RBC’s guy feels very good about the market these days: emphasis mine…

(Bloomberg) — Risk assets should continue higher amid an economy that’s in good shape, barring “some exogenous event,” and “bearish arguments appear to be increasingly contrived,” RBC strategists led by Jonathan Golub write in a note. * Drivers of market upside include: synchronized global pickup, easier lending conditions, improving consumer situation, renormalization of rates and corporate profits…..

And, clearly, he’s in no mood for dissenting opinions.

If you’ve been tuning in here you know that we presently pretty much echo Mr. Golub’s bullish sentiment. But, you know, in our business (to do it right) you gotta stay open to all possibilities.

So, if the setup’s so good, why would anybody waste his or her time contriving false bearish scenarios? Why not just join the trend and buy? Well, in at least one respect the setup isn’t as good as it was, say, last fall (I’ll get to that in a minute). Nevertheless, given the present weight of the evidence (while acknowledging that the market can move against the prevailing trend/evidence at any moment), you have to stretch a bit to paint a resoundingly bearish picture.

So why the bear stretch? Well, I have a theory…

This gets into the weeds a bit, but stick with it (I won’t bog us down):

Let’s say you’re a sophisticated investor, you’ve got cash to burn, and you’ve noticed that the cost of call options on the S&P 500 Volatility Index (VIX) is really really cheap. For example, as I type, you can pick up VIX calls with a 25 strike, maturing in mid-July, for what amounts to $.30 a share. You note that in recent history the market has tended to get volatile come the summer months and maybe you’re in the mood to gamble. So you buy, say, 5000 contracts (1 contract covers 100 shares) for $150,000. Without getting into the minutia of how options work, suffice it to say that if the VIX rises much above 25 you make a boatload of dough. In fact, not adjusting for time value, a move to 30 (not unheard of when the market gets squirrelly) turns your $150,000 investment into $2.5 mill. At 35 we’re talking $5 mill. Thing is, the VIX currently sits around 10, so it’s got a ways to go (hence, the cheap call options). If it doesn’t get above 25 come July you’ve lost the entire $150,000.

Now let’s say you wield some influence; you merit a large audience, so to speak. Not to say that you’d contrive your bearish story (assuming you had some quantifiable reason for your gamble), but, in that you’d benefit immensely should traders suddenly panic, you’ve got huge incentive to scare the bejeebers out of your followers. So, at a minimum, you point to, say, weakening market breadth (the one thing I hinted to above) along with anything else remotely dire that you might come up with.

In my story, you’re the “expert” — with real skin in the game — who finds his/her way to the media with a tale of doom and gloom.

My point? While those doom-seers — whose prognostications can do a real number on one’s psyche — may be completely sincere in their convictions, make no mistake, they didn’t take precious time out of their busy days because they care about you and me enough to warn us of what’s to come. Nope, they’ve already placed their bets and they need the rest of us to take action (panic and sell, pushing the VIX north of 25, in my example) if they’re to cash in.

I.e., if they say governments are printing us into oblivion and you should buy gold — they own gold (and/or they have a book to sell you). If they say the U.S. market’s overvalued and you should short U.S. equities and buy emerging markets (as a couple gurus did recently) — they’ve already shorted U.S. equities and bought emerging markets. If, like Mr. Golub, they cite global synchronization, easy lending and strong consumers as reasons to buy stocks en masse — they own stocks en masse. And so on….

Bottom line folks: We gotta focus on data, not opinion, and think for ourselves!

On Market Breadth:

The healthiest bull markets are ones where their rising tides lift all (or most) boats. As opposed to markets where the major averages are making all time highs while the average stock isn’t. The latter occur when a few big cap names are rising so much that the cap-weighted averages (like the S&P 500) push ever higher, despite the less than stellar performance of the rank and file. Therefore, in our constant market temperature taking, we closely track a number of breadth indicators. And, as of late, we’ve noticed some breakdowns.

One of which would be the percentage of S&P 500 members that are trading above their 50-day moving average. Obviously, a broadly-participated bull market would see most members trading above their respective 50 dmas. As you can see below (panel 2), the present trend is concerning:

click charts to enlarge…

Breadth, via the % of members above their 50 dmas, trending lower amid a rising market is what we call a bearish divergence.

