So what are we, as investors, to do amid all of the present turmoil? Let alone the stuff to come; like the looming debt ceiling debate, the ongoing Russia investigation, the U.S./South Korea military drills slated to begin next week, the German election, etc.??

Seriously, that’s some serious stuff to think about! But what else is going on out there? Well, as you may know, we keep a monthly current trends file. And, for whatever reason(s), August’s folder is already bulging with 96 entries. I.e., there’s lots of events/trends/data happening outside of politics.

Nope, I’m not going to cut and paste 96 titles below, but I will feature the first five, the middle five and the most recent five just to get the flavor of what’s happening beyond the disturbing headlines.

Here you go, in chronological order:

- Copper price and metals producers’ stocks speak to global economic optimism.

- Corporate lending in Japan at highest yoy growth on record. Singapore lending at record high.

- Australia business lending up, residential down.

- China’s official PMIs remain in expansion mode (particularly services), but range bound.

- Eurozone labor market looks very strong.

- Germany, and European equity markets in general, beginning to show some cracks.

- Earnings season looking very good.

- A look at past years resembling 2017 speaks optimistically about the remainder of the year.

- S&P 500 intraday action speaks bullishly about present state of the market.

- The Nasdaq’s intraday action less bullish that S&P’s, although not at all bearish.

- Multi-family housing fundamentals are waning, single-family fundamentals, however, remain strong.

- July Fed minutes strike a dovish tone.

- S&P 500 earnings are an unambiguous positive at this point.

- Breadth is looking a bit suspect of late.

The general tone above fairly well represents the overall picture painted by the 96 entries to our August trends file. I.e., while the data is mixed, we can say that it tilts positive, or, at least, that there’s virtually nothing going on in the world that screams a global recession lurks around the next bend.

Now, for a quick look at the charts.

