In last week’s message I shared an email conversation where I suggested that despite present yield spreads denoting a low financial risk environment (essentially paving the road to higher interest rates), folks were nonetheless willing to buy bonds. Here’s that part:

And while various yield and CDS spreads (let me know if you need specifics), in particular, are not showing heightened stress (denoting a low financial risk environment) bond prices are still catching a bid. The contradiction there is that, for example, CDS players are the definition of careful (and they’re smart) — yet they’re presently quite sanguine (i.e., they appear to be buying into the stock market rally).

Ironically, yesterday, Fed Chair Janet Yellen implied that present financial conditions (read spreads and a weak dollar) essentially give them a green light to hike their benchmark rate.

Per Bespoke:

Yellen also noted that while the FOMC doesn’t target financial conditions (looser today than the were when the hiking cycle began), they are a significant input to their thinking; that implies that low credit spreads and a weak dollar will be viewed as giving the FOMC room for more hikes.

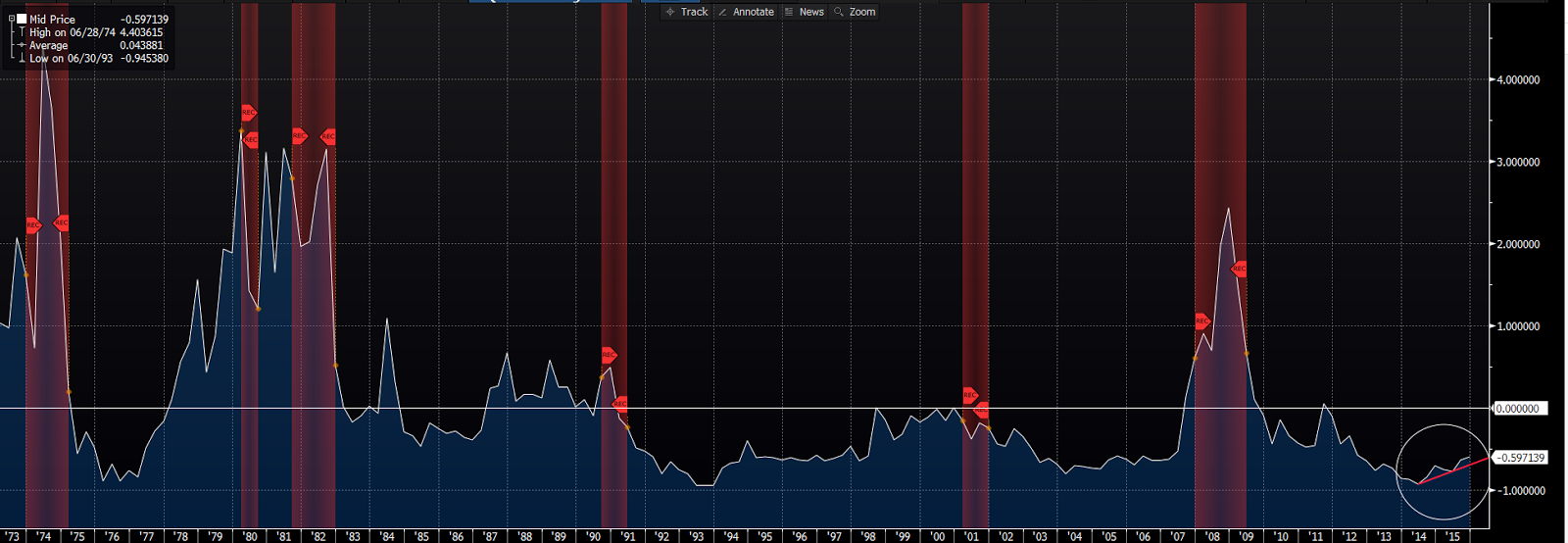

My observation is that “significant” is nearly an understatement of how critical “financial conditions” are in today’s Fed’s decision-making process. And while the aggregate financial stress/conditions indexes we track, save for one, haven’t approached danger territory since early in the expansion, they were trending in the wrong direction (per my trend lines below [up is bad]) during a period where many an expert thought the Fed should start getting the economy off the juice.

