In this week’s message we’re going to jump around a bit.

For starters, I received inquiries pre and post yesterday’s Fed announcement. Here was my response to a client who asked about how I saw the Fed meeting playing out and how it would impact gold and stocks specifically:

The consensus is that the Fed won’t move on rates this meeting (odds have increased for December), and will announce that they’ll cut the reinvestment of interest and principal payments from their existing portfolio (treasuries and mortgage backed securities) by around 10 billion per month. That anticipation (along with other supporting data), I suspect, is impacting the dollar and gold already (a tightening would be bullish for the dollar, bearish for gold). Stocks seem okay with those prospects in light of a generally positive setup overall (doesn’t mean there won’t be sentimental negative near-term reaction to the perception of Fed tightening). Historically-speaking, the Fed has a ways to go (in terms of tightening) to threaten the economy (and, thus, the equity market).

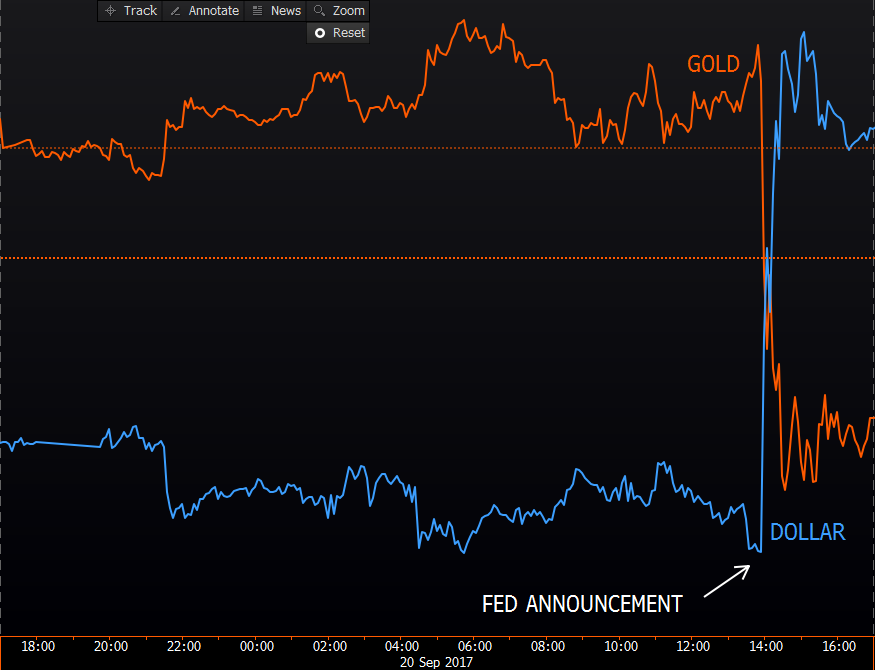

And the consensus was right on the money in terms of the extent of the rolloff and the absence of a rate hike. And the bullish dollar/bearish gold assumption was validated:

click to enlarge…

As for stocks, that dip on the news would be the sentimental near-term reaction I eluded to. And I wouldn’t necessarily consider the strong snapback into the close as the end of the story. I.e., while we remain constructive on U.S. stocks going forward, we’re way overdue for some healthy corrective action (read volatility):

Here’s my reply to a client who solicited my overall opinion on the markets in light of the Fed’s stated objectives and strategy going forward:

It’s going to be quite the task… The timing is about as good as it gets right now to get it started. They’re testing the water with 10 bill per month. While it’ll be interesting to see how fast market-driven rates rise going forward, at this stage of the cycle I believe we should expect essentially the same reaction (in equities, the dollar, gold, etc.) we’d see if it was a tightening via traditional measures (that is, just raising the policy rate). Basically, the rolling off the balance sheet inspires less aggressiveness on the fed funds rate… They’re in essence balancing the two and hoping not to create too much of a headwind for the economy..

While we’re overdue for some volatility, our research says we’re likely a ways from the next recession/bear market… and I don’t suspect the present Fed tightening stance will upset the applecart…