We can’t — while recognizing that, in markets, anything can happen at any time — overemphasize how derailing (something more than a ~20% correction) a bull market is really tough when it’s not in the mood for, well, derailing.

A la the late great Jesse Livermore:

“Not even a world war can keep the stock market from being a bull market when conditions are bullish, or a bear market when conditions are bearish. And all a man needs to know to make money is to appraise conditions.”

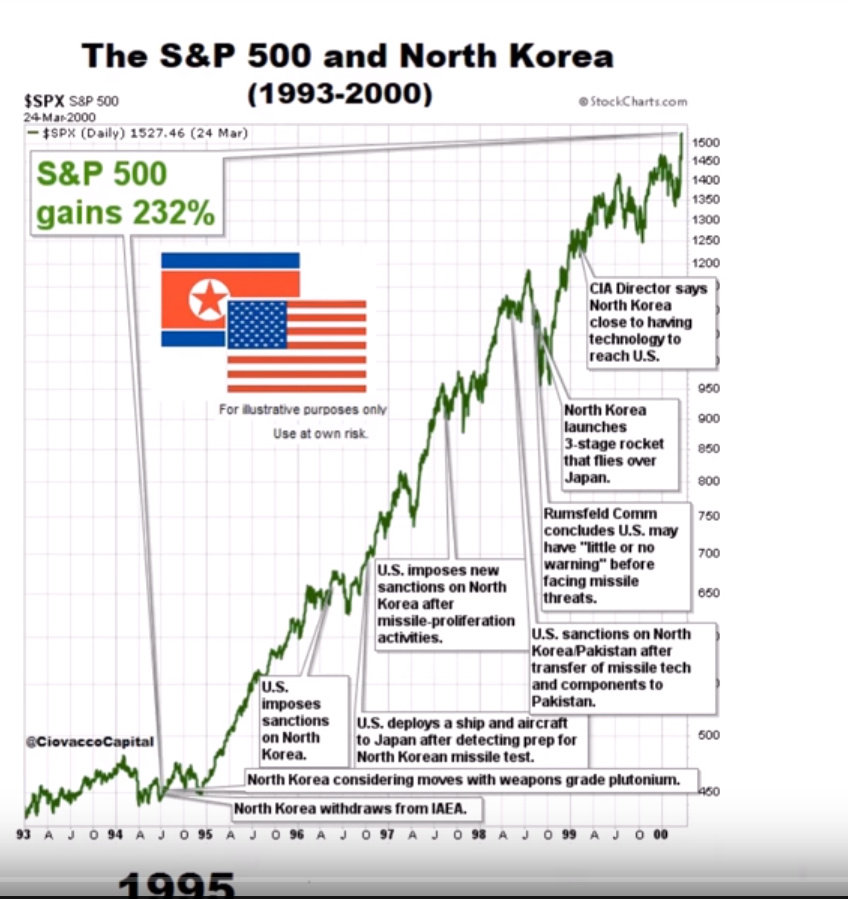

For example, in the fall of 1998, a then storied (and monster of a) hedge fund called “Long-Term Capital Management” (LTCM), run by the two Nobel laureate economists who, ironically, wrote the options pricing model we all use today, and who were, ironically!, huge proponents of modern portfolio theory (i.e., what happened to them — they theorized — had one in a bazillion odds), blew to pieces (as Russia, for example, defaulted on its debt). And, yep, among other things, North Korea flew a rocket over Japan (talk about icing on the cake!) — although, clearly, it was LTCM and an emerging market debt crisis that did the number on global markets. A number

that, to the surprise of many, didn’t derail the then bull market.

Here again is that chart of North Korea and the S&P 500 in the ’90s:

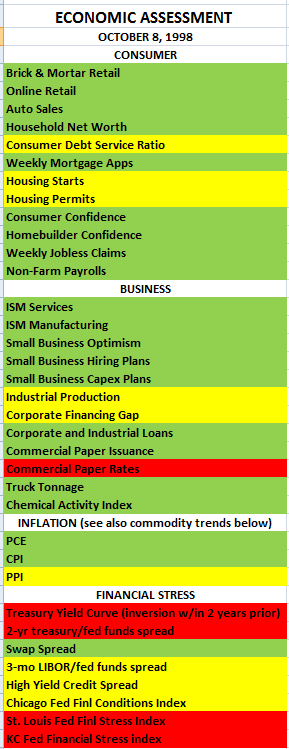

And here, from last week’s video (watch if you haven’t yet), is the economic backdrop in the fall of 1998:

Not perfect, but not ready to roll over. I.e., no bear market:

Not like two years later (and [S&P 500] 50% higher):

Now that’s an economic setup nearly begging for a bear market. Which it got:

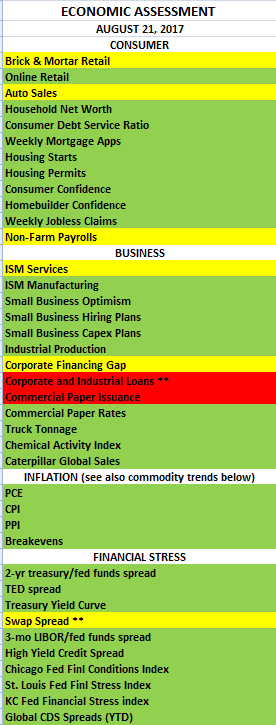

And, again, while anything can happen (I stress!) — and we remain open to all possibilities — the present economic backdrop is not screaming recession, or, therefore, bear market:

In last week’s video we — in the above style — visited several other moments in recent history…