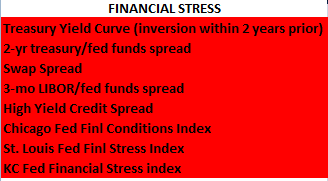

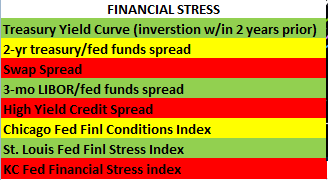

click any insert to enlarge…

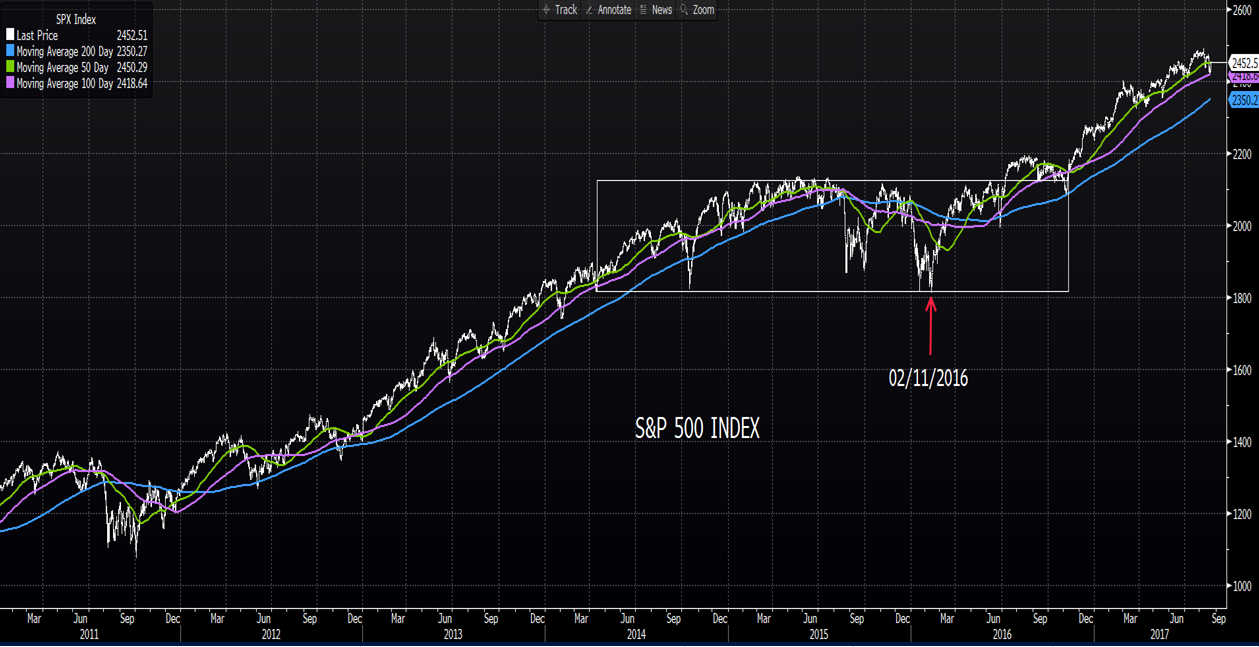

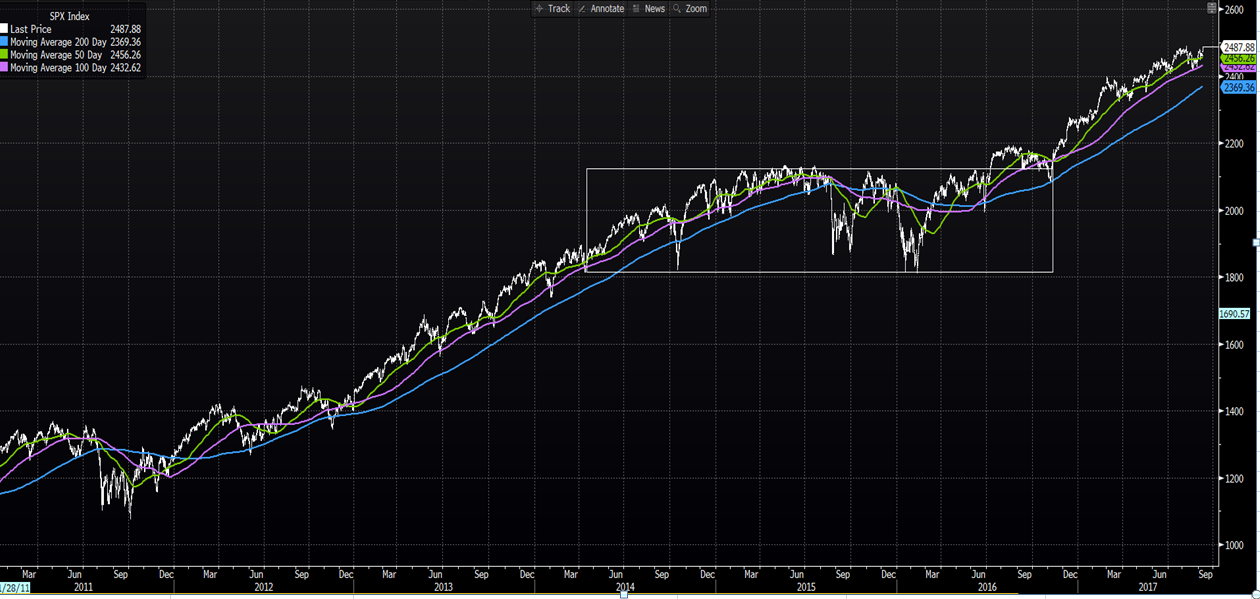

And here’s the accompanying chart (see red arrow):

So, absolutely, if Mr. Robertson was making the bubble case back then, he was right on the money!

Haven’t heard whether or not he predicted the 2008 mess (that next plunge on the chart), we’ll assume not, or it surely would’ve been mentioned in the article. But let’s go ahead and see how our stress indicators were fairing back then.

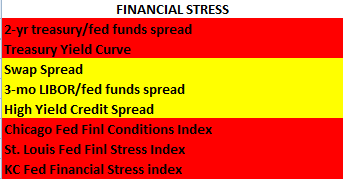

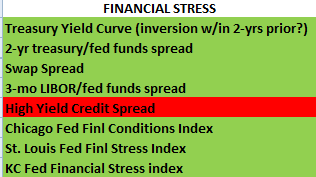

Here’s October 2007:

Getting scary!

Here’s the chart:

No question, the mounting pressure from the past two bubbles was showing up vividly in our financial stress indicators as the stock market was peaking.

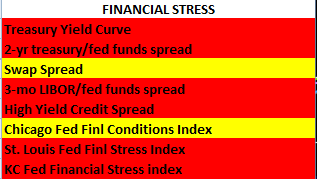

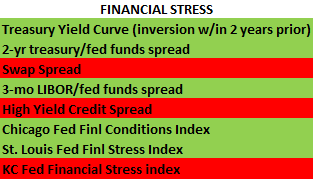

Here they are on the dates (red arrow on each chart) we’ve tested from the tech bubble on (not repeating the ones above):

9/21/2001 (while the tech wreck was still underway)

3/31/2003 (the tech bear market bottom)

7/14/2006 (2 years before next bull market end)

03/31/2008 (5 months before market freefall)

