Reagan budget director David Stockman has a knack for getting himself in the headlines. Seriously, take a look at his latest work (this is just me Googling for a few minutes):

Dang! A U.S. government budget director ought to know what he’s talking about. So, we should really be worried, right?

Well, let’s Google the past few years:

2016:

2015:

2014:

2013:

2012:

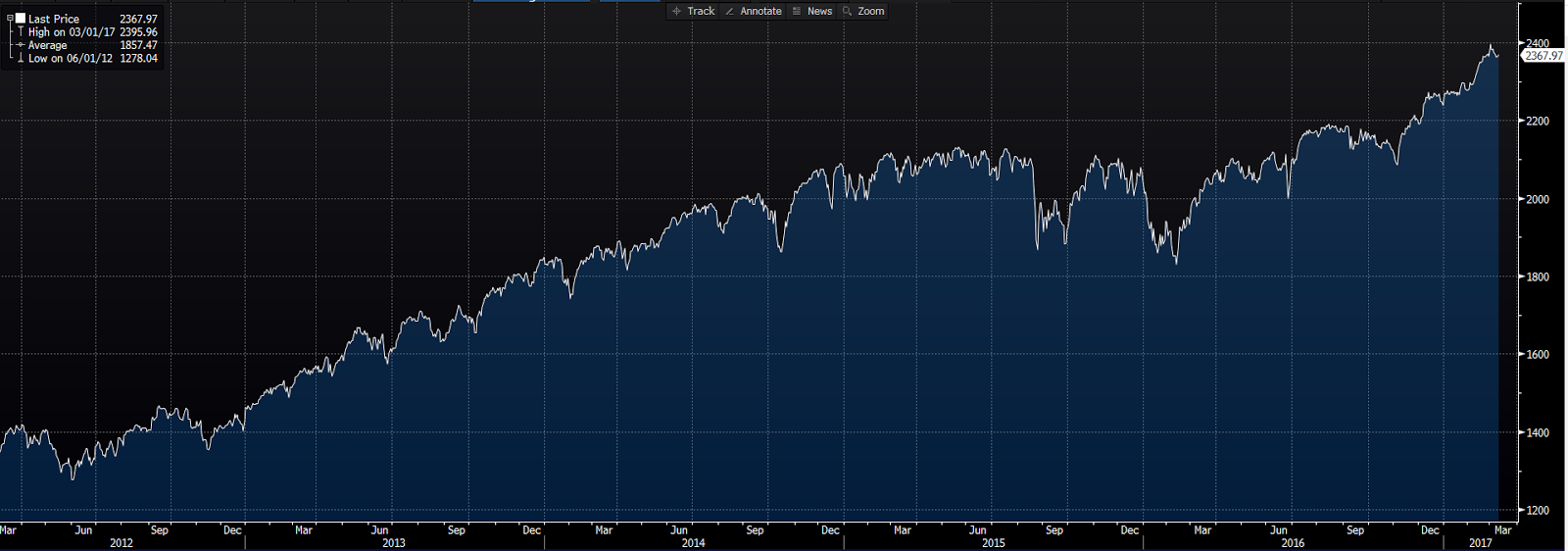

Hmm…. I guess we should run a chart of the S&P 500 from March 2012 to present:

{kind=link}

While, over the past 5 years, Stockman told his horror stories, offered his prognostications and shamed those of us investors who refused to go all cash — oh, and let’s not forget, sold his books — the market managed to grind 73% higher. Hmm….

Does this mean we shouldn’t heed his latest warning, “market bloodbath imminent”? Well, clearly, we shouldn’t heed David Stockman; not because he’s predicting doom and gloom, but because the man’s record needle is hopelessly stuck. The sad thing for his equally-stuck followers is that the proverbial stopped clock being being right for 2 out of every 1,440 minutes applies to the likes of Stockman. I mean, sure, we’re destined for recessions and bear markets (they’re the nature of things), and that’s when their celebrity really shines.

Nassim Taleb, on the other hand, is a heed-worthy fellow for sure:

“Once your mind is inhabited with a certain view of the world, you’ll tend to only consider instances proving you to be right. Paradoxically, the more information you have, the more justified you’ll feel in your views.”

“Our ideas are sticky. And we tend to stick to our theories. Good idea then to delay ones theories, for once they’re made they’re very difficult to let go of.”

As is Anthony Crescenzi:

“There is now scientific evidence indicating that the part of the brain associated with reasoning is inactive when people are given information that conflicts with their own thoughts about a particular subject. In place of reason people seek out information and opinions that confirm their own views.”

In terms of global economic risk, then, whom should we listen to? Well, I think you go where the players have the most skin in the game.