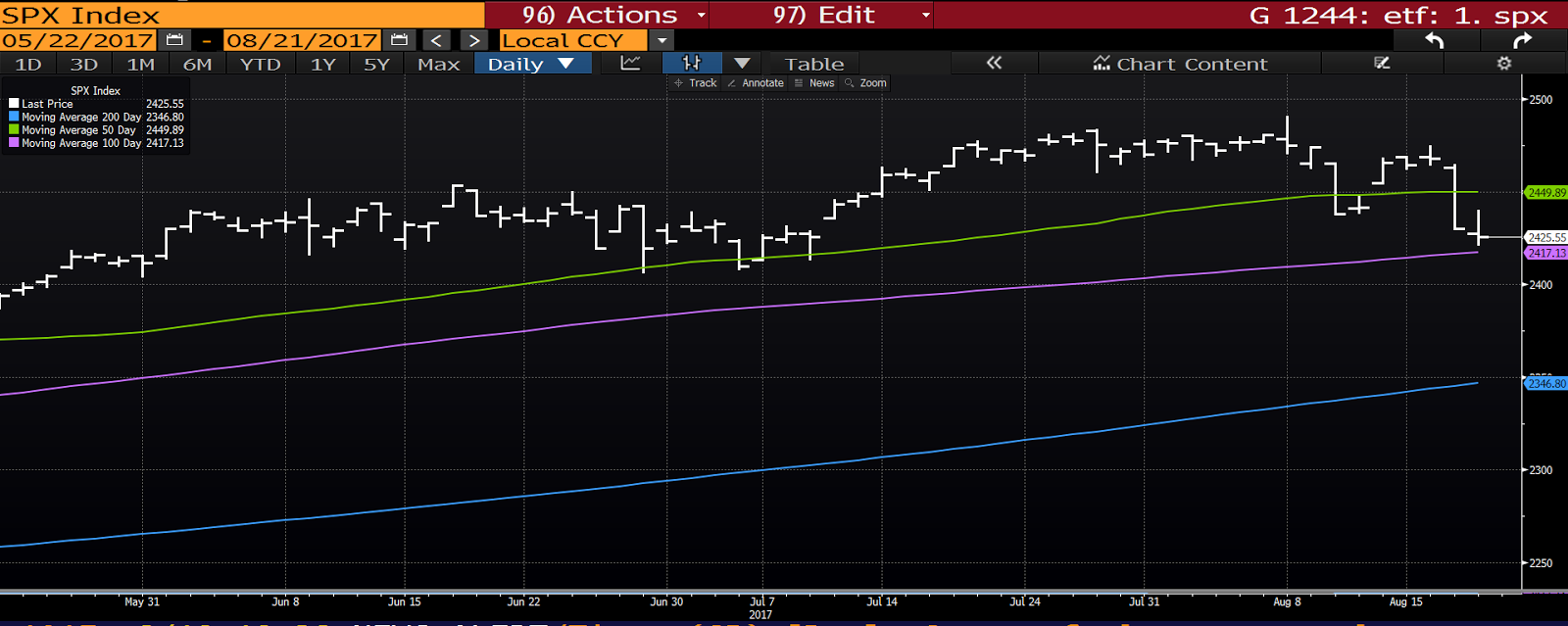

Here’s a 3-month look at the S&P 500 with its 50, 100 and 200-day moving averages:

click to enlarge…

As you can see, there’s definitely been a technical breakdown of late — with the price breaking below the 50-day moving average.

Question is, would this be volatility to ignore (inspiring us to stay the course with our sector allocations) or volatility to respect (inspiring perhaps a defensive tweak)?

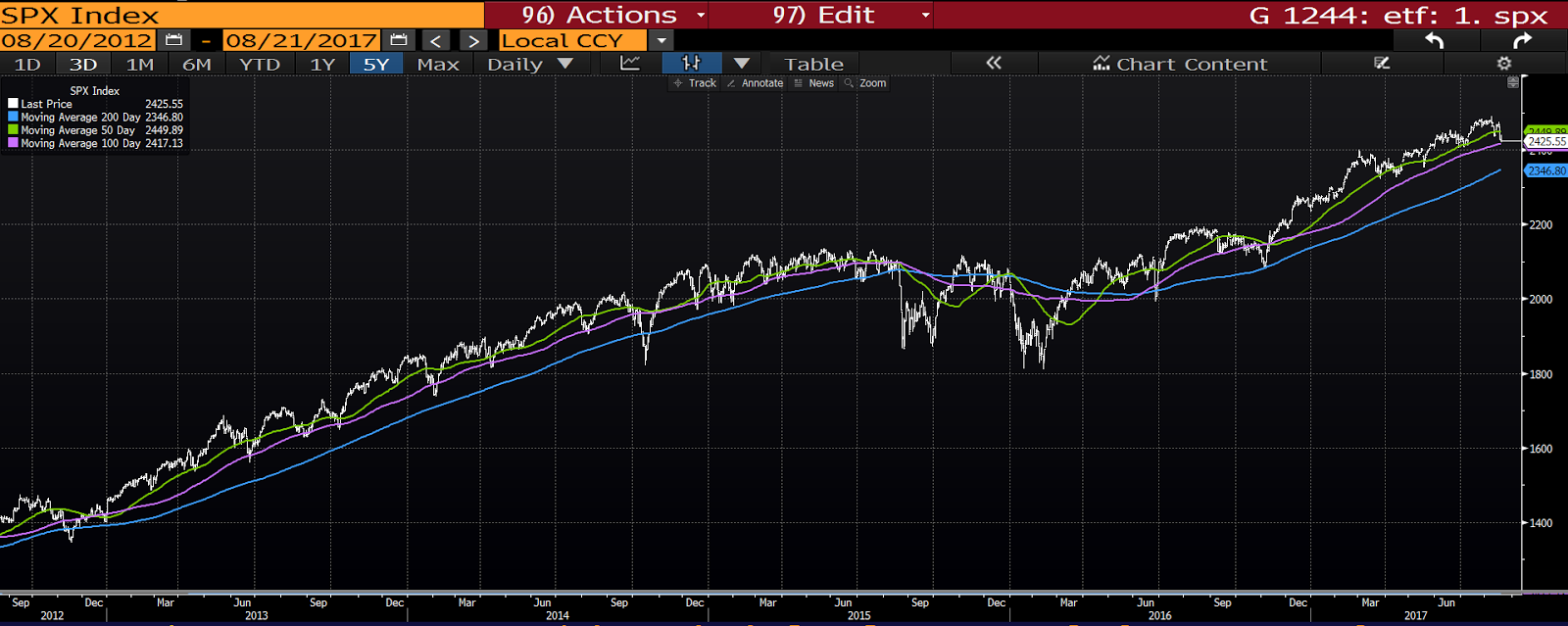

Well, take a look at a 5-year chart and ask yourself how advisable it would’ve been to react to all of the moving average breaches?

