Fed Chair Janet Yellen gave her 2-day semiannual report to Congress this week and offered up what you might say was a moderately optimistic view of the economy going forward. Like us, the Fed tracks an array of published economic data to gauge its view of general conditions.

The Fed’s overall assessment is what guides its monetary policy moves. Our overall assessment influences (technical data plays prominently into our view as well) the sector and regional weightings within our portfolios’ equity exposures, and — along with our technical market assessment — guides our approach to the fixed income allocation.

The market-relevant message from Ms. Yellen was that the Fed sees itself being soft on interest rate increases going forward while beginning to unwind its massive balance sheet (the t-bonds and mortgage backed securities it bought off of bank balance sheets during the last recession). Bond traders, heartened by the written release of what would be her dovish testimony, bid up prices on day one, then, disheartened by who knows what, sold off on day two:

While markets can and will defy the charts (particularly in the short run), the following is a bearish-trending graph that suggests to me that traders will likely be selling into the bond rallies (as they did on day 2) for the foreseeable future:

So, again, the Fed’s feeling just okay about the economy going forward. And they should know, right? I mean the economy is about people, and how they spend their money. And the Fed has its finger on the pulse because…….., because…….., well, I honestly don’t know how the Fed can truly feel the marketplace’s pulse???

I mean, the Fed governors and staff are off the charts intelligent, but they don’t sell stuff to consumers, they don’t mingle with customers, they don’t compete for business. Shouldn’t we, therefore, get a little closer to the ground when we’re efforting to take the economy’s temperature? And how can we do that?

Well, the folks at the Institute for Supply Management can help. Every month they survey hundreds of purchasing managers across both the manufacturing and service sectors and ask them a slew of direct questions. Then they score the answers and index the results. In our view, those monthly purchasing manager surveys are among the very best gauges of the overall health of the economy.

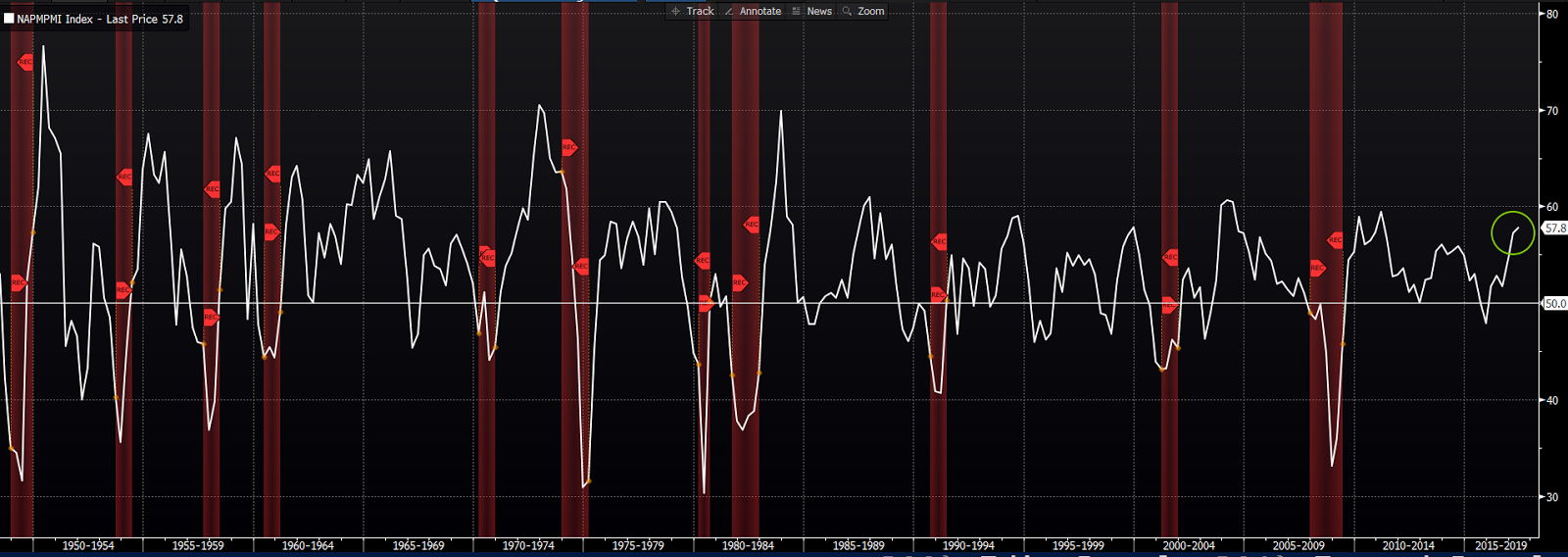

Here’s a 70-yr graph (yep, they’ve been doing this a very long time) of the manufacturing survey (red shaded areas are recessions). Above 50 (white horizontal line) denotes expansion, under 50 means look out below!:

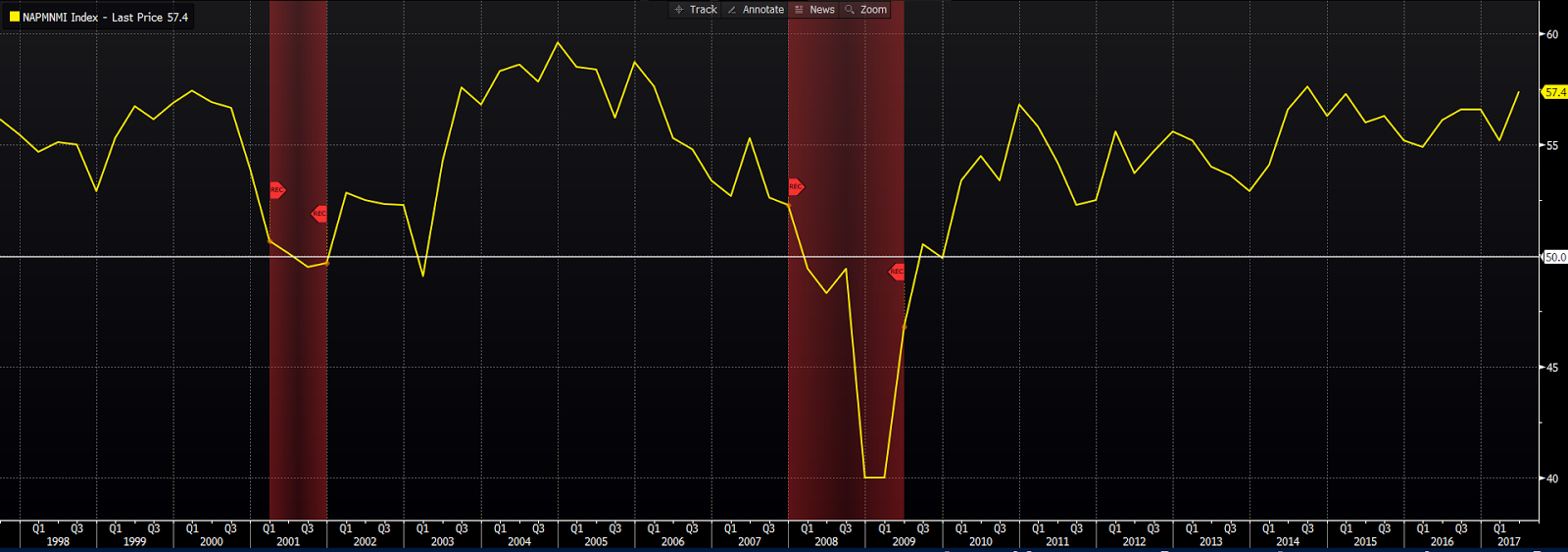

Here are the results of the much younger services sector survey:

Note how — while not every decline led to recession — every recession was preceded by a decline. And of course that makes sense, given the intimate relationship between the economy and private industry’s purchasing managers.

Of course it’s fine to update a chart once a month and check the expanding or contracting box, but it’s even better to dig into the details to get a more nuanced view of what’s happening under the surface.

With that in mind, here are the ISM’s highlights of the sentiment they gleaned from their most recent surveys:

Comments from the June ISM Manufacturing Survey: emphasis mine

WHAT RESPONDENTS ARE SAYING …

“Overall, business is strong. We are seeing price increases for packaging and handling materials as well as some MRO supplies” (Plastics & Rubber Products)

“Overall, demand is up 5-7 percent and expected to continue through the end of the year, at least. ” (Transportation Equipment)

“Demand is picking up; meeting budget expectations.” (Electrical Equipment, Appliances & Components)

“Business is still very robust. Have continued to hire to match increased demand.” (Computer & Electronic Products)

“Business [is] steady; not great, but good and fairly solid.” (Furniture & Related Products)

“Business globally continues to show improvement.” (Chemical Products)

“Environmental regulations have strong effects on our business. We continue to watch for any changes as a result of the new administration.” (Paper Products)

“Dry weather helping demand.” (Nonmetallic Mineral Products)

“International business outside North America on the upswing.” (Machinery)

“Metal pricing continues to drag down our profit margins, but we are very busy quoting new business, so our customers have a good outlook on the rest of the year.” (Fabricated Metal Products)

“Business is strong both domestically and internationally. Supplier deliveries are quick domestically, international supply chain is slowing. We are in a hiring mode.” (Food, Beverage & Tobacco Products)

And here’s from June’s Services Survey:

WHAT RESPONDENTS ARE SAYING …

“Labor continues to be constrained in the construction industry, driving cost increases. Regional unemployment rate of 2.7 percent is making hiring difficult on all phases of the construction supply chain.” (Construction)

“Off to a very strong start — 2017 YTD results above 2016 actual and 2017 target. Expect trend to continue. Very positive outlook for our business.” (Finance & Insurance)

“We continue to struggle with the unknowns surrounding Obamacare, whether it will be repealed, or replaced, and if replaced what does it mean for our health services business, as well as our health plans business.” (Health Care & Social Assistance)

“Activity level continues to climb in the oil and gas sector with supply in certain spend categories continuing to tighten.” (Mining)

“June has been quite a busy month in terms of internal food activity. Seasonal increases in beef and poultry overall. Produce has remained steady with some early summer items coming down in price as product moves from Mexico to California growing regions. Dairy slightly up due to summer season cream production increase.” (Accommodation & Food Services)

“General overall optimism in economy. Still job growth issues with mismatch in available labor pool and jobs available.” (Professional, Scientific & Technical Services)

“Activity is increasing due to full budget appropriations.” (Public Administration)

“Overall business is trending up and we have a positive outlook for 2017.” (Retail Trade)

“Several positive signals as we approach [the] third quarter.” (Wholesale Trade)

Bottom line: Private sector movers and shakers are, on balance, feeling good about the economy’s prospects. I.e., recession is not in the least something to sweat at this point, and, therefore, beware the bond market going forward.

Have a great weekend!

Marty