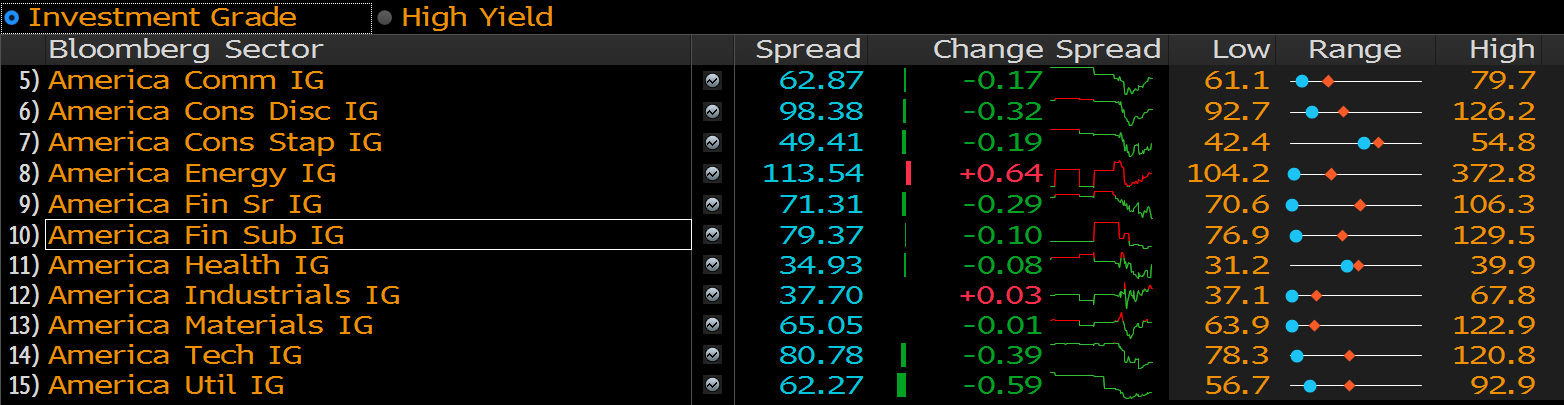

There’s a thing called a Credit Default Swap (CDS); it’s in essence a guarantee of someone else’s, or an entity’s, debt. For example, if I buy a French government bond and want to protect myself, I pay a guarantor a slice of the interest to protect my investment, should I be stiffed by the French. The contract we enter into is the CDS. Of course the riskier the borrower the more the interest the guarantor will require of me to protect myself. Make no mistake, the issuers of CDS, and those who trade those certificates in the market, are intently interested in the health of the global economy. That — as opposed to book sales — is where their livelihoods lie.

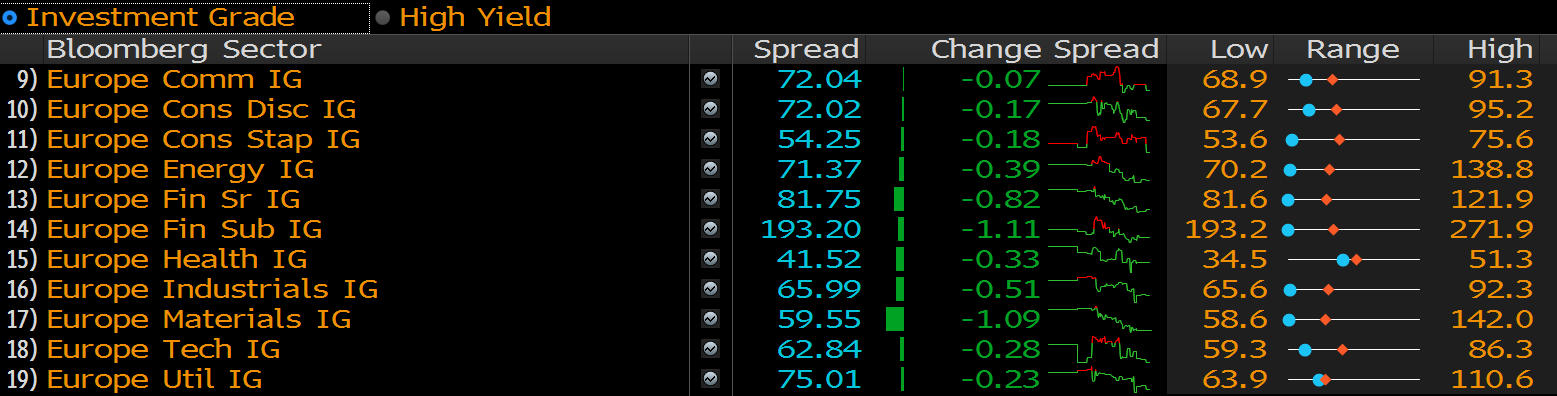

Weekly, I track CDS spreads across nations and across sectors. The following snip shows the spreads for investment grade players within various U.S. sectors. Under “range”, the blue dot represents the current spread, the orange triangle represents the average over the past year. The blue dot left of the orange triangle denotes improved credit risk: click to enlarge…