Here’s a look at the Chicago Fed’s Financial Conditions Index through the end of 2015 (the red shaded areas highlight past recessions). click charts to enlarge…

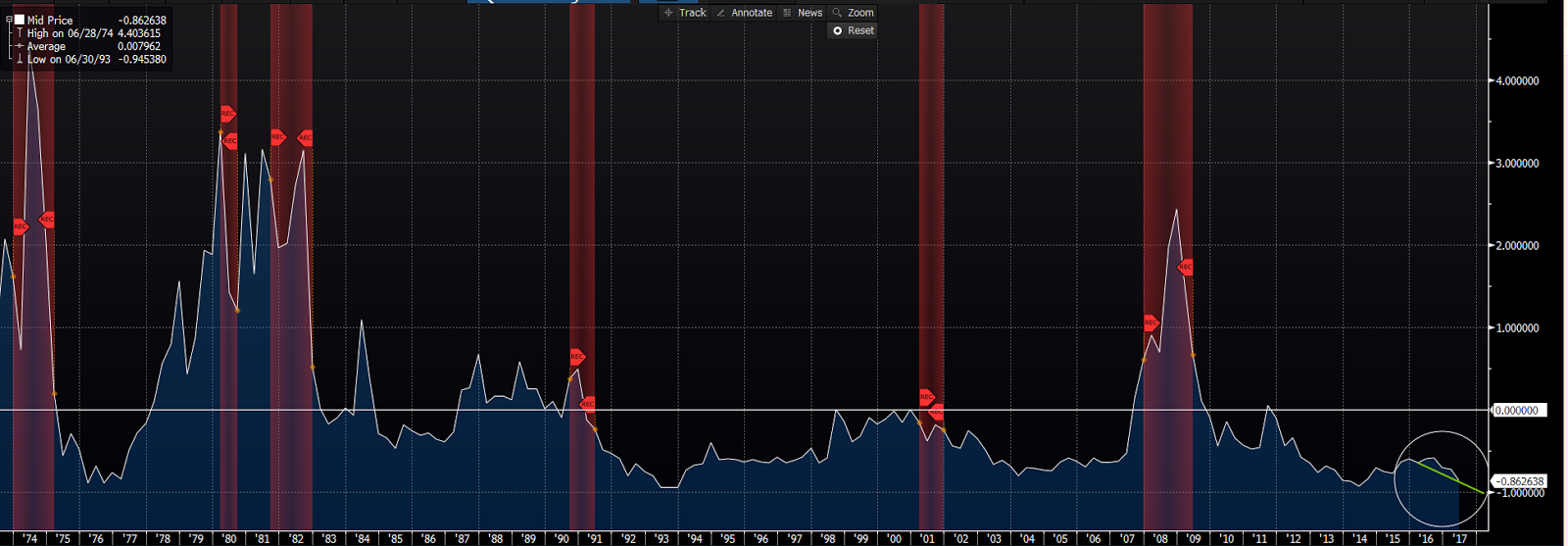

Here’s a look at it now:

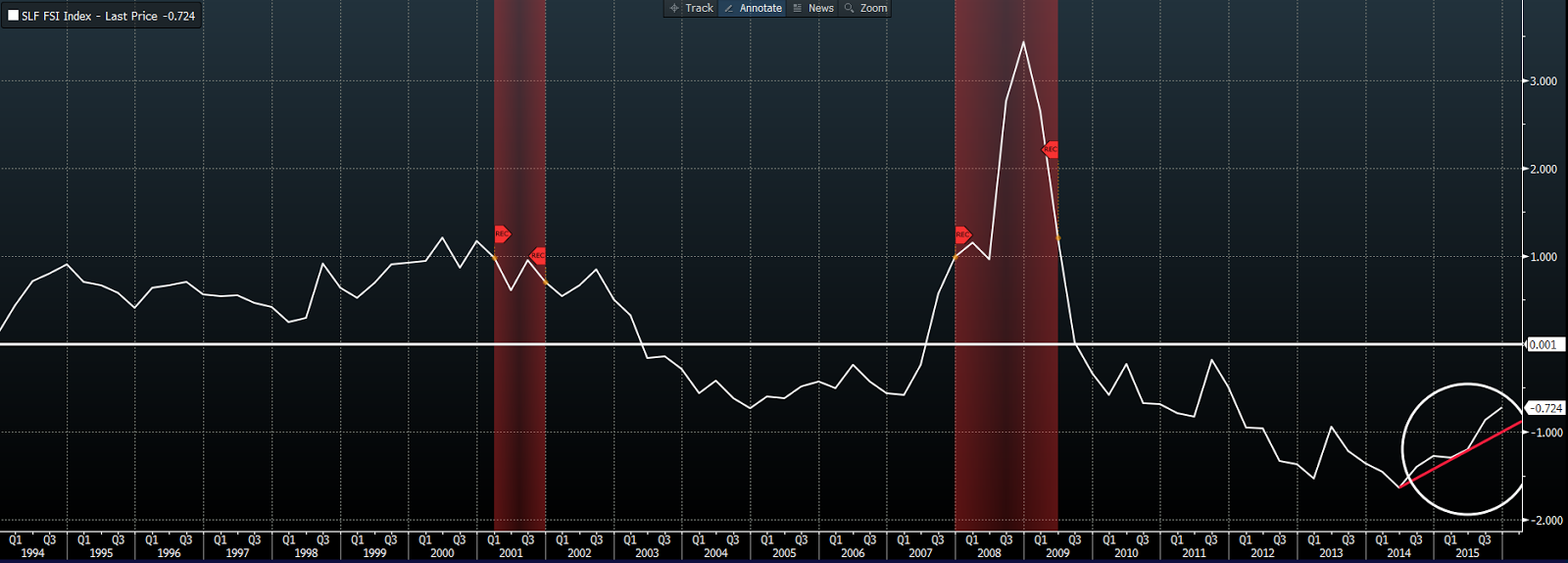

Here’s the St. Louis Fed Financial Stress Index through 2015:

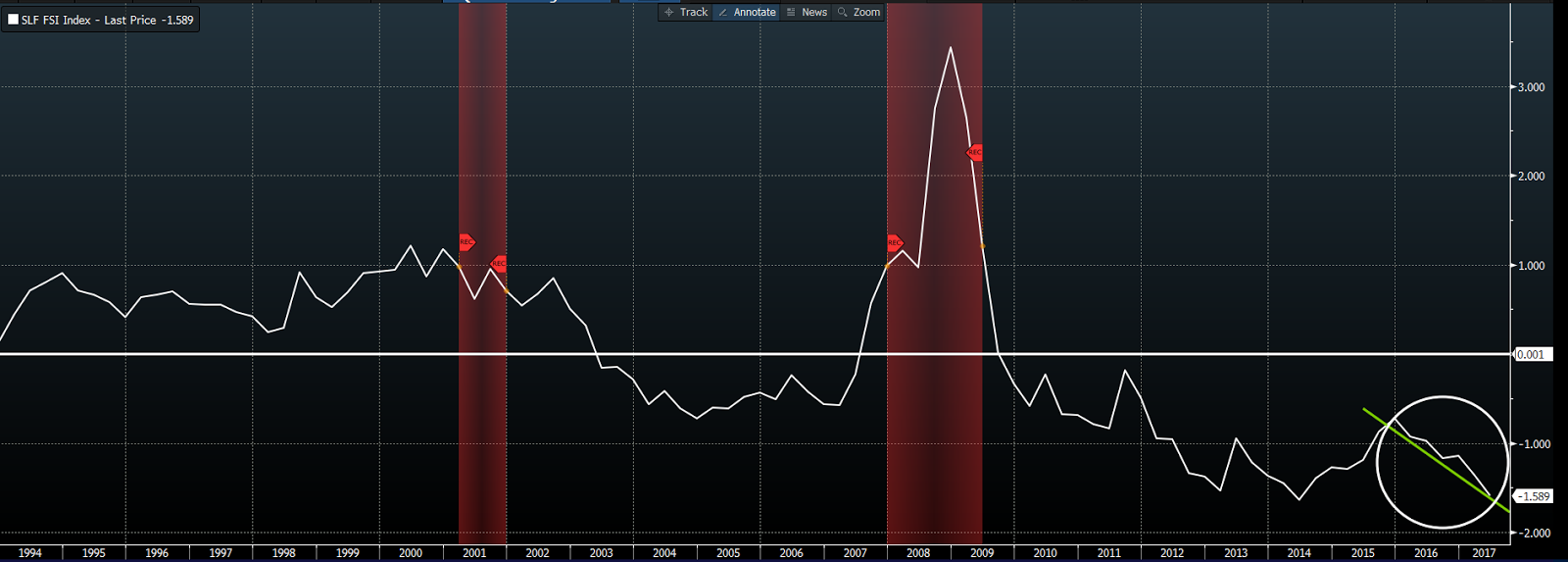

Here it is now:

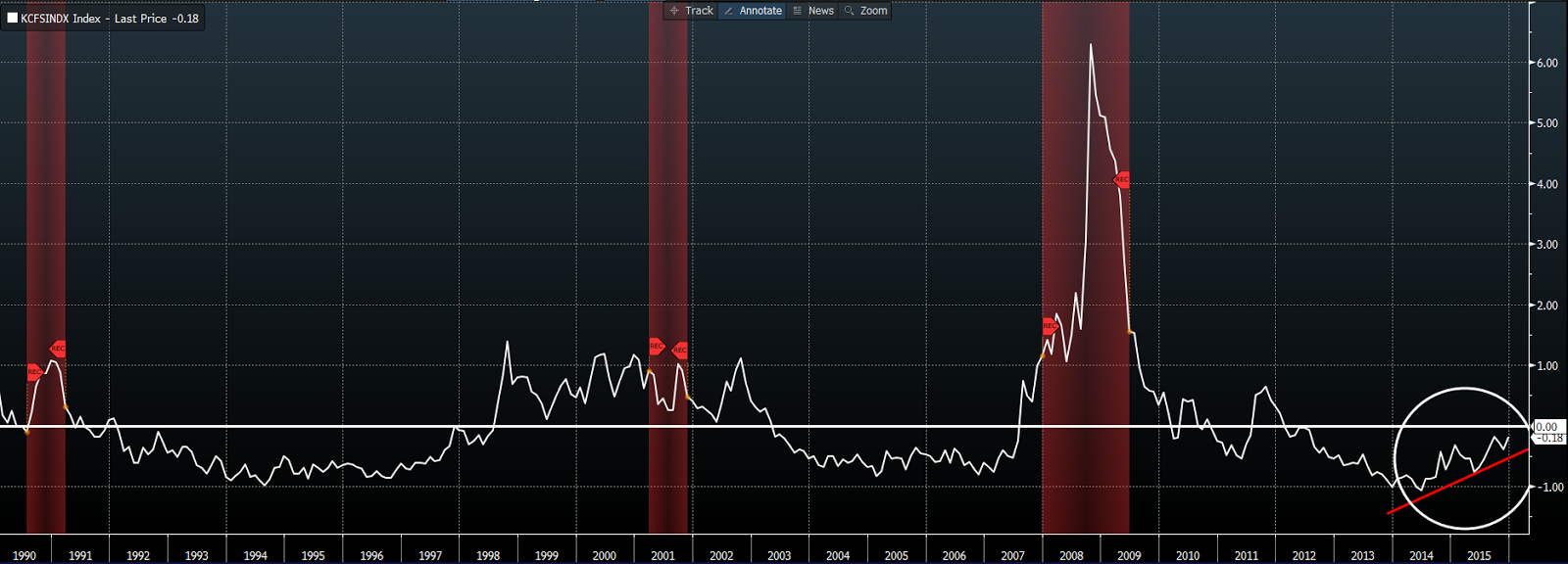

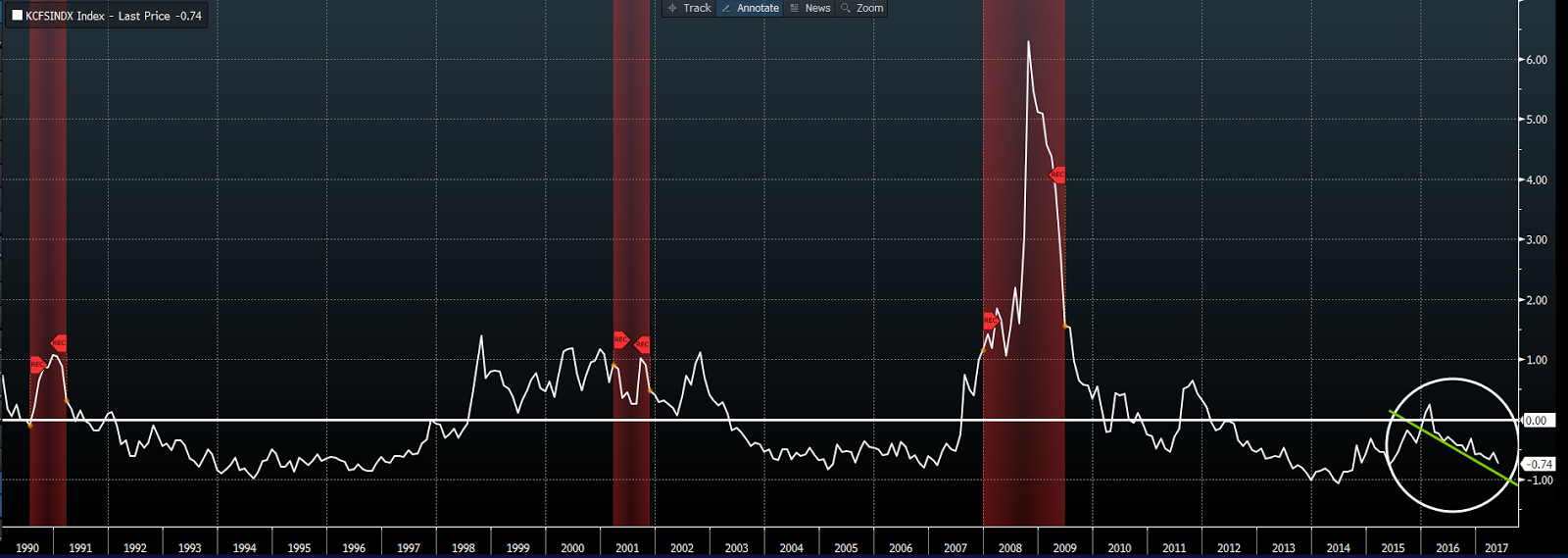

The Kansas City Fed’s U.S. Financial Stress Index through 2015:

Now:

So, as you can see in the up-to-date charts, overall financial conditions have been trending in a manner that allows the Fed to get busier building a little amo for the inevitable next recession. I.e., the time to do that is when — like lately — the inevitable is essentially off the radar.

So how’s the stock market to react to this newfound Fed confidence? Well, while a lack of financial stress is unambiguously good news, it doesn’t mean the stock market has to like it. Traders will have to recalibrate their thinking to a less accommodative Fed, which, at a minimum, lends itself to a noticeable pickup in volatility (the world over) — which has been disturbingly low (yes “disturbingly”, as in not normal) for quite some time.

And what about bonds? While yields have ticked up a bit this morning, I don’t know that bond investors are willing to jump ship just yet. They’re no doubt pondering whether the Fed is correct in its economic assessment, and thus justified in hiking rates, or whether — as the one dissenter among the Fed’s voting members would argue — today’s economy is in fact not equipped to handle a less-helpful central bank.

We’ll keep you posted…

Have a great weekend!

Marty