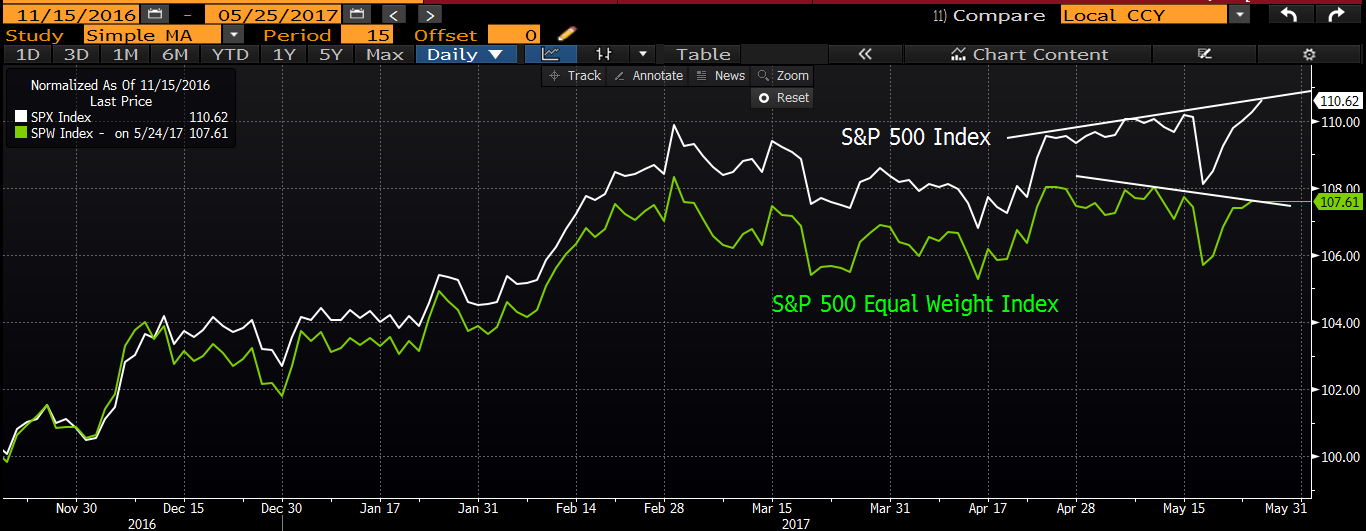

Another breadth red flag is the of late out-performance of the S&P 500 Index over the S&P 500 Equal Weight Index. Again, the S&P 500 is cap-weighted; meaning, larger cap stocks hold greater sway over the index’s performance than do smaller cap members. The S&P Equal Weight Index, on the other hand, gives the same weight to all members, regardless of size. A comparison of the two offers insight into the inclusiveness of the trend.

Have a look:

A trailing Equal Weight Index, along with a bearish divergence in the trend, tells us that recent gains have been concentrated in a few big names.

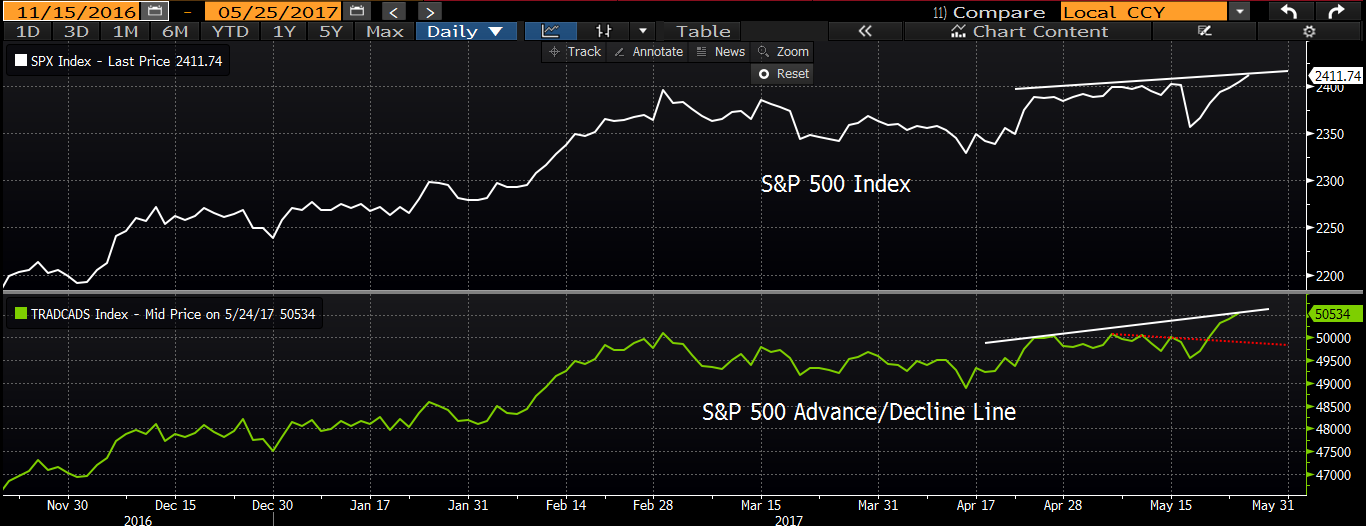

On the other hand, there is at least one key breadth indicator that’s telling a different story — the S&P 500 cumulative advance/decline line. This one moves higher or lower each day based on the number of members whose stocks advance vs decline on the session. For example, if, in a given day, 300 rise in price and 200 decline (showing positive breadth), the a/d line would increase by 100. Conversely, if 300 decline and 200 rise, the line would decrease by 100. Therefore, a rising line denotes strong breadth, and vice versa.

Have a look (panel 2):

The a/d line hitting highs along with the index says good things about the overall health of the rally. Note that as of just a few days ago this one too was flashing caution (red dotted line). Should this bullish move continue, we’ll likely see the other two indicators improve markedly as well.

So, does the concerning signal in two of the three breadth indicators featured herein warrant panic and wholesale selling of stocks? Well, I might say absolutely if I just bet the farm on VIX call options (although, in that case there’s no way I’d have shown you the a/d line). Or I might say absolutely not if I just placed all my money on VIX puts (in which case the a/d line is all you’d have seen). But, since I’m here to share our findings in objective fashion and help you keep markets in perspective, I’ll say that while the recent cautionary trends in certain breadth indicators have our attention, the overall setup (as I type here today, could change tomorrow) tells us to maintain our present allocation course.

Have a nice long weekend!

Marty