Ah, you say, but what about those back to back corrections occurring in the fall of ’15 and the beginning of ’16?

Well, I can answer that two ways:

1. Note that you accurately used the term “corrections”, as opposed to “bear markets”. Generally, long-term investors don’t fret corrections (less than 20% drawdowns), it’s the bear markets (drawn out drawdowns of more than 20%) that they’d like to mitigate if possible.

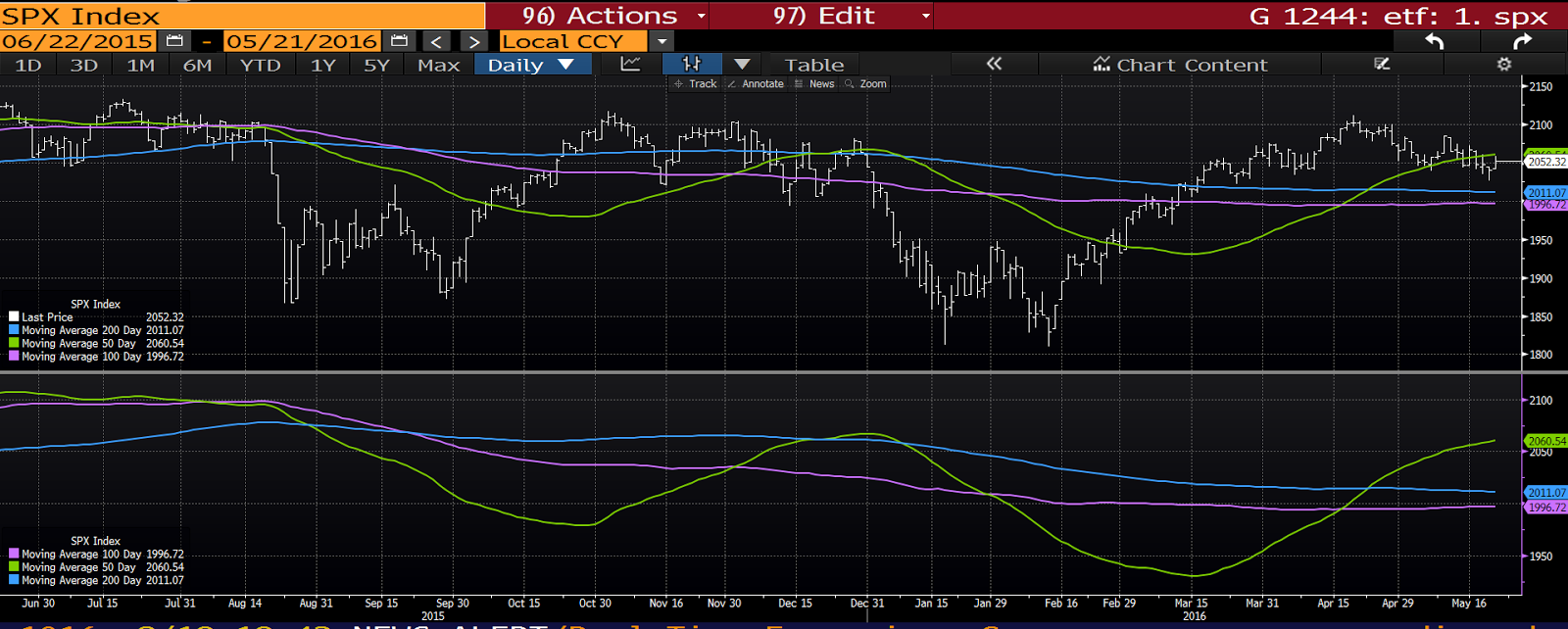

2. Note the positioning and slopes of the moving averages going into those drawdowns, versus all of the other times the price dropped below one or more them.