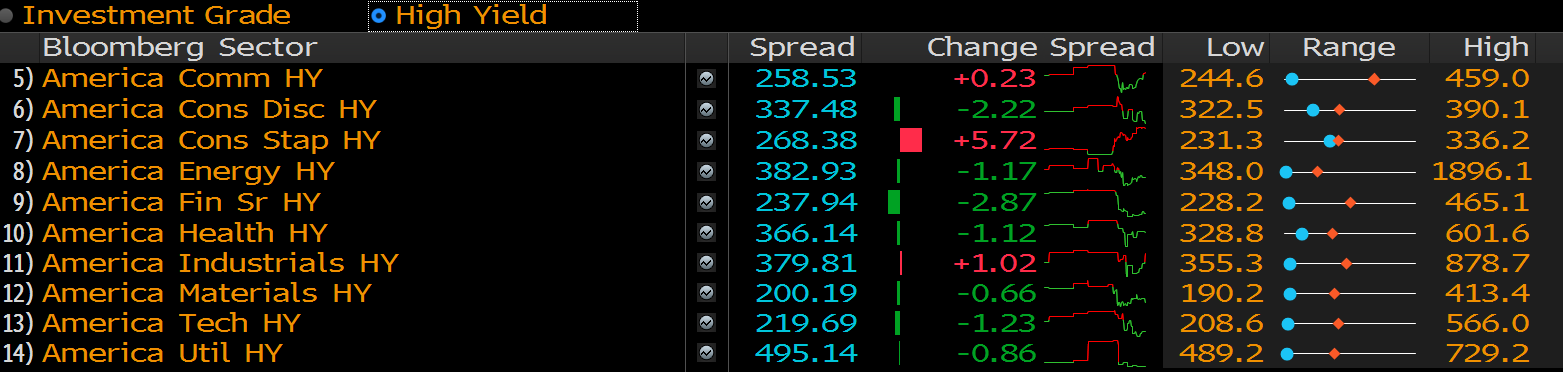

Here are the spreads for U.S. high-yield debt issuers (lower credit ratings) in their respective sectors:

Here’s Europe’s investment grade:

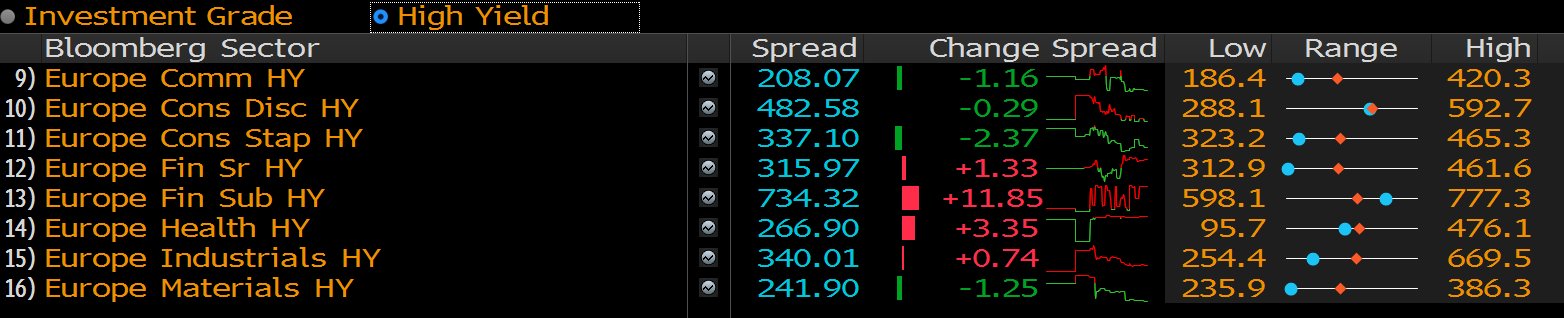

Here’s Europe’s high yield:

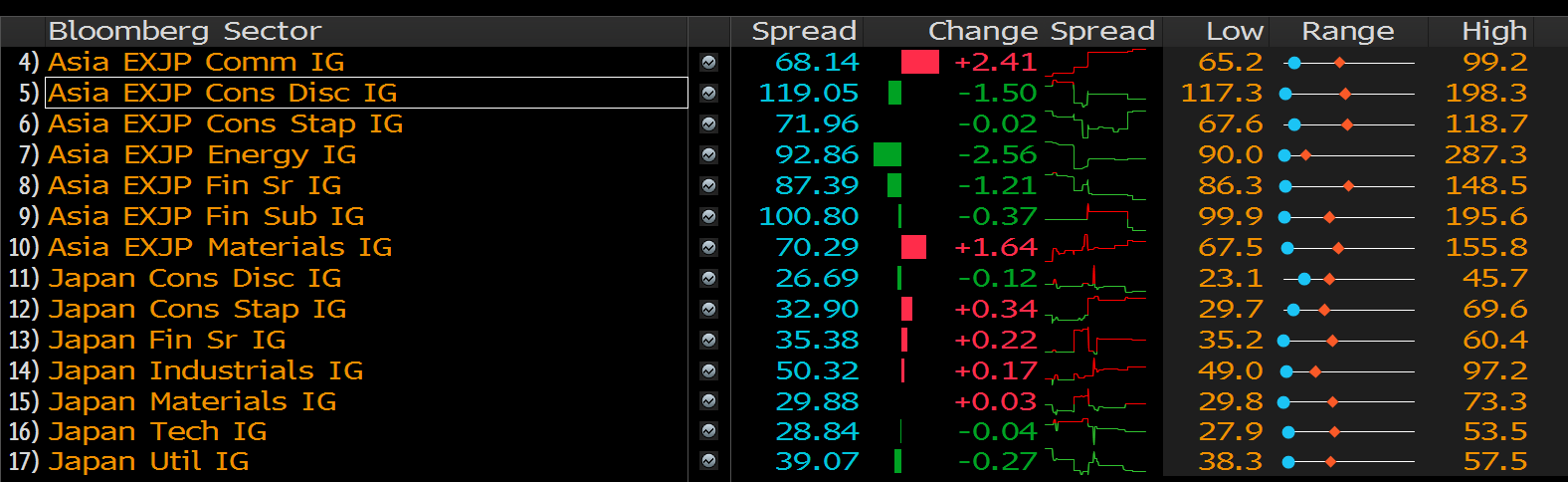

Here’s developed Asia (only investment grade available):

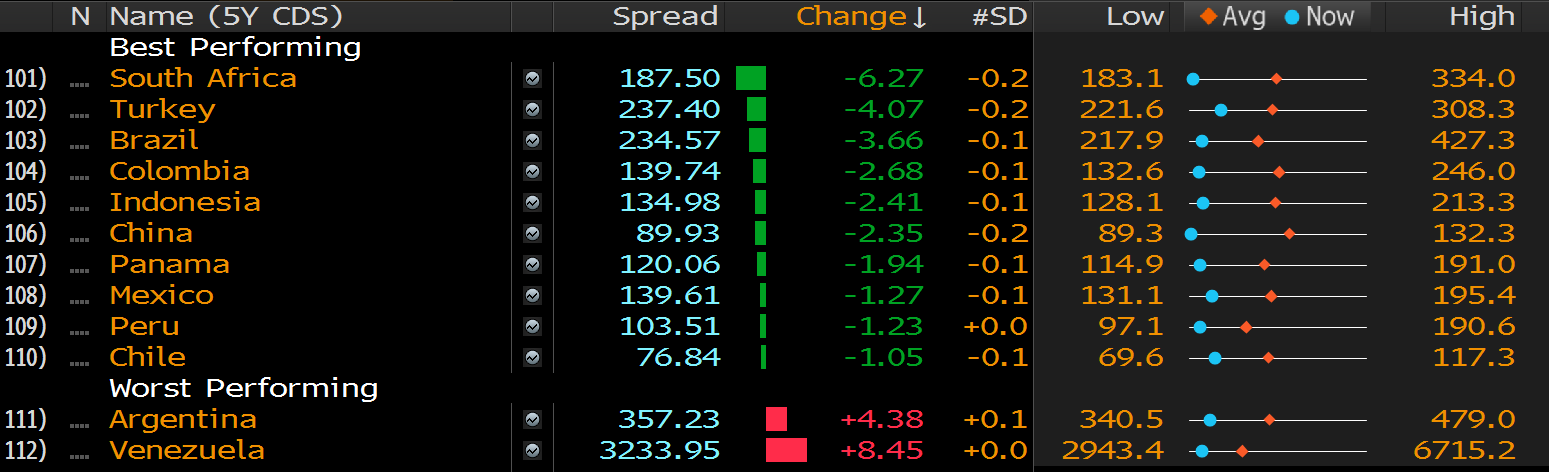

And here are emerging markets:

The bottom line: the folks who absolutely have to be correct on the global economy are feeling relatively okay right about now.

Have a great weekend!

Marty