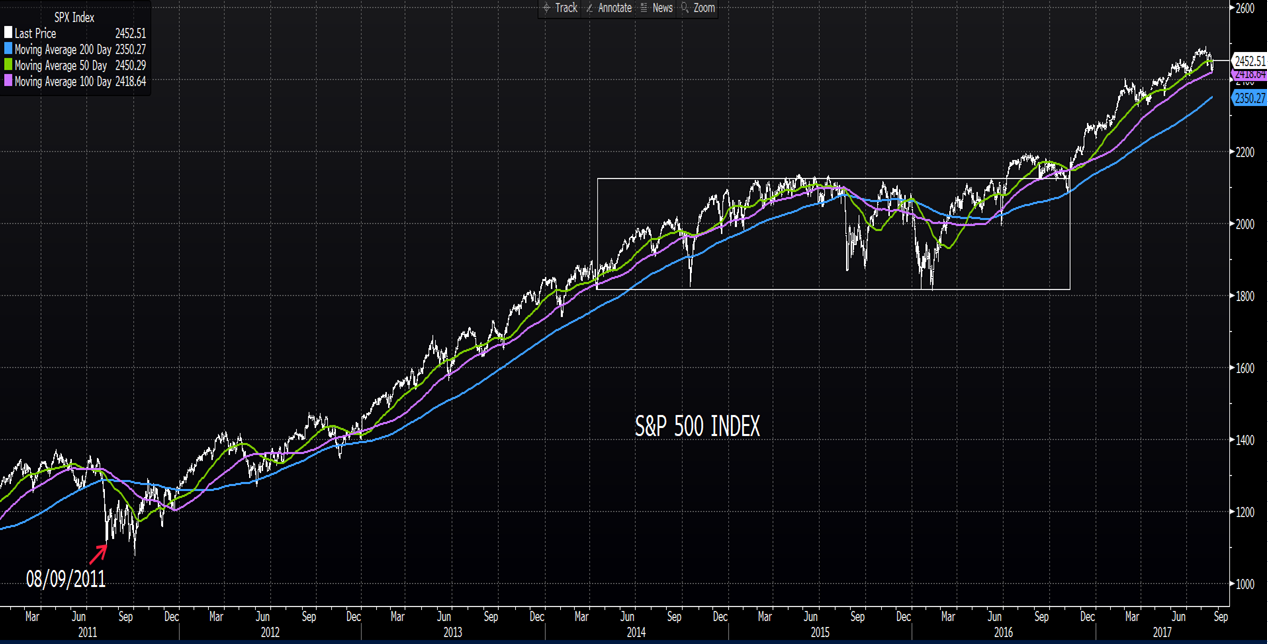

8/09/2011 (first 10+% correction after 2008 bear market, but no new bear market)

11/16/2012 (notable market dip, but no bear market)

08/24/2015 (first 10+% correction since 2011, but no bear market)

2/11/2016 (worst start to a year in history, but no bear market)

Monday of this week

As we can conclude from the above, it’s likely (not guaranteed mind you) that there’ll be warning signs in the macro data ahead of the next great bear market. And, presently, virtually no such signs (at least not in these financial stress indicators) exist.

So what had Mr. Robertson getting it so right ahead of the tech bubble? Clearly, it wasn’t the financial stress data. I mean, if it was, he’d be resoundingly bullish right about now, not bearish (which he is).

Well, alas, we should seldom, if ever, take the media at its word. Again, the author stated:

Robertson is perhaps best known for predicting the tech bubble in the late 1990s.

Truth be told, Mr. Robertson was early on his predicting the late 1990s tech bubble. Disastrously early!

Henry Blodget, in his article titled Why Wall Street Always Blows It tells the sad story of an excellent stock picker whose past success robbed him of the humility that I suspect kept his feet under him while he racked up a phenomenal stock-picking track record:

For almost two decades, Robertson’s Tiger Management had racked up annual gains of about 30 percent by, as he put it, buying the best stocks and shorting the worst. (One of the worst, in Robertson’s opinion, was Amazon, and he used to summon me to his office and demand to know why everyone else kept buying it.)

By 1998, Robertson was short Amazon and other tech stocks, and by 2000, after the NASDAQ had jumped an astounding 86 percent the previous year, Robertson’s business and reputation had been mauled. Thanks to poor performance and investor withdrawals, Tiger’s assets under management had collapsed from about $20billion to about $6billion, and the firm’s revenues had collapsed as well. Robertson refused to change his stance, however, and in the spring of 2000, he threw in the towel: he closed Tiger’s doors and began returning what was left of his investors’ money.

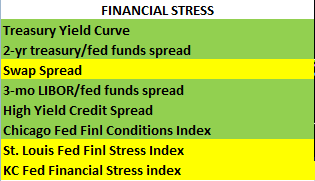

Unbelievable! The spring of 2000 (literally the moment when the market would’ve begun turning his previously unwavering stance into one of greatest investment success stories of all time) is when Robertson cashed out his investors and closed Tiger’s doors to outside money. Here again is that chart featuring March 2000:

In the end, all we can truly say is that Julian Robertson got excited merely over record high stock prices. At the time, the bubble-burst that he supposedly predicted was years (at least 2 [don’t know when he began shorting tech stocks]) away. And while the financial stress indicators featured herein were showing some strain, other economic data suggested that the next recession was still a ways off.

Here’s a look at more of the data we track, along with the stress indicators, as of October 8, 1998 (as Robertson was making big bearish bets):

Here’s what that larger picture looked like 2 years later, heading into the tech bubble implosion:

If Mr. Robertson had a grasp of the macro, he would’ve in all likelihood put off his shorting campaign until he had more than a hunch to go on. In which case, this week’s headline would’ve read:

Robertson is perhaps best known for predicting the tech bubble in the late 1990s, and making billions as a result.

I find it ironic, and, frankly, deceptive, that a journalist would have today’s reader pay heed to the warnings of a man based on a prediction that ultimately had him blowing up his own multi-billion dollar hedge fund. Now, if Mr. Robertson has an individual stock tip to offer, I’m all ears!

In closing, we want to be sure and stress that markets are inherently unpredictable, especially in the short-run. Things forever change and there’s no guarantee that a set of indicators that “worked” in the past will work as well in the present. The best we can do is collect and interpret what we believe to be the most pertinent data, remain open to all possibilities, and base our investment decisions accordingly.

We’ll keep you posted…

Have a nice weekend!

Marty

P.s. Here’s me, in August of last year, picking on a couple of popular doomsayers. Perhaps someday they’ll be famous for (among other things, in one case) predicting the great bear market of ????. Apparently, per our commentary above, one can be way off the mark and still get the credit… (as you watch, remember, we produced this over a year ago)…