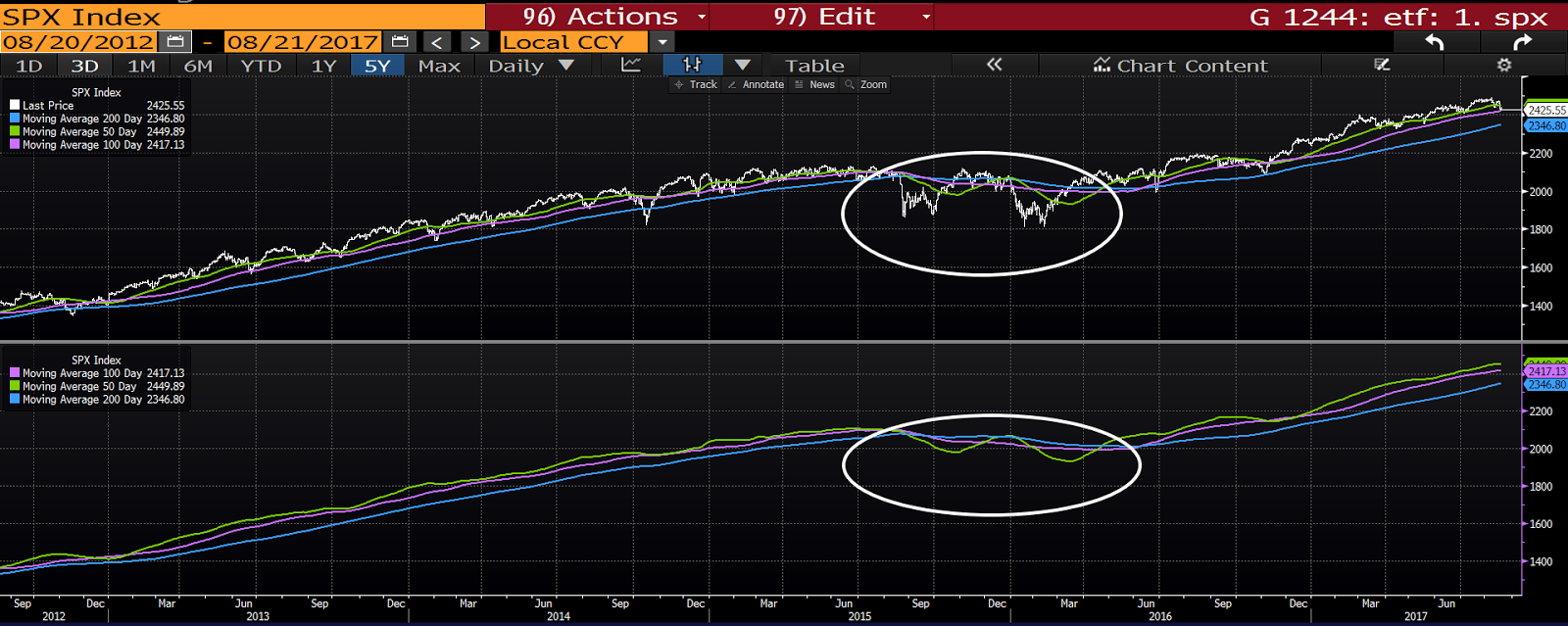

I’ll add a panel with just the moving averages to make it easier:

Easier still; here’s zeroing in on those back-to-back corrections:

So, if 10% corrections rattle your nerves, the current setup (first chart above) wouldn’t warrant much worry. I have to add that if 10% corrections rattle your nerves, and you’re heavily exposed to equities, you either need to rethink market reality or dramatically reduce your equity allocation: For (notwithstanding very recent history) they are typically annual events.

Speaking of setups, the fact that the above referenced corrections (with their concerning looking charts) didn’t morph into full-on bear markets speaks to the macroeconomic backdrop at the time. While it wasn’t as robust as today’s, our indicators were not signaling that a recession was in the offing. Typically, bear markets need recessions.

Bottom line: The charts — and the economic backdrop — for now suggest quite strongly that what we’re experiencing is simply normal volatility within the context of an ongoing bull market. Of course it’s all subject to change (it ultimately will) and we thus remain open to all possibilities.

Have a great weekend